The MarketDesk Focused U.S. Dividend ETF (NASDAQ:FDIV) was launched by Empower Funds and is co-managed along with MarketDesk Indices. The fund is advised by Empower Capital Management, which manages a large pool of mutual funds with assets topping $125 billion as of Q3, 2023. As a group, Empower has over three decades of experience. MarketDesk Indices, the group managing FDIV, is essentially a tech enabler that provides, among other services, quant portfolio solutions.

As you can imagine, the strategy behind FDIV is highly quant-driven, and you’ll see that reflected in its 60% annualized turnover. The ETF has an expense ratio of 0.35%, which isn’t too expensive, but I assume much of that goes toward transaction fees. The $104 million AUM doesn’t offer much in the way of liquidity, which averages about 13,400 ETF shares traded on a daily basis.

As a dividend-focused fund, you’d expect the yield to be considerably higher than most other ETFs, so I was surprised to learn that the current yield is just 1.9%; that’s not even close to the 2.6% median for all ETFs. Moreover, the total return with all distributions reinvested is a paltry 7.7% against the broader market’s 15.4%, on a YTD basis.

As such, I’m not recommending this ETF, but I’m open to rating it a Hold because of a few reasons that I’ll outline here.

Why FDIV is Not Working Now

There are several reasons why the yield isn’t as promising as the ETF’s name would make it out to be. The obvious one is that equities have had a strong run over the past year, which is how long the fund has been in existence (inception date: 9/19/2024).

SA

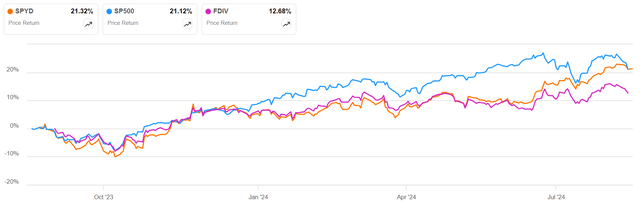

The fund was launched about a month before the long rally in the market that lifted the (SP500) by more than 20%. Interestingly, the SPDR Portfolio S&P 500 High Dividend ETF (SPYD), another dividend-focused ETF, has appreciated the most in terms of price, and its forward dividend yield is still an impressive 4.15% as I write this.

So, the first reason FDIV’s yield is that low is because its holdings have collectively appreciated about 13%, so that’s proportionately pushed down the yield.

However, this observation raises another issue – why didn’t FDIV’s equities appreciate as much as SPYD’s?

That leads to the second reason, and I believe that has to do with the quant strategy behind the ETF. FDIV and SPYD both hold a comparable number of equities, with FDIV holding about 67 stocks and SPYD holding about 83, both as of September 5, 2024. So, although SPYD’s AUM is $6.5 billion against FDIV’s $104 million, there’s still a reasonable basis for comparison.

SA

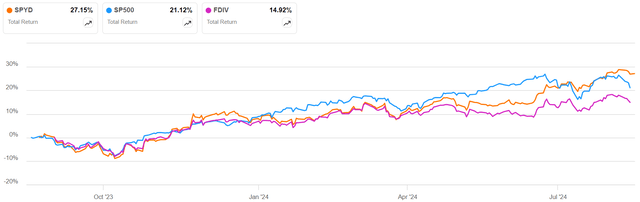

If you look at total return, you’ll see that SPDY has not only beat FDIV with dividends reinvested, but it’s even beaten the index by a considerable margin since July. You can also see how its high yield is capably negating some of the effects of capital decline toward the end of those graph lines.

Putting it all together, it’s clear that FDIV isn’t performing up to expectations, and in my opinion that’s likely because the quant model used to make these stock picks is dynamic and still learning. In contrast, SPYD’s 46% turnover suggests that their model for picking top dividend payers from the SP500 works better when pitted against the underlying benchmark, the S&P 500 High Dividend Index.

MarketDesk Indices Website

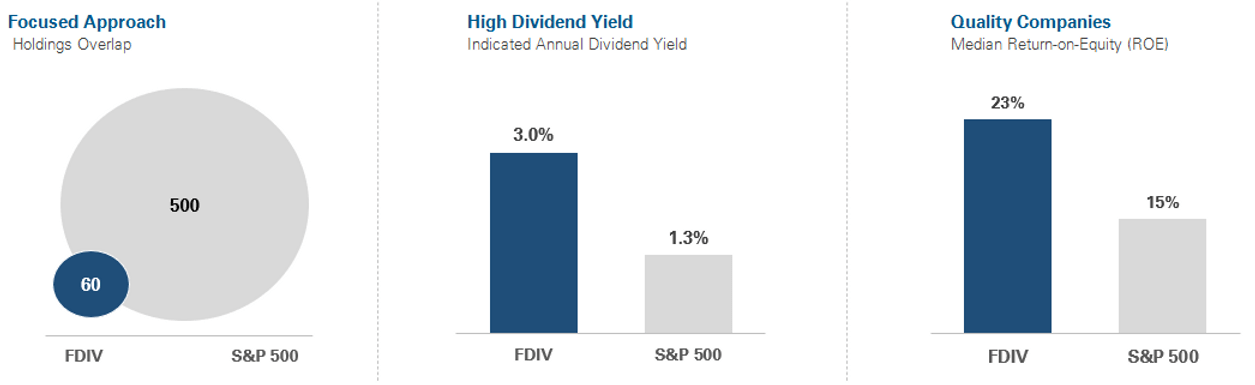

FDIV, on the other hand, goes outside the SP500 to make its picks, with a relatively small overlap. Moreover, there’s a massive difference in sectorial distribution between these two dividend-focused ETFs, which is the third reason why FDIV is underperforming SPYD as well as SP500.

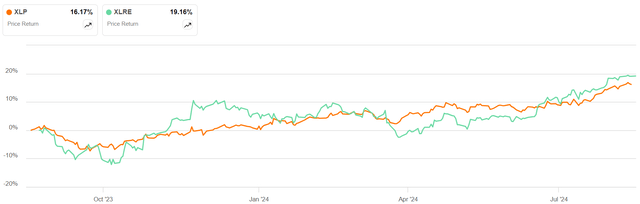

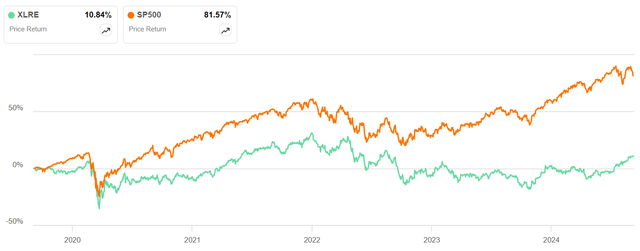

If you look at their holdings, it becomes obvious. SPYD has a 24% weighting to Real Estate, which includes REITs that need to distribute the bulk of their earnings. FDIV, on the other hand, is 26% weighted to Consumer Defensive. Unfortunately, that’s not working well at the moment, although it theoretically should.

SA

So, on the one side, you have the quant model making more frequent rebalances, and on the other, you have the sectoral picks not performing the way they normally do. Over the past ten years, consumer staples stocks have done extremely well, while real estate has lagged behind, but if you zoom into a one-year period (hint: the period of time this new ETF has been around), it’s clear that real estate is coming into its own. This possibly marks an end to the long period in which the real estate sector has been underperforming the market, but more relevant to our thesis for FDIV is the fact that consumer staples, by comparison, just aren’t cutting it.

SA

That being said, things will very likely change if there’s a major market disruption, and there are several signs that point to this as a real possibility. Volatility is still a real concern right now, and I believe it’s going to get worse before things settle down in the markets.

SA

If you look at the S&P VIZ Index over the YTD period, it’s clear that the market is still showing signs of instability after a relatively calm period – between the spike after the July jobs report and the yen carry trade debacle that broke in early August, and now.

The crux of the matter seems to be that FDIV is positioned well for a recession, but since the economy has been so resilient over the past two years, its strategy of selecting stable dividend payers like Mondelez International (MDLZ), The Hershey Company (HSY), and PepsiCo (PEP) hasn’t really panned out. For instance, both HSY and PEP have either lost ground or moved sideways over the past year, and we’ve seen how most other consumer staples have struggled to gain alpha during that period.

My Take on FDIV

The way I see it, unless there’s a recession up ahead or the fund drastically alters its sectoral allocation strategy, it’s going to be hard to deliver the kind of gains that you’d get with a SPYD holding, or even with the broader (SPY).

Moreover, even if we do see a recessionary economy in the year ahead, it only means FDIV’s holdings are going to drop their yields, and much of the distribution is likely to shift to return of capital vs investment income (dividends). Depending on your tax situation, that could be favorable to you, but it’s only favorable to the fund if there are fresh inflows from investors.

In either scenario, investors would benefit. The only problem is, until the Fed starts its rate cuts, presumably to be announced after the Sep 18 FOMC meeting, we won’t have a clue as to the probability of a recession over the next year to year and a half.

For now, therefore, I’d recommend staying away from FDIV. I like the fund and its strategy, but it seems to me that designing a fund to navigate a recession turned out to be more than a little premature. A year into the fund’s existence and we still don’t have much visibility into the state of the economy, so even though we’re seeing a lot of market volatility right now, it’s hard to take a call on FDIV based on whether or not a recession is imminent. As such, I can only recommend a Hold.

Read the full article here