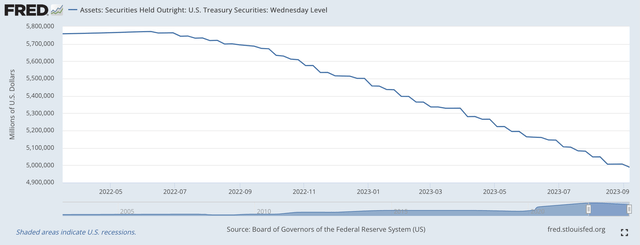

The Federal Reserve began to reduce the size of its securities portfolio, the securities it bought outright in March 2022.

This week, the balance sheet of the Federal Reserve, the H.4.1 statistical release shows that Securities Held Outright were $8,490.5 billion on March 16, 2022, and were $7,489.7 billion on September 6. 2023.

Securities portfolio down…$1,000.8 billion…or $1.0 trillion!

So Federal Reserve officials have been watching its securities portfolio decline for one and one-half years!

Wow!

Who would have thought at the start?

Securities Bought Outright (Federal Reserve)

This is quantitative tightening at its best.

Quantitative Monetary Policy

This is the fifth effort that the Federal Reserve has made at some kind of “quantitative” policy.

Basically, the idea in these quantitative policies is to let the securities portfolio either increase or decrease steadily for a substantial amount of time, with very little variation in the effort, if any at all.

The first three efforts at quantitative easing came in the 2010’s came in the 2010’s and were the creation of the then Federal Reserve Chairman, Ben Bernanke.

Mr. Bernanke believed that a policy stance should be created where the Federal Reserve, in the case of quantitative easing, acquired securities, outright, at a regular pace for an extended period of time.

Mr. Bernanke did not think that the extended period of time should be too long, but it should be long enough to convince participants in the financial community that the Fed was serious and was going to stick to its guns.

Mr. Bernanke described the effort of one of trying to create a “wealth effect” that would cause an increase in consumer spending.

Mr. Bernanke was especially interested in creating a steadily rising stock market.

In all three efforts, Mr. Bernanke succeeded in getting the results he wanted.

Consequently, the U.S. economy went through the longest economic recovery on record since the Second World War.

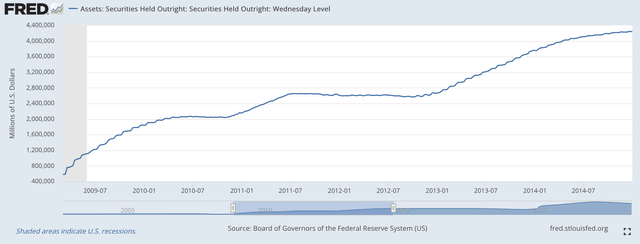

Here is the picture of Mr. Bernanke’s efforts.

Securities Held Outright (Federal Reserve)

One can very clearly see the three periods in which the Fed’s securities portfolio was increasing during this time period.

Fed Chair Janet Yellen did not add anything to this and the securities portfolio actually declined modestly while Ms. Yellen was directing the Federal Reserve.

The economy, overall did very well through the 2010s, following the picture Mr. Bernanke originally drew. Wealth increased, spending increased, and the economy did just fine.

Also, price inflation remained modest.

For the whole period of expansion following the Great Recession which ended in June 2009, the economy rose at an annual compound rate of 2.3 percent and the price index concentrated on by the Fed increased also at an annual compound rate of 2.3 percent.

The only grip people really had during this period was that the economy rose as slowly as it did. However, the economy did rise, and rise, and rise.

What seems to have happened is that the Fed’s stimulus tended to go into financial markets and not into the building of real capital expenditures.

A consequence of this was that during the decade the growth of labor productivity slowed and this factor seems to have caused the economy to grow at a slower rate than it had done in the past.

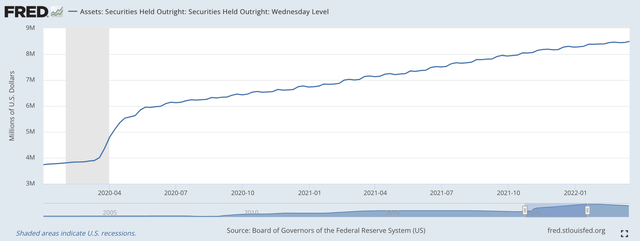

Quantitative Easing–Number Four

During the period under review, there was one additional case of quantitative easing. It came under the leadership of Fed Chairman Jerome Powell.

Securities Held Outright (Federal Reserve)

One can see that Mr. Powell and the Federal Reserve responded to the recession and engaged in a very aggressive round of quantitative easing.

People have accused Mr. Powell and the Fed of being too “loose” during this time period and forcing too much “cash” into the financial system.

As a consequence, the effort has left an enormous amount of liquidity in the financial system.

That is another topic for another time.

The point is, Mr. Powell and the Federal Reserve relied on the fourth round of quantitative easy to protect the U.S. economy and keep the economy from falling into a very severe recession…or, worse.

The problem, however, is that the head of a faster rate of inflation began to show up and Mr. Powell and the Federal Reserve had to reverse course.

But, and this is very important.

The path that Mr. Powell and the Fed followed was one of “quantitative” tightening. The steady reduction in the amount of securities the Fed held outright on its balance sheet.

Quantitative Tightening

What does this tell us?

It tells us that the Federal Reserve has a whole new operating policy procedure, one that was created and initially initiated by Fed Chairman Ben Bernanke.

The inflation rate in the U.S. economy dropped to a 4.2 percent year-over-year annual rate. Not yet where the Fed wants it, but it is heading in the right direction.

It now appears as if quantitative easing or quantitative tightening IS the major operating monetary policy of the Federal Reserve.

What about movements in the Fed’s policy rate of interest?

It appears as if the Federal Funds rate now is a secondary tool.

The Federal Reserve moves its policy rate of interest to meet the market needs.

In the past year and one-half, the market has needed to see a rising Federal Funds rate. The effective Federal Funds rate now stands at 5.33 percent.

But, what is most important is how the Federal Reserve is handling its securities portfolio.

The Future

And, what can we expect from the Federal Reserve in the near future?

Mr. Powell has stated that the Federal Reserve will do what is necessary.

What that means to me right now is that the Federal Reserve will continue to reduce the size of its securities portfolio.

Will it reduce the securities by another $1.0 trillion?

Maybe…or, maybe not.

But, for the time being, it will oversee a continued reduction in the size of its securities portfolio.

Will Mr. Powell and the Fed raise the Federal Funds rate in the near future?

My best guess is YES.

How far will the Fed continue to raise the rate?

Mr. Powell is watching the market.

But, this seems to be secondary.

When will Mr. Powell and the Federal Reserve stop letting the Fed’s securities portfolio shrink?

Keep watching the H.4.1.

Read the full article here