Beginning in March 2023, the Federal Reserve had to deal with some bank failures.

As a consequence, Federal Reserve officials changed their focus a little bit in responding to the problems of the failing banks and responding to the possibility that there could be more bank failures given that the Federal Reserve had been engaged in a policy of quantitative tightening, reducing the size of its securities’ portfolio, along with a series of increases in the Fed’s policy rate of interest since the middle of March 2022.

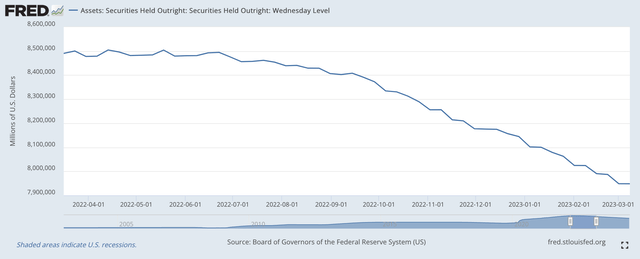

Between the start of the Fed’s policy of quantitative tightening and March 2023, Federal Reserve officials had overseen a sustained decline in the size of the Fed’s securities portfolio. (These figures were obtained from the Federal Reserve H.4.1 statistical release, “Factors Affecting Reserve Balances of Depository Institution.”) So

Securities Held Outright–3/16/22 to 3/8/23 (Federal Reserve)

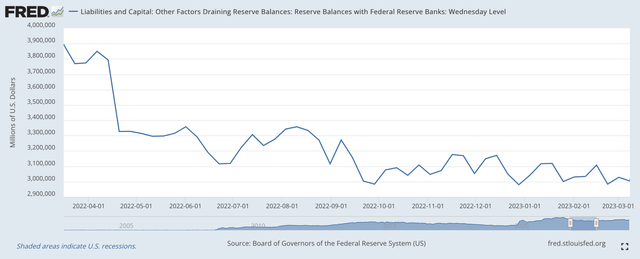

Reserve Balances with Federal Reserve Banks, which can be seen as a proxy for the excess reserves in the commercial banks, fell during this same period of time.

Reserve Balances With Federal Reserve Banks–3/16/2022 to 3/8/2023 (Federal Reserve)

This decline in commercial bank “excess reserves” was consistent with the Federal Reserve’s effort to “tighten up” on the banks’ reserve position.

Then in March 2023, the problems with the failing banks came up.

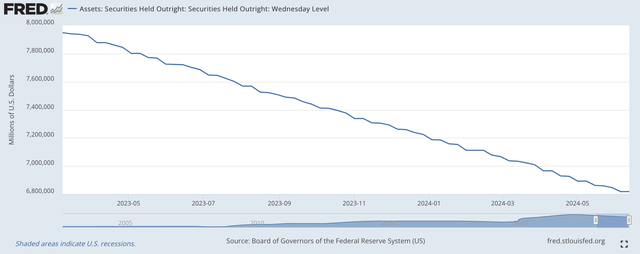

The Federal Reserve continued to reduce the size of the Fed’s securities portfolio.

Securities Held Outright–3/8/2023 to present (Federal Reserve )

However, the “excess reserves” in the commercial banking system did not follow the path, did not continue to decline, after this date.

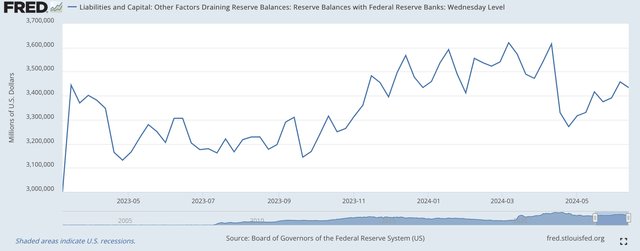

Reserve Balances with Federal Reserve Banks: 3/8/2023 to present (Federal Reserve)

Commercial banks hold more “excess reserves” now, after the Federal Reserve’s response to the problem of failing banks, than it did in early March 2023.

How did Federal Reserve officials achieve this shift?

Well, the use of Reverse Repurchase agreements fell. Whereas the reduction in the Fed’s securities portfolio resulted in a decline in bank reserves, the decline in the use of reverse repurchase agreements “freed up” reserves.

From March 8, 2023, to June 12, 2024, reverse repurchase agreements on the Fed’s balance sheet declined by $1,727.8 billion, or, by just over $1.7 trillion.

Federal Reserve officials continued to oversee the reduction in the size of the Fed’s securities portfolio, consistent with the policy of quantitative tightening, but, on the other hand, Federal Reserve officials “managed” the amount of excess reserves in the banking system through the use of the reverse repurchase agreements line item.

Federal Reserve officials, at the same time, continued their efforts to reduce the size of the Fed’s securities portfolio consistent with its policy of quantitative tightening, while managing commercial bank liquidity positions consistent with its effort to keep the banking system functioning.

Note: the quantities we are referring to are not “minor” movements.

The Fed’s securities portfolio declined by over $1.1 trillion during this period, while reverse repurchase agreements declined by over $1.7 trillion!

Commercial bank “excess reserves” rose by $430.5 billion.

So, the Federal Reserve was not, just blindly, letting securities run off from its portfolio. The Federal Reserve was still…and is still…managing bank reserve position to keep the banking system functioning.

Going forward, it should be noted that the Federal Reserve appears to be backing off from the suggestion it made in March that it might reduce the size of the monthly decline in its securities’ portfolio this June.

As I reported earlier, the Fed did not include information on a reduction in the size of its monthly reduction of its securities’ portfolio in the statement the Federal Open Market Committee produced after its meeting this past week.

So, for the time being, it appears as if the Fed will continue to reduce, on a monthly basis, its securities’ portfolio in amounts similar to what it has been doing over the past 27 months.

What Federal Reserve officials will do with commercial bank “excess reserves” is another story…to be determined by market conditions going forward.

The important “take away” from this discussion is that the Federal Reserve is not, just blindly, following a prescribed map going forward.

Yes, the Federal Reserve is reducing the size of its securities’ portfolio…and, in my mind, it needs to continue to do so…but is still watching over the banking system so that things don’t fall apart.

Going forward, Federal Reserve officials, as I have written about before, will be very cognizant of the upcoming presidential election and will try to keep from doing anything that might cause market disturbances or be called “political.”

I believe that the Fed has positioned itself well to avoid being accused of acting to support one political side or another. Chairman Powell will continue to lead the Fed in this way.

Market disturbances are another story. There remains a lot of uncertainty that investors must deal with. My point here is that Mr. Powell and the Federal Reserve will do just about anything it can that might call attention to its motives.

Read the full article here