Summary

Following my coverage of Fair Isaac Corporation (NYSE:FICO), I recommended a hold rating due to my preference for a cheaper valuation before investing. This post is to provide an update on my thoughts on the business and stock. While the 3Q23 results were okay on a standalone basis, the red flags that I have identified continue to worry me. Furthermore, I believe the current valuation is not sustainable given the expected earnings growth rates and also relative to comps. I note here that the FICO valuation has gotten even higher than the last time I wrote about it, which indicates that expectations have gone even higher. Hence, I am downgrading from a hold to a sell with expectations of valuation reversion to the mean.

Valuation

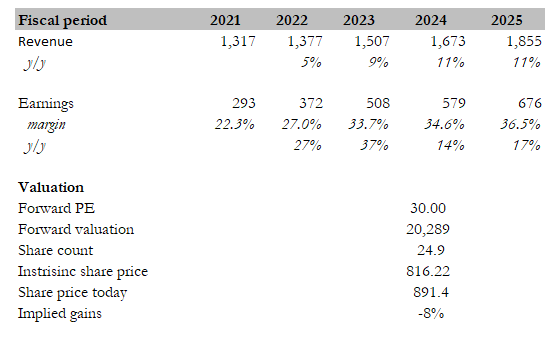

Own calculation

I am shifting the valuation section up as it deserves attention given the current state of things.

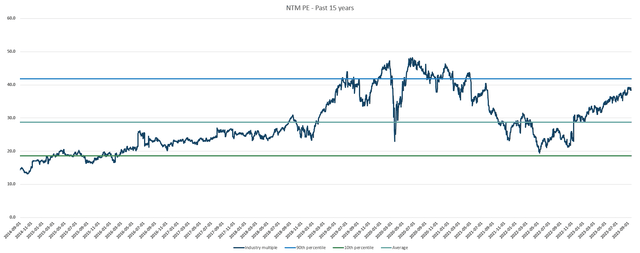

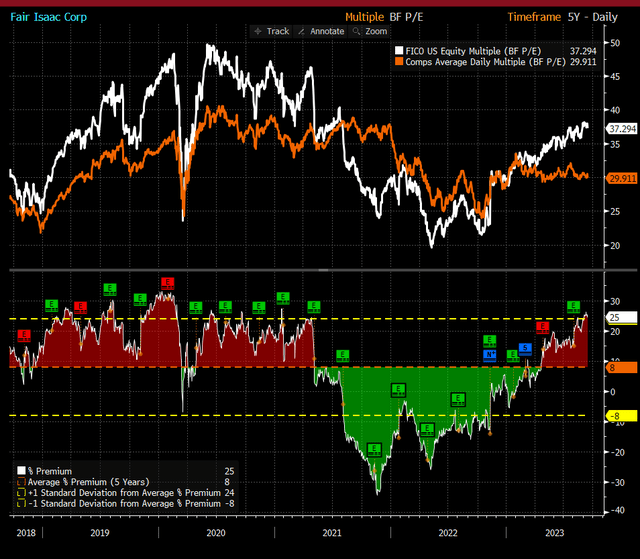

I believe the fair value for FICO based on my model is $816. My model assumptions are that revenue will eventually track back to the low teens as the economy normalizes, which should drive near-term acceleration given the weakening of 2021 and 2022. Margins should also gradually improve as the business continues to exert its pricing power. The issue is that I don’t think FICO can continue to trade at 37x NTM PE given the expected earnings CAGR over the next 2 years (based on consensus estimates). The last time FICO traded at 37x NTM PE during FY19 was when the business had an expected 2Y net income CAGR of 30% (FY19 EPS was $5.35, and consensus FY21 EPS back then was $8.35). This is a stark difference from current expectations. While I do give credit that the net margin profile today is much better, I don’t see it as a factor that warrants an elevated multiple of 37x (which is also near the +1 standard deviation across its 15 years of trading). When compared to peers, FICO is also now trading at a premium of 25% vs. peers, which is a 17-point difference from its average of an 8% premium over the past 5 years. This is despite similar revenue and earnings growth expectations between FICO and peers.

Peers include Morningstar, Transunion, Equifax, S&P Global, Verisk Analytics, Moody’s Corp., MSCI, and Factset Research Systems. The median forward earnings multiple of these information services peers is 30x, and the expected 1Y revenue and earnings growth rates are 13% and 38%, respectively, which is in line with FICO.

Own calculation Bloomberg

Investment thesis

3Q23 revenue for FICO was $399 million, up 14.2% year over year and 9.4% higher than consensus had predicted. Scores contributed to the company’s growth by increasing its revenue by 12.5% y/y, with growth in B2B sales (up 24%) offsetting a decline in B2C sales (down 11%). Furthermore, software sales increased by 16.1% year over year. EBITDA margins increased by 550bps to 53.9%, which is better than the consensus estimate of 52.9%, and earnings per share of $5.66 was higher than the consensus estimate of $5.25.

I think overall the 3Q results were fine, but I think the expectation for the business might be running too high, especially considering the red flags I am seeing and the valuation that it is trading at. For example, Scores’ B2C revenue dropped 11% year over year in the third quarter, a rate of decline that accelerated from the 8% seen in the second quarter. Higher interest rates and falling mortgage volume were blamed for the drop in myFICO.com memberships. Management has stated that myFICO.com volumes are stabilizing on a quarterly basis, and that B2C revenue in F4Q should be comparable to 3Q, but I am still concerned about a continued decline because these two factors are beyond management’s control. Both of these factors may suffer if the macro environment worsens. My interpretation of the “stabilization” trend thus far is that clients are increasingly signing up for credit monitoring services ahead of schedule, in anticipation of an uptick in home buying. This does not indicate that the mortgage market as a whole is getting healthier. Therefore, I do not anticipate a return to B2C expansion until consumers once again have faith that the housing market has bottomed.

While revenue in the B2B segment grew by 24%, volume growth data indicates underlying weakness. For instance, business-to-business card and personal loan origination volumes have declined year over year and quarter over quarter. These things tell me that the business operating environment is weakening inexorably, and I attribute this to companies cutting back on spending because they fear a recession in the US.

Conclusion

In conclusion, my assessment of FICO has led me to downgrade my rating from a hold to a sell. While the 3Q23 results displayed respectable performance, certain red flags persistently concern me. Notably, FICO’s valuation has surged even higher, surpassing sustainable levels when compared to expected earnings growth and peer benchmarks. The historical context of FICO’s valuation reveals a stark contrast to its current expectations, challenging the justification for its elevated multiple. Moreover, FICO now trades at a 25% premium to its peers, far exceeding its historical average.

Considering the recent decline in B2C revenue and underlying weaknesses in the B2B segment, it’s apparent that the business environment is deteriorating. These challenges, coupled with a potentially unstable macroeconomic landscape, cast doubt on FICO’s growth prospects.

Read the full article here