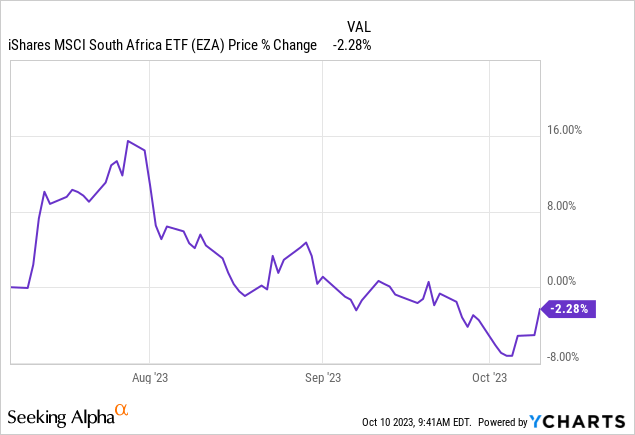

We last covered the iShares MSCI South Africa ETF (EZA) in July, and numerous variables have shifted during the time that has elapsed since then.

For those unaware, South Africa’s financial markets possess significant volatility stemming from the fact that the nation has broad inflation targets (between 3% to 6%), serious geopolitical risks, and a reliance on cyclical sectors such as financial services and mining.

As such, frequent revisions are required. Moreover, the iShares MSCI South Africa ETF is probably best utilized in a tactical asset allocation framework instead of a strategic framework.

Let’s discuss a few events that might influence the iShares MSCI South Africa ETF’s trajectory.

Market-Based Activity

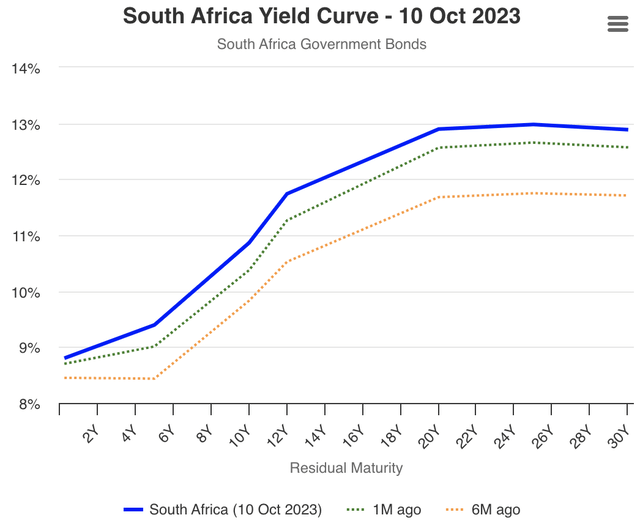

In my view, and in the opinion of many others, stock returns start with the bond market. The bond market lays the foundation for risk premiums, meaning assessment of credit spreads, yield curves, and monetary policy is essential when executing a systematic analysis of a geographic stock index.

South Africa’s yield curve is experiencing significant volatility amid an uncertain policy rate environment. As things stand, the bond market anticipates additional rate hikes by the end of the year, which could send broad-based asset valuations downward.

wordgovernmentbonds.com

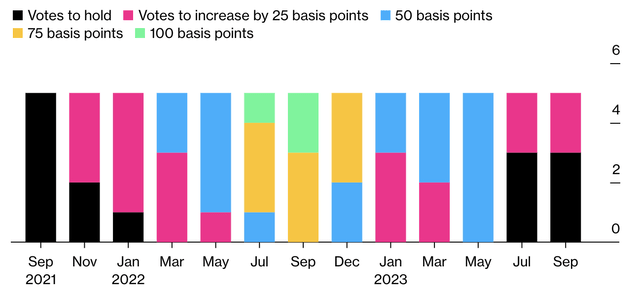

To illustrate the uncertainty about policy rates, I embedded a diagram below, showing that merely one voting member needs to swing the other way (in this month’s policy rate decision) for South Africa’s reserve bank to raise rates.

South Africa Policy Rate Votes (Bloomberg, South African Reserve Bank)

The monetary environment’s instability has carried over into credit spreads, which concurrently raises the risk profile of corporate bonds and stocks alike. If sustained, elevated credit spreads can inflict significant damage to South African stocks.

Investing.com

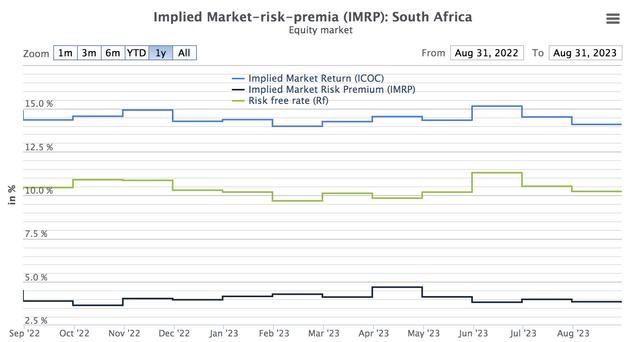

Let’s piece it all together and look at equity risk premiums.

The latest equity risk premium I could gather was recorded at the end of August. Based on how flat it was back then, I believe it is highly unlikely the market anticipated the most recent volatility within the yield curve. As such, I think the next surveyed data will show a significantly higher ERP.

marketriskpremia.com

However, despite the likelihood of a higher ERP, the iShares MSCI South Africa ETF’s recent drawdown implies that the higher risk premium might already be baked in. As such, tactical asset allocators should consider South Africa’s existing risk metrics in tandem with the ETF’s realized price movements.

Portfolio Changes

The iShares MSCI South Africa ETF tracks the MSCI South Africa 25/50 Index, which rebalances quarterly. However, the underlying index’s exposure might change between rebalancing dates as prices change. Moreover, it is an adjusted free-float index, meaning any stock buybacks or equivalent events will likely require the index provider and the iShares MSCI South Africa ETF to adjust their exposure accordingly.

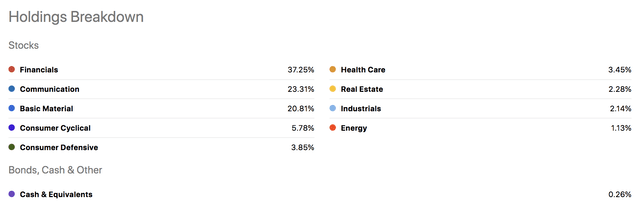

The following table displays iShares MSCI South Africa ETF’s latest allocation, with a discussion following beneath.

Seeking Alpha

The significant changes I noticed are as follows.

| Sector | Approximately Change in Exposure |

| Financial Services (Banking and Insurance) | +2.85% |

| Basic Materials (ex-Energy) | -2.29% |

| Consumer Cyclical | -1.37% |

The increase in financial services exposure seems risky, given the rise in the shorter end of the yield curve, which could potentially result in elevated funding rates for banks. Moreover, rising CDS spreads is worrisome as it will increase the velocity of asset base downgrades in the event of an interest rate hike while also raising the probability of higher default rates.

Furthermore, there has been a reduction in basic materials exposure. However, Gold Fields (GFI) and AngloGold Ashanti (AU) span nearly half of the ETF’s basic materials allocation. This implies that the recent price drop in gold probably lowered the weight of basic materials.

In my view, lower exposure to gold isn’t necessarily a good thing. Gold stocks provide diversified returns, which may be beneficial given that global markets are yet to consolidate a clear direction.

Lastly, there’s been a reduction in consumer cyclical exposure, which is probably a good thing if the regional risk environment is considered. Moreover, the ETF has a humongous position in Naspers (OTCPK:NPSNY), providing it with an offshore hedge as most of Naspers’ operating activities occur outside of South Africa.

Sure, the substantial allocation to Naspers introduces concentration risk. However, it is well worth it in my point of view.

Seeking Alpha

Valuation and Dividend Profile

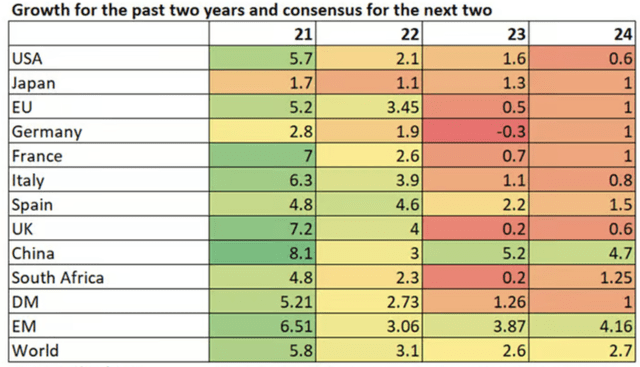

One could argue that the ETF is fairly priced at a price-to-earnings ratio of 10.23 and a price-to-book ratio of 1.45. However, my concern is that South Africa’s forecasted economic growth is slow, providing little substance to its non-exporting companies’ valuations. In essence, I fail to see how non-exporting companies will be able to grow their earnings and book values in the next two years.

GDP Growth Forecasts (Investec Asset Management)

On the other side of the spectrum, foreign demand might recover in the coming years, supporting South Africa’s export industries and Naspers. Thus balancing the argument.

However, in general, I revert to my opening statement: the EZA ETF is probably more of a tactical play than a strategic asset that would provide long-term growth prospects.

From an income-based perspective, one would have to say that the iShares MSCI South Africa ETF ranks quite well with its 3.62% dividend yield. However, note that these dividends are taxed to most foreigners and are generally quite cyclical, given the ETF’s underlying exposure.

Seeking Alpha

Final Word

South Africa’s central bank policy seems indeterminate at this stage. Consequently, the bond market has priced in significant risks, which has been relayed into the equity market.

Arguments exist that the iShares MSCI South Africa ETF’s headwinds are baked in. However, investors would be wise to consider re-evaluating their exposure to the ETF.

Read the full article here