Roughly half a decade ago, I found myself preparing for a visit to a frigid Montreal. At the time, I was a student at the University of British Columbia, nestled in the much milder city of Vancouver. Realizing I’d need some warmer armor I’d subtly hint at my predicament in casual conversations, fishing for some advice, or better yet, recommendations for a suitable jacket. Now, brace yourself, because I am about to use the word “bruh”… a term I usually avoid. The recommendation of Canada Goose (NYSE:GOOS) from the “bruh” crowd was resounding. Vanity prevails and since I really wanted to look cool, I bought my beloved North Face jacket instead. How about that for a plot twist?

Yet, the genesis of my current argument has roots in that interaction. I was fresh from my triumph over the Level 2 exam in the CFA in the preceding year. And after that triumph, I had consumed a small library’s worth of books on the qualitative aspects of investing. I knew I liked the moat. I kept tweaking numbers in my DCF model to discover scenarios to build a compelling long case. But the pricing was just way off. My view is changing though, it pays to be patient. As it stands now, I hold a decidedly bullish view on GOOS.

Company Overview

To the uninitiated, GOOS is a globally recognized brand, well-known for its premium outerwear products. With its origins dating back to 1957, the company has built a reputation on the back of its high-quality parkas designed to withstand the harshest of winters.

While parkas are a staple in their product line, Canada Goose has gradually diversified its portfolio to include lightweight jackets, knitwear, accessories, and more recently, footwear, thanks to its strategic acquisition of Baffin Inc. in 2018. This diversification allows the company to cater to a broader range of weather conditions and consumer needs.

Geographically, Canada Goose’s presence is felt worldwide. While North America remains its biggest market, the company has been rapidly expanding into Europe and Asia. Especially noteworthy is its growth in the Chinese market, a testament to the brand’s global appeal.

An important part of Canada Goose’s business strategy is its Direct-To-Consumer, or DTC offerings. The DTC approach, which includes both e-commerce and company-owned retail stores, has been instrumental in strengthening its relationship with customers. This strategy not only allows Canada Goose to control its brand presentation but also offers better profit margins than wholesale distribution.

From an economic moat perspective, Canada Goose is more than just a retailer of luxury winter wear. It’s a brand that has successfully tapped into the global luxury apparel market with a diversified product mix, a strong DTC presence, and a growing international footprint. As we delve deeper into the analysis, you’ll see why I hold a bullish view on this company.

Valuation: Skeptical Topline, Believable Bottom Line

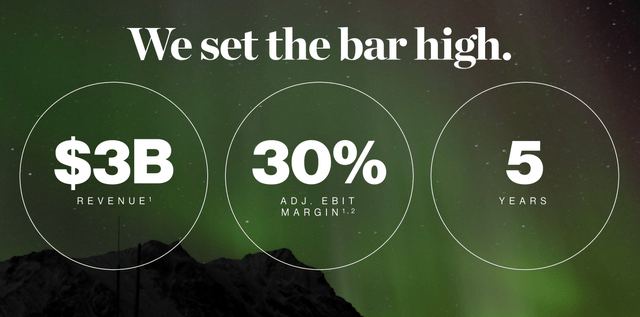

Canada Goose investor day (Canada Goose)

Source: Canada Goose Investor Day Presentation

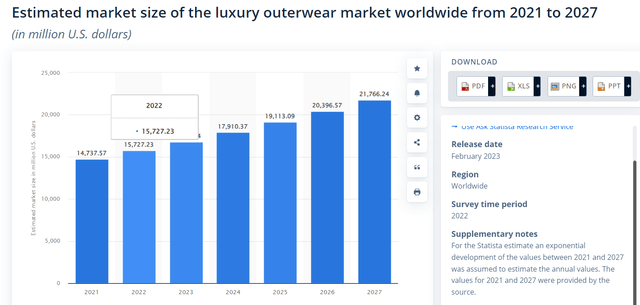

We are not insiders in the company, and it would be foolish to assume we know more than management. Yet, I find myself questioning some of their assumptions. Based on market size estimates, Canada Goose had a market share of close to 6% in 2022.

Statista

Source: Statista

If we believe growth estimates for the luxury outdoor market, management expects market share to edge closer to 10% in 5 years. I don’t want to argue my assumption is better than yours. Not a big fan of dancing on a tightrope stretched over a volcano. Let’s use precedents instead. In 2018, Credit Suisse had a note about how GOOS had a market share of 6% vs 16% for Moncler (OTCPK:MONRF).

Forbes

Source: Forbes

If you were curious about Credit Suisse, they lost a staggering $60 million underwriting the stock. But I digress. Looking at current figures, it appears as though we’ve been circling the same pond for the past half-decade, with market share stubbornly stuck at ~6%.

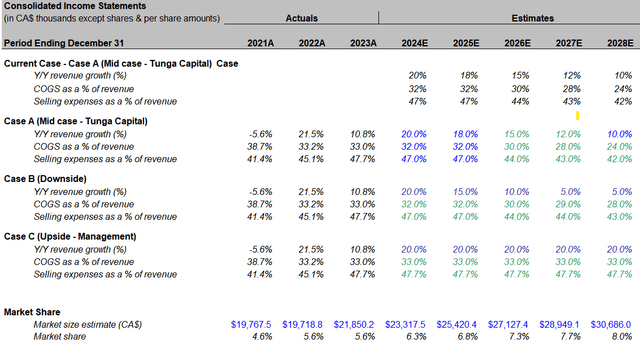

So I have a downside that assumes market share stays at 6% by 2028 and management expectations of 10% as the upside. I feel 8% is a fair credit to recent 20+ percent topline growth achieved by both GOOS and Moncler (27% increase in revenue FY22). Both companies have at least a narrow moat stemming from their brand and are therefore best positioned to take market share at this point in time.

| Scenario | Market Share in 2028 | Basis for Assumption |

| Downside | 6% | Historical performance over the past 5 years |

| Middle | 8% | Credit to recent 20%+ topline growth that eclipses ~8% growth in luxury outdoor market. But assumes persistent 10%+ outperformance of the market is unlikely. |

| Upside (Management Expectations) | 10% | Management estimates based on revenue projections in recent investor day. |

Author’s basis for assumptions for scenario analysis

Author

On the other hand, the company’s EBIT projections are reasonable. Moncler already has 80% of its sales coming from DTC. At the scale of CAD 3 billion revenues, EBIT margin would expand to 30% based on efficiencies of scale and the gross margin bump coming in from DTC sales. With my 8% of market share assumption, revenues only stretch to ~CAD 2.4 billion. So I am projecting a 24% EBIT margin in 2028 for now.

On the working capital side, days payable are projected at 55 days, a slight improvement over the years but assuming they have net 60 paying terms, there is little incentive to pay earlier. Finished goods inventory concerns were factored into the response after earnings. Moncler had a 23% increase in finished goods inventory as well, compared to 28% in GOOS. But with a mid-20 percent increase in sales, forecasting inventories can be difficult and it is hard to pin that as a fault.

In the past, capital expenditure has been between 2.9% and 3.7% of sales but just to push the numbers towards conservatism, I have assumed it at 4%. Strangely I have seen some authors pick 8% as the discount rate. If you look at notes in the company’s 20-F filings (below), interest rate on its term loan is LIBOR plus 3.5%. Current LIBOR (assuming quarterly rate for quarterly payments) is at least 5.5% resulting in an interest rate of at least 9%. Debt is cheaper than equity, so 8% is just too rich even after assuming long term average rates.

Canada Goose

Source: Company filings, 20-F FY23

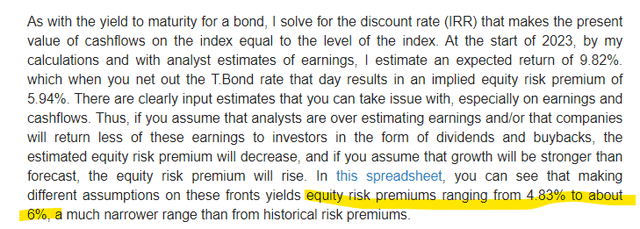

I have assumed a discount rate at 12.6% which is 14.6% minus 2% to account for long term averages. Ashwath Damodaran is a well-known expert in the valuations world. Based on his calculations, I have picked the higher end of implied equity risk premiums at 6%.

Equity risk premium (Ashwath Damodaran)

Source: Ashwath Damodaran’s blog

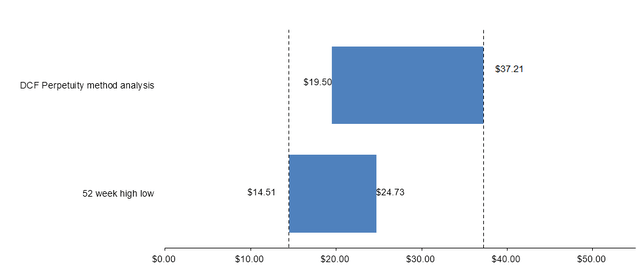

With all of the above assumptions, I have a downside valuation of $19.50 and management case valuation of $37.21. My mid-case is clocking in at $28.34. And the thing I like is the minimal upside overlap below.

Author

Risks vs Reward

If a shortcut to a destination involves a dark alley, would you take it? It’s not well lit, it looks menacing. Time seems like a fair trade for security offered by the longer route. However, if you’re journeying home, in a neighborhood you know like the back of your hand, this shortcut becomes a practical, time-saving solution. Unless you are averse to shadows.

Current pricing of GOOS mirrors this analogy, reflecting a sentiment of risk aversion among investors-much like the fear of shadows. Of course, failure to execute targets by management could potentially sink GOOS, but it’s safe to assume they’re acutely aware of this. Similarly one could argue consumer preferences could change. Technically it could, but it’s not something you can attach easily to a company experiencing 20+ percent revenue growth. Revenues are harder to manipulate.

Avoiding shadows doesn’t alter the fact that the shortcut is fundamentally safe. Even legitimate fears can lead to irrational choices. Much like the dimly lit pathway the recent declines of GOOS have lit up the stock for the vigilant, yet cautious investor. At $18, the stock represents a viable value proposition for the cautious, yet astute, investor.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here