One company (and especially stock) that was always too expensive in the last few years and therefore not a great investment was FactSet Research Systems Inc. (NYSE:FDS). In my last article published in September 2022 I wrote:

FactSet also belongs to the category of great businesses with a wide economic moat that are just not available for the right price. While the business model is great, the stock is simply not a good investment as it is too expensive in my opinion.

Due to the extremely high valuation multiples, FactSet is faced with a high risk of multiple contraction in the next few quarters. And in combination with possibly lower earnings per share, FactSet’s stock could easily be cut in half – like it has been following the Dotcom bubble and the Great Financial Crisis.”

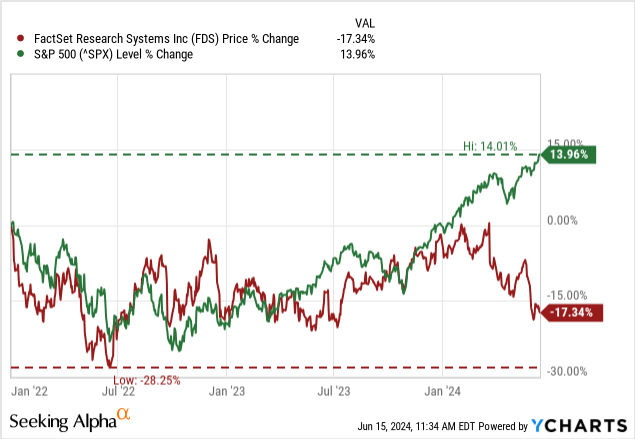

So far, the stock has not been cut in half. Instead, it is still trading rather close to its all-time highs. But since 2022, the stock has been in a side way correction and since my last article was published the stock declined about 10%. While 10% seems not so dramatic, the underperformance becomes obvious when comparing FDS to the S&P 500 and looking at the performance since the beginning of 2022.

FactSet lost about 17% in value since early 2022, the S&P 500 gained 14% in the same timeframe. And in the years 2022 and 2023, the index and FDS performed more or less in line, but in the last few months the discrepancy became obvious. In the following article we answer the question if FactSet is a good investment now.

Valuation Multiples

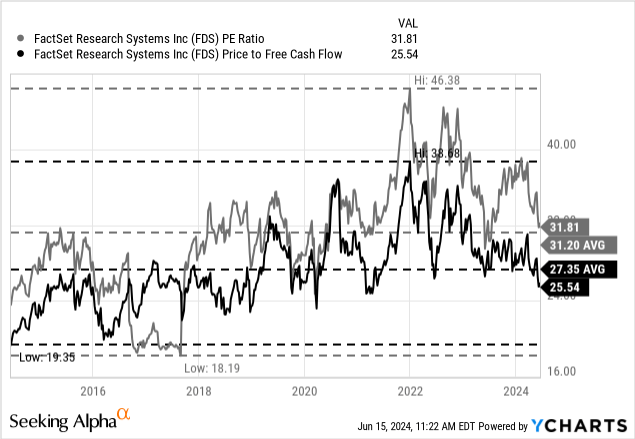

In the last few years, I always saw FactSet as too expensive and one quick way to determine whether a stock is rather expensive or not is by looking at the two major valuation multiples – the price-to-earnings ratio as well as the price-free-cash-flow ratio. And in early 2022, the P/E ratio peaked around 46 times earnings per share and has since then declined to 32 times earnings per share. It is now in line with the 10-year average again (which was 31.20).

The picture for price-free-cash-flow ratio is the same. At the peak, FactSet was trading for 39 times free cash flow, and it declined to 25.5 times free cash flow during the last few quarters. And while FactSet is still trading slightly above the 10-year average P/E ratio, it is now trading below the 10-year average P/FCF ratio, which was 27.35.

We certainly can claim that the stock got more reasonably valued, but on the other hand a valuation multiple around 30 is still not cheap, and we have to take a closer look at the business and stock to answer the question if FactSet is a good investment right now.

Quarterly Results

We saw the P/E ratio and P/FCF ratio getting lower over time, but the stock price did not decline nearly as much as the valuation multiples. Hence, only one conclusion is logical: While FactSet has been in a side way correction at a high level, the fundamental business improved. And the results for the second quarter of fiscal 2024 were underlining this statement.

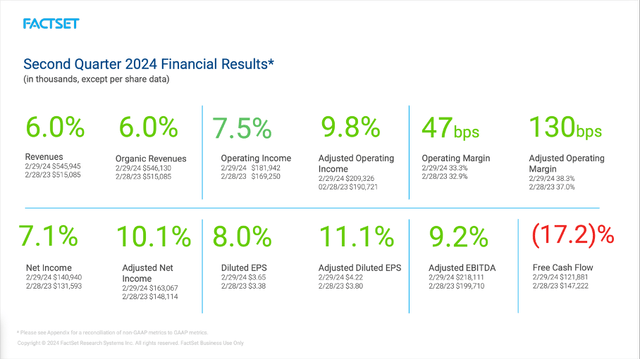

Revenue increased from $515.1 million in Q2/23 to $545.9 million in Q2/24 – resulting in 6.0% year-over-year growth. Operating income also increased 7.4% year-over-year from $169.3 million in the same quarter last year to $181.9 million this quarter. And diluted earnings per share grew even 8.0% year-over-year from $3.38 in Q2/23 to $3.65 in Q2/24.

FactSet Q2/24 Presentation

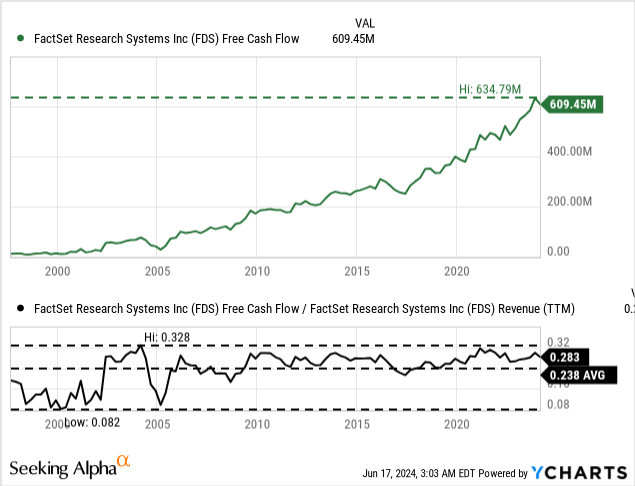

However, one important metric is declining. Free cash flow declined from $147.2 million in the same quarter last year to $121.9 million this quarter.

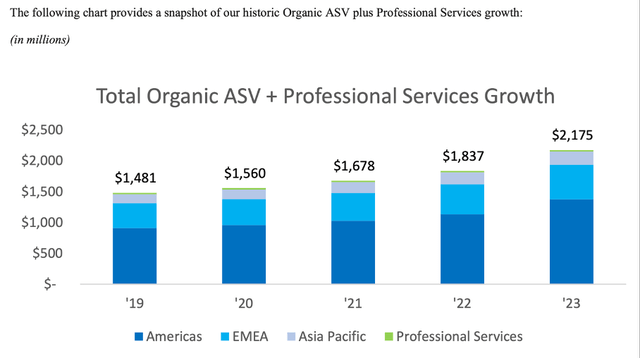

And in case of FactSet, we should look at some other metrics as well. One important metric is the ASV – the annual subscription value – which is representing the forward-looking revenues for the next twelve months from all subscription services clients. And on February 29, 2024, ASV plus professional services was $2,208.8 million compared to $2,096.2 million one year earlier – an increase of 5.3% year-over-year. And when looking at the bigger picture we see total organic ASV constantly growing in the last few years.

FactSet Annual Report 2023

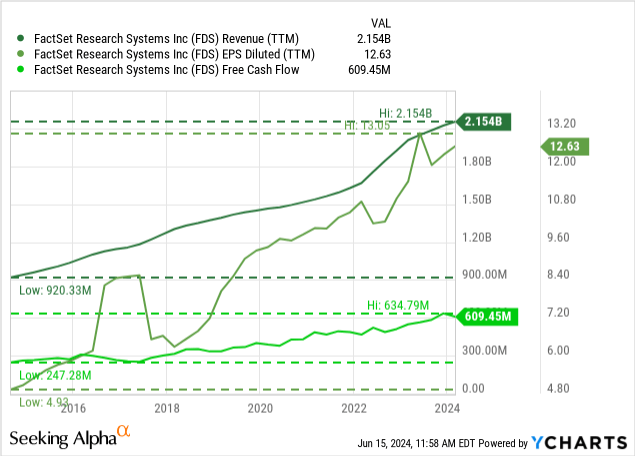

And the same is true for the income statement. When looking at the last ten years, we see revenue, earnings per share and free cash flow continuing to grow with a solid pace. Revenue increased with a CAGR of 9.29% in the last ten years, and while operating income also increased with a CAGR of 9.29% in the same timeframe, earnings per share increased even with a CAGR of 10.47% in the last ten years.

So far, we can argue that FactSet is continuing to perform well and the reason for the struggling stock price is probably the extreme valuation and not so much the fundamental performance of the business.

Growth

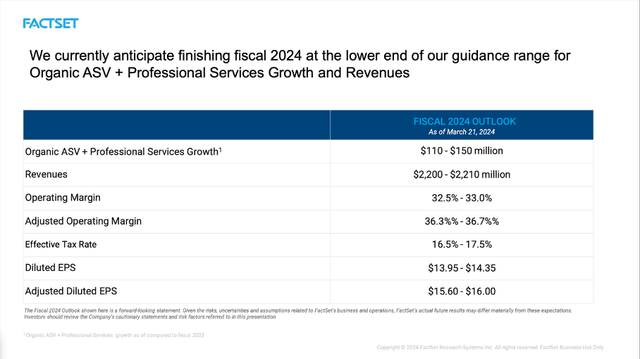

When looking at the company’s guidance for fiscal 2024, management is expecting revenue to be between $2,200 and $2,210 million. When comparing this amount to the fiscal 2023 results, top line would grow close to 6% year-over-year. And diluted earnings per share are expected to be in a range of $13.95 to $14.35. In fiscal 2023, FactSet generated $12.04 in earnings per share and therefore bottom-line growth would be between 16% and 19%.

FactSet Q2/24 Presentation

It seems like management is still quite optimistic for fiscal 2024 and is assuming growth to continue. And analysts are sharing this optimism. In the next five years until fiscal 2028, revenue is expected to grow with a CAGR of 6.1% and earnings per share are expected to grow with a CAGR of 9.75%. These growth rates are slightly lower than the growth rates in the last ten years but can be called reasonable.

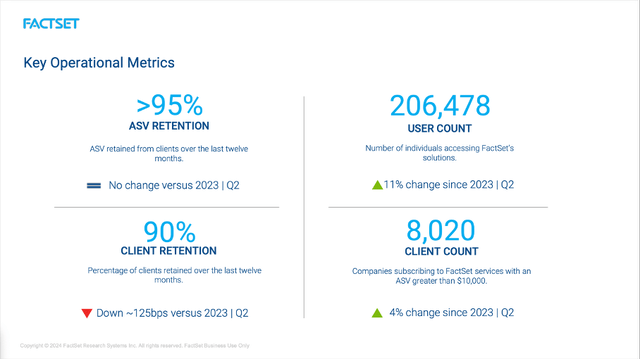

When looking at some other metrics, there is reason for caution as well. The client count in the last three months increased by 75 clients and is now 8,020. And while an increasing number of clients is good, FactSet needs a certain growth rate for its clients to achieve revenue (and earnings per share) growth. While 4% year-over-year client growth could still be acceptable, the user count actually declined in the last three months. It only declined by 605 users to 206,478, which is a rather small decline, but it is a decline nevertheless and a problem for a growing business. Additionally, the client retention rate declined to 90% (125bps lower than in Q2/23).

FactSet Q2/24 Presentation

Of course, these are not horrible results, and the company is still reporting a high ASV retention above 95% and in my first article about FactSet I already described the economic moat based on switching costs:

These switching costs mostly stem from steep learning costs, that most companies and clients are trying to avoid. A company might have to train its staff to use another platform and the knowledge how to use FactSet’s tools and programs that many employees might have gained over the years suddenly is lost. To understand the whole functionality of a platform takes a lot of time. Especially smaller companies don’t have the time and/or financial resources to double these investments they already made (considering money as well as time).

Additionally, these systems and the provided data might also be embedded in other applications or software the company uses and this embeddedness is creating high switching costs as it would take a lot of time to “fix” this. So even if another company comes along with a slightly better or cheaper product many customers won’t switch as the process of switching costs a lot more than the company would save and this is creating pricing power for FactSet.

And despite the economic moat and clients still growing, I argue to be rather cautious at this point for reasons I will explain in the following section.

Risks

Of course, there are many risks surrounding a business all the time, but in the case of FactSet, I would like to highlight two potential risks that seem important at this point. One of these two risks I have already written about in previous articles – the risk of an economic downturn and recession going hand in hand with a bear market. And such a scenario would have an impact on FactSet Research – in my opinion.

However, I mentioned in my last article that FactSet can be described as rather recession-resilient when looking at the numbers. Revenue never declined in the last three decades (which are including at least two severe recessions and bear markets). And despite FactSet’s revenue not declining in the past, I wrote:

And while I don’t want to dispute evidence from the past, we still must assume FactSet being affected by the next potential recession. In case of a bear market – and the 2020 bear market doesn’t count as it was quickly replaced by euphoria once again – the number of clients and users will probably decline. When asset prices are declining quarter over quarter, many people are suddenly not interested in financial markets anymore and often sell assets. This will lead to a lower number of users and institutional investors might cut staff (which will also lower demand for subscriptions).

And it seems like the sky is getting cloudier here. In the last few months, especially the fund management industry was hit by layoffs and with fewer analysts and reduced staff, customers of FactSet will renegotiate their contracts and simply need less licenses, which is leading to lower revenue and lower ASV for FactSet Research. I, personally, assume that the situation will continue to get worse in the coming quarters – a scenario that is not reflected in the guidance and analysts’ estimates. For several of FactSet’s clients – especially banks and asset managers – we can assume challenging times ahead (for more information, see my last article about the Toronto-Dominion Bank (TD))

Another risk, which I did not mention in this context before, but which could also lead to layoffs in the banking and asset management industry is artificial intelligence and the possible applications, especially generative AI, could have. The layoffs mentioned above are already occurring due to the shift away from active managed products towards passive managed funds, i.e. ETFs. And this trend could accelerate in the years to come with money flowing more and more towards passive managed funds. With AI tools making progress and getting better, it seems possible and likely that some tasks of people working in the banking and financial industry will be replaced. And this is making fewer licenses necessary and lead to lower revenue for FactSet.

Intrinsic Value Calculation

Finally, we can also use a discount cash flow calculation to determine an intrinsic value for the stock. And as always, we are calculating with 38.65 million outstanding shares as well as a 10% discount rate as this is the annual return we like to achieve (at most). As basis for our calculation, we can use the free cash flow of the last four quarters, which was $609 million.

When calculating with these assumptions, FactSet must grow its free cash flow “only” 6% annually from now until perpetuity in order to be fairly valued. And at this point, we can make the argument that 6% annual growth seems achievable for the business. Such a growth rate is not only below past growth rates but also below analysts’ assumptions for the coming years. Even when taking into account the above-mentioned risks for the business, I think 6% growth on average is achievable for FactSet.

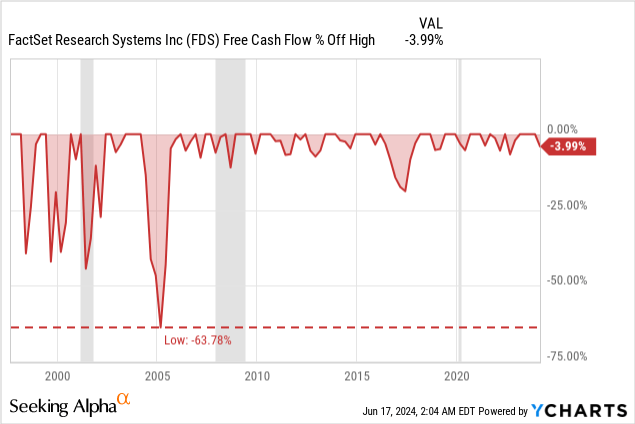

And we also must discuss if the free cash flow of the last four quarters is a reasonable basis we can take for a calculation. When looking at the last three decades, we see several drawdowns for free cash flow, but we can’t really associate these drawdowns with recessions. Instead, it seems just like normal fluctuations. We could also make the argument that the free cash flow/revenue ratio is a bit high at this point, but I still think the free cash flow of the last four quarters can be used as the basis for our calculation and FactSet could be seen as almost fairly valued.

Conclusion

In my opinion, FactSet is still a “Hold” but the stock is certainly not so expensive anymore as it was in the last few years. And at this point we can make the argument for FactSet being more or less reasonably valued. But the stock is still not a bargain and considering more difficult times ahead with layoffs and cut-backs in the banking and asset management industry, I would still not but the stock. Due to high switching costs and a sticky product, FactSet might be able to avoid declining revenue, but declining earnings per share and declining free cash flow are likely in the next few quarters.

On Friday, June 21, 2024, FactSet will report third quarter results. But we should be cautious as the stock is certainly still not cheap and the risk of further declining stock prices is rather high, and the upside is limited in my opinion.

Read the full article here