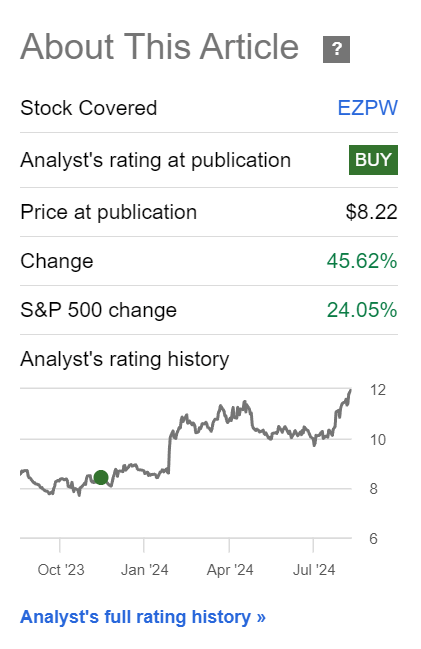

EZCORP (NASDAQ:EZPW) has been one of my favorite ways to capitalize on my macroeconomic view of a weakening economy, especially for lower-income consumers. Since my last article in November, EZPW’s stock has been on a tear, returning 45% and leaving the S&P 500 Index in the dust (Figure 1).

Figure 1 – EZPW shares are up 45% since November (Seeking Alpha)

With the company recently reporting Q3/F24 earnings, let us review EZPW’s YTD results to determine whether EZCORP remains a buy at this time.

EZCORP continued to see double-digit revenue and earnings growth as struggling consumers continued to increase their utilization of pawn loans to meet their financial needs. Trading at just 10.6x Fwd P/E, I continue to view EZPW as a countercyclical investment to play the cost-of-living/inflation crisis. I reiterate my buy rating on EZPW’s shares.

Brief Company Overview

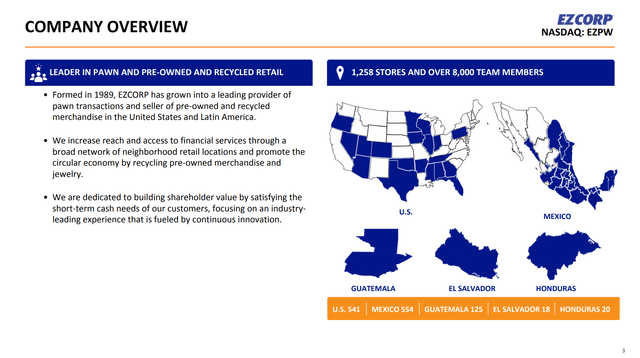

First, for those not familiar with the company, EZCORP is one of the largest pawn brokers in the U.S. and Latin America with over 1,200 retail stores across 5 countries (Figure 2).

Figure 2 – EZPW overview (EZPW investor presentation)

EZCORP’s main business is extending “pawn loans” to consumers. Pawn loans are consumer loans fully collateralized by underlying “pawned” merchandise.

While pawn lenders are commonly grouped with payday lenders as both target struggling consumers, their credit risk profiles are dramatically different as pawn loans are fully collateralized and only lend a fraction of the merchandise value while payday loans are non-recourse loans. Loan losses are typically very low for pawn loans.

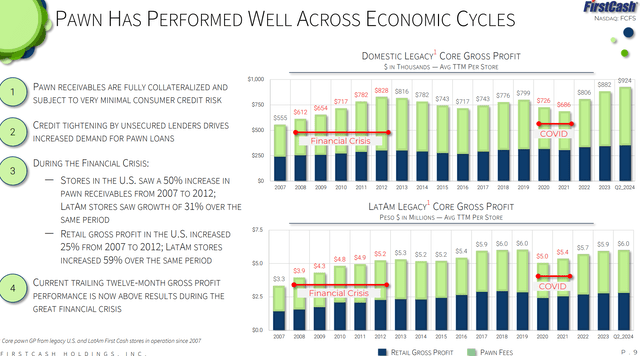

Historically, the use of pawn brokerage services is counter-cyclical to the economy; low-income consumers tend to fall back on pawn loans or payday loans during tough economic times as they struggle to meet financial obligations (Figure 3).

Figure 3 – Pawn loans are countercyclical (FCFS investor presentation)

Readers interested in learning more about the business should read my initiation EZCorp Stock: Tailwinds From A Weak Economy on EZPW.

Q3/2024 Review

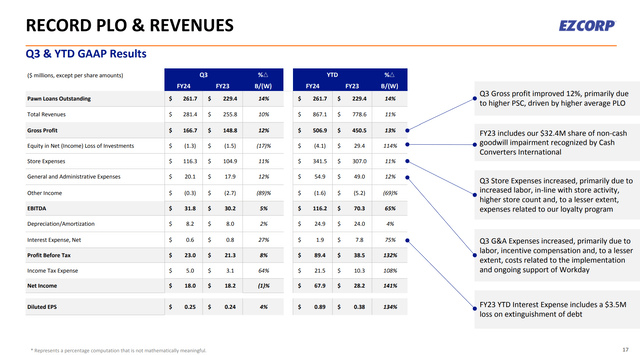

Recently, EZCORP reported strong Q3/F24 results, with the company delivering a 10% YoY revenue gain to $281 million and diluted EPS of $0.25 compared to $0.24 in Q3 2023. YTD, EZPW’s revenues were $867 million (+11% YoY) while dil. EPS grew 134%YoY to $0.89, as 2023’s results included a large write-off of EZPW’s investment in Cash Converters International (Figure 4).

Figure 4 – EZPW Q3/24 financial summary (EZPW investor presentation)

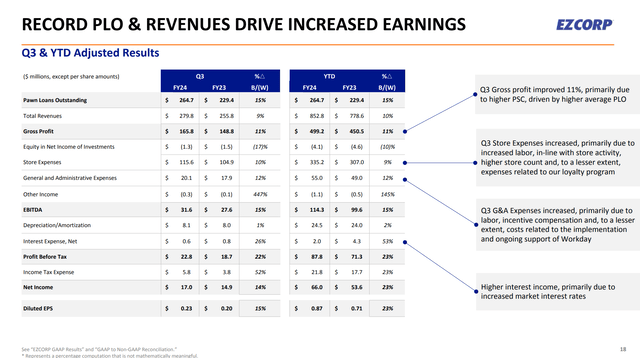

On an adjusted basis, backing out the 2023 write-offs, earnings grew a more normalized 15% YoY in Q3 to $0.23 / share (Figure 5).

Figure 5 – EZPW Q3/24 adj. financial summary (EZPW investor presentation)

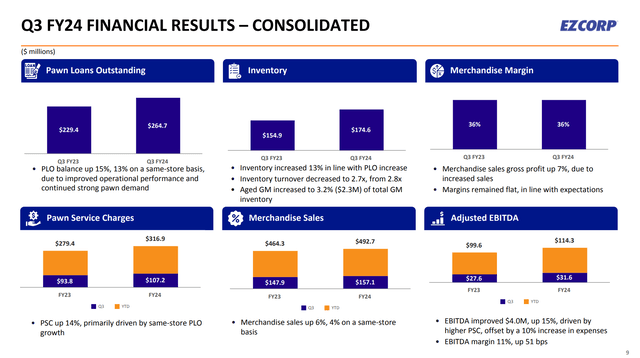

EZCORP continued to see strong demand for its pawn broking services, as pawn loans outstanding (“PLO”), a key performance indicator for EZCORP, grew 15% YoY to $265 million, while pawn service charges (“PSC”) grew 14% YoY (Figure 6).

Figure 6 – EZPW Q3/24 Key Performance Indicators (EZPW investor presentation)

Adj. EBITDA for EZCORP grew faster than revenues, increasing 15% YoY, as PSC growth outpaced expenses growth of 10% YoY.

EZCORP’s merchandise gross margin stayed flat YoY at 36%, suggesting business remained relatively healthy, while inventory turnover ticked down to 2.7x. However, aged inventory, another indicator of pawn performance, increased 0.9% QoQ to 3.2%, suggesting there is some stale merchandise in EZCORP’s stores.

Latin America Is The Standout Performer

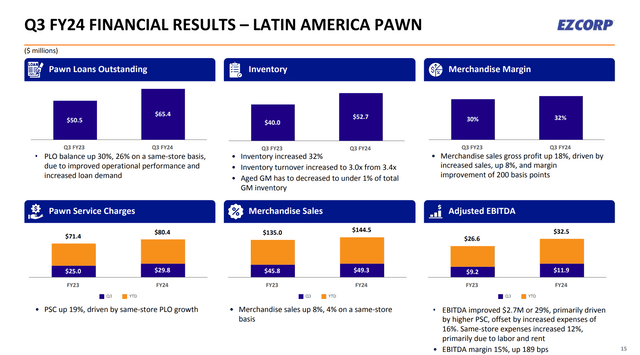

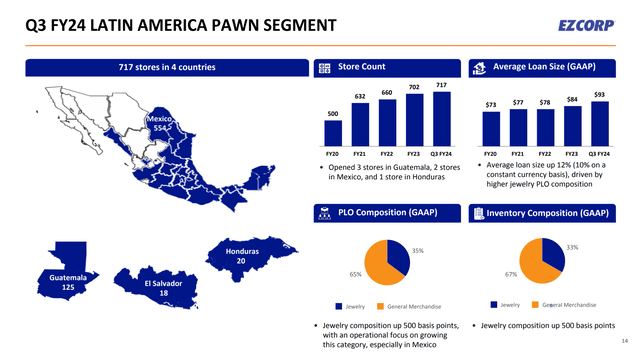

Digging through EZCORP’s results, the clear standout performer has to be the company’s Latin American operations, as Latin America PLO grew 30% YoY on the back of rising consumer demand for pawn brokerage services (Figure 7).

Figure 7 – EZPW Latam PLO grew 30% YoY (EZPW investor presentation)

Latin American growth was due to a combination of higher store count, higher throughput (i.e. more loans per store), and larger average loan sizes as EZCORP gained headway in larger-ticket jewelry loans (Figure 8).

Figure 8 – EZPW Latam operations overview (EZPW investor presentation)

As expected, EZPW’s operations continued to deliver solid growth as low-income consumers struggled to make ends meet in the face of the ongoing cost-of-living crisis.

Valuation Continues To Screen Cheap

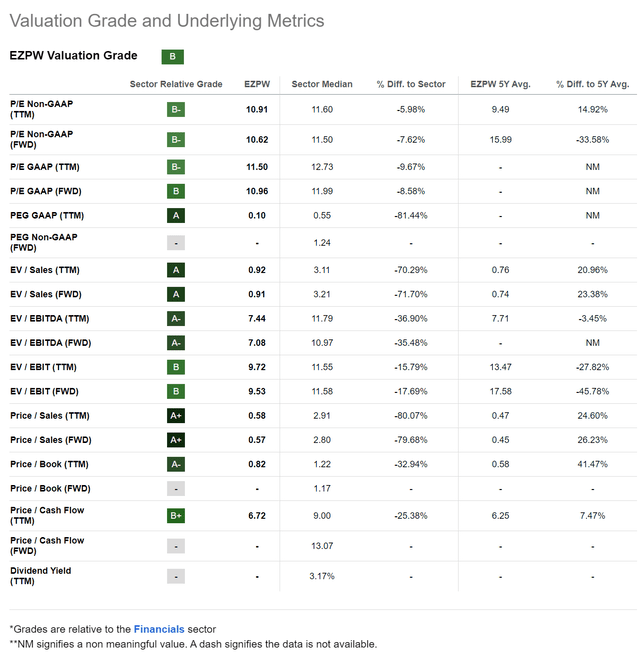

Despite the stock rallying more than 45% since November, EZCORP still screens as cheap on valuations, as the company’s fundamentals have grown in the past year. On 2024 earnings, EZPW is only trading at 10.6x Fwd P/E, a discount to the Financial sector’s 11.5x multiple (Figure 9)

Figure 9 – EZPW continues to screen cheap (Seeking Alpha)

Furthermore, unlike banks and other financial institutions that experience declining earnings from higher loan losses when the economy worsens, EZPW’s pawn brokerage business experiences a tailwind when the economy gets tough.

Technicals Target All-Time Highs

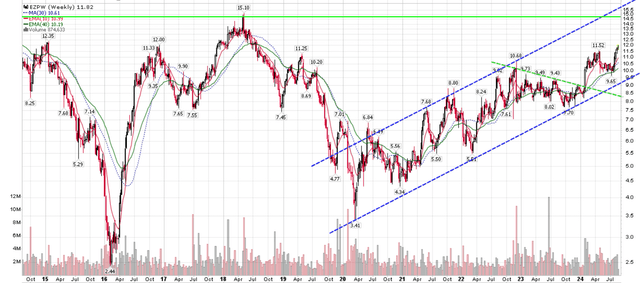

Technically, EZPW’s chart continues to rally within a well-defined uptrend established since the COVID lows in 2020 (Figure 10).

Figure 10 – EZPW’s chart continues to grind higher within uptrend (Author created with price chart from stockcharts.com)

A recent breakout of EZPW’s stock from a small downtrend in 2023 suggests the company is well on its way to re-test the upper end of the up-channel and all-time highs of ~$15 / share from 2018.

Conclusion

Overall, EZPW’s latest quarter results continue to demonstrate how EZCORP’s pawn brokerage business is ideally suited for the current tough macroeconomic environment as low-income consumers struggle with the cost-of-living crisis.

I continue to rate EZPW a buy.

Read the full article here