The past decade has seen a robust evolution of technology with components such as radios, computers, and most importantly mobile phones weaving themselves into daily human lives. One company that comes to mind when I consider mobile communication and data analysis is FingerMotion, Inc. (NASDAQ:FNGR). Ever since it was founded in 2016, FingerMotion has revolutionized backend payment processing. It leverages a unique relationship with notable Chinese telecommunication providers such as China Mobile and China Unicom to offer solutions in mobile payment and recharge.

Thesis

Despite the 22.91% (YoY) drop in share price, FingerMotion looks to provide shareholder value boosted by its plan to expand its mobile top-up services and other data protection systems. The company is on a path to augment its recurring revenue streams and add new customers while moving toward the insurance space. FNGR’s revenue growth is also being supported by the abatement of Chinese lockdowns and technological growth into 2024 which will also help in raising shareholder value for the stock in the long run.

Financial developments

FingerMotion reported its Q2 FY2024 revenues at $9.3 million representing a 23.77% (QoQ) decline. However, the revenue had grown 86% (YoY) from $5 million realized in Q2 2023, The company’s prudent cost management saw it reduce its cost of revenues by 35.65% (QoQ) to $7.4 million thereby growing its gross profit by 157% (QoQ) and up to 350% (YoY).

For the six months ending on August 31, 2023, FNGR grew its revenue by 118% (YoY) to approximately $21.5 million from $9.84 million in 2022. Telecommunication products and services accounted for 98.9% of this revenue at $21.2 million, SMS & MMS business comprised 0.07% while Big data took up the remaining 1.06%. FNGR has significantly grown its Telecommunication business over the past year since it only accounted for 37% of the company’s revenue in FY 2022 while SMS messaging was the highest earner at 62%.

I believe FingerMotion is executing its growth strategy efficiently by expanding its product and service vertical. FNGR’s product offering includes “payment and recharge services, device subscriptions, data plans, mobile phones redemptions services for loyalty points and mobile protection plans”. The company’s sales have been growing in China since most mobile phone customers in the region pay their phone bills using third-party e-marketing websites. To process the payments, the e-marketers include JD.com, TMall Pinduoduo, etc. use government-licensed portals (such as the one offered by FNGR) to connect to the mobile telecommunication providers.

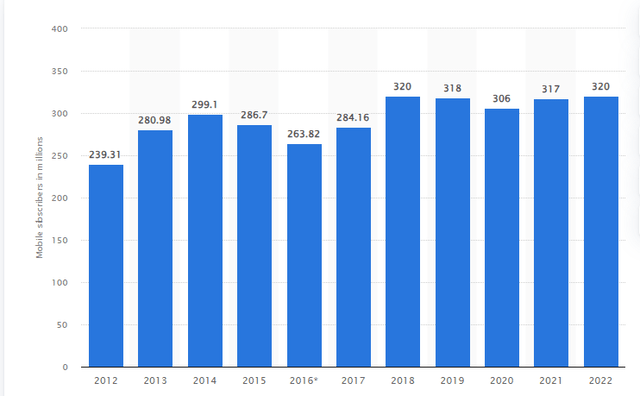

To say that FNGR is still in its infancy would not be far from the truth since it signed its volume-based agreement (through its Chinese contractual affiliate- JiuGe Technology) with China Mobile Fujian in May 2021. So, in less than 2 years, FNGR has almost doubled its revenues primarily by offering mobile payment/ recharge premium services to China Unicom and China Mobile customers or subscribers. China Mobile’s subscriptions as of 2022 stood at 320 million having grown its clientele by 33.72% from 2012 to 2022.

Statista

FNGR’s revenue in this segment also includes income rebates from the discounts offered through its platform, business-to-customer stores established on major e-commerce systems in China, and loyalty redemption partnership income.

Future Projects to Consider

FingerMotion’s second highest earner, Big Data launched Sapientus (in mid-2020), a data insights technology platform targeting the insurance, healthcare, government departments, and financial services segment. It leverages FNGR’s access to consumer data including demographics and geographical information that it uses to determine behavioral contexts and risk ratings.

I believe FNGR has a lot to offer in the insurance space seeing the rapid development of Fintech around the world. It will help in the company’s expansion drive outside the Chinese market. To put it in context, FNGR through Sapientus entered into a collaboration agreement with its first client, Pacific Life Re, a California-based Insurance Company in January 2021. Pacific Life has more than 37 clients in at least nine countries and has also recently expanded into Korea and China. Sapientus has a proprietary formula or an advanced algorithm with which it filters client data allowing it to develop a risk-rating concept. While announcing this agreement, Pacific Life Re indicated that it will specifically use Sapientus (for its Chinese market, due to FNGR’s presence there) to apply the “consumer behavioral insights to deliver insurance solutions to China.”

By the end of 2022, Sapientus had signed up another customer, global reinsurance company, Munich Re, a relationship that began in 2021 as a collaborative research alliance. While making this announcement, Munich Re’s Chinese General Manager of Life and Health stated,

We are launching a behavioral rating services platform with FingerMotion’s Sapientus following our initial collaborative research study. Leveraging our joint data resources and analytic expertise, we will continue to expand our data inventories and finesse the model algorithms. We look to apply what we have learned through our behavioral research and analysis to practical use for the benefit of our clients and insurance consumers in the China market,” said Eric Zhao, Munich Re China’s General Manager of Life & Health.”

Notably, the relationship between FNGR and insurance companies is tied toward developing and commercializing new products while mining behavioral patterns and using unique in-house actuaries. In the long-term, I believe Big Data Analytics will form a significant percentage of FNGR’s revenue, seeing its potential is research-driven in the fintech world. Sapientus has received 7 patents over the last 2 years from the National Copyright Administration of China (NCAC) to cover its proprietary algorithms and other insurance applications. The company is quickly shifting towards monetizing its Big Data Analytics infrastructure through Sapientus. I expect earnings to include commissions, profit-sharing strategies, and other partnership benefits that will develop in the future.

Financial Update

FingerMotion had about $4 million in cash and short-term investments in Q2 FY2024 compared to $2 million recorded a year ago. However, this cash has dropped 26% (QoQ) from $5.4 million recorded in Q1 2024. In August 2022, FNGR announced the closure of a $4 million funding agreement with Lind Global, proceeds that were to be used as working capital for the company through 2023. The fund manager was also awarded with warrants to buy another 3.5 million shares at $1.75. This move was expected to help FNGR introduce its device protection plan.

In the 12 months trailing to the quarter ending in August 2023, FingerMotion used up $9.7 million from operations. It also used up $0.1 million in Capex. However, the company generated $11.5 million from financing activities leaving it with $2 million (net change in cash).

As of August 31, 2023, FingerMotion’s working ratio stood at 3.3 (with its current assets at $20.1 million against current liabilities at $6.1 million). The company’s working capital into Q3 FY2024 is $14 million which is adequate to cover operational expenses for the remaining 2 quarters of the year.

Risk and Valuation

FingerMotion’s main operations are conducted in China with the company’s expansion projects still in their infancy. A disruption of the economic environment in this region will hamper growth opportunities for the company in the long run.

The payment processing space upon which FNGR operates is very competitive, especially in China. Also, being an American company, FingerMotion works with its Chinese contractual affiliate, JiuGe Technology to deliver services to China Mobile and China Unicom. It does not have a direct relationship with its Chinese clientele.

FingerMotion was slapped with a short-sellers report at the beginning of October 2023 that indicated an imminent dilution with a supposed target of $1. However, the company provided a rejoinder (including an SEC filing) maintaining its commitment towards accurate corporate governance and financial disclosure by the US SEC and Nasdaq rules. In regards to its “$300 million shelf registration (securities) and $25 million at-the-market agreement,” FNGR stated that it had the Form S-3 to guide in easy access to capital and prevent stock dilution.

FNGR’s forward price-to-sales ratio stands at 4.66 against the industry average of 1.06 (a difference of 335.24%). The price-to-book ratio is at 24.46 against the sector average of 1.54 (a difference of more than 1,490%). These figures show that the stock is overvalued and we may see some downside. However, I think that this situation may reverse once the company updates its business performance in H2 2024.

Bottom Line

I believe FingerMotion is in the infancy stages of growing its revenue after signing its first contracts in 2021. The company is steadily building its revenue streams while raising capital in a challenging environment to fund growth programs. According to me the shift from SMS messaging that had low margins to the mobile recharge/ device protection business and big data analytics is a masterstroke. I expect long-term marginal growth into FY 2025 as the company stabilizes its revenue. For these reasons, I recommend a buy rating for the stock.

Read the full article here