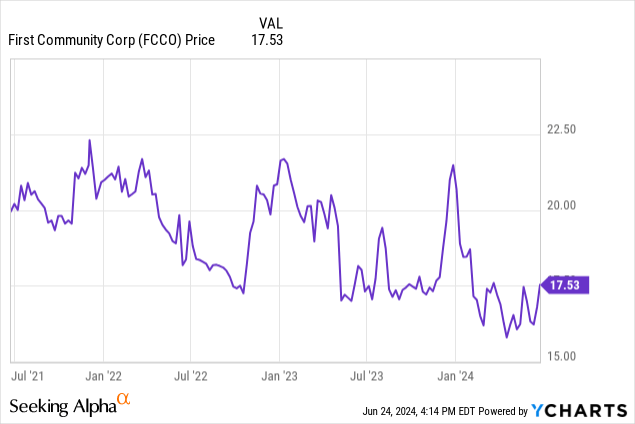

Introduction

First Community Corporation (NASDAQ:FCCO) is the holding company that owns the First Community Bank, which is active in South Carolina. In my previous article, I was very impressed with the bank’s ability to keep the loan loss provisions very low, mainly due to the fact that most of the loans are current. That situation hasn’t changed and as of the end of the first quarter, only 0.04% of the loans was categorized as ‘past due’. That being said, the bank’s earnings are under pressure due to a lower net interest income while the increase in salaries also has an impact on the bottom line result.

The bank remains profitable, but the earnings are under pressure

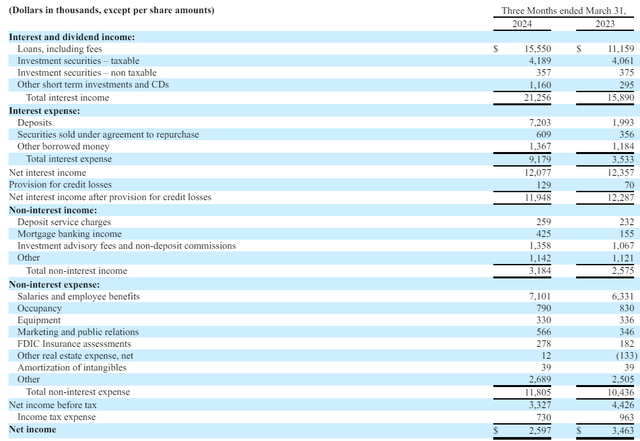

The net interest income remains a very important profit generator for any bank and that is definitely the case for a smaller local bank which obviously doesn’t really generate a whole lot of fees from customers nor from investment banking related activities.

In the first quarter of this year, the total interest income of FCCO did increase by approximately 34% to $21.3M but unfortunately the interest expenses more than doubled to $9.2M resulting in a net interest income of $12.1M. That’s just 2.5% lower than the $12.4M it recorded in the first quarter of 2023 so it’s safe to say the bank was able to keep the damage pretty limited.

FCCO Investor Relations

The bigger concern is the increasing net non-interest expenses. Whereas those net non-interest expenses came in at $7.9M in the first quarter of last year, First Community Corp. lost some ground in the first quarter of this year as the total net non-interest expenses increased to $8.6M. And as the income statement shown in the picture above indicates, this was almost entirely attributable to the higher salaries. Fortunately the investment advisory fees are also increasing and that is entirely attributable to the 10.3% increase in the total amount of assets under management compared to the final quarter of last year. I hope the bank can continue to grow its AUM as the related fee income could help to reduce the net non-interest expenses.

Fortunately the loan loss provisions remained pretty limited at just $0.13M (which is an increase compared to the $70,000 in Q1 2023 but the increase is small enough that it doesn’t really have a big impact in the greater scheme of things.

The pre-tax income was $3.3M which resulted in a net profit of $2.6M for an EPS of $0.34.

The bank currently pays a quarterly dividend of $0.14 per share which means it retains about 60% of its reported net profit. This represents approximately $6M in net income that is added to the balance sheet on an annual basis. That money is used to strengthen the balance sheet and to expand the loan book.

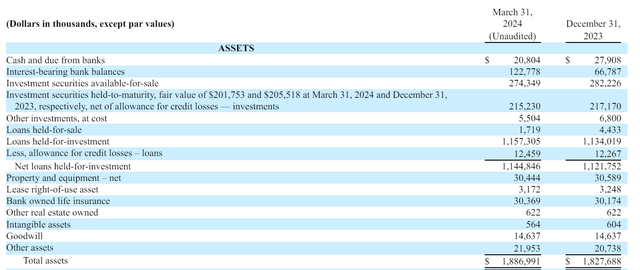

A closer look at the quality of the CRE-heavy loan book

Looking at the balance sheet, you can indeed see the total asset base has increased to $1.89B, up from the $1.83B as of the end of last year. The assets side of the balance sheet clearly shows there’s approximately $143M in cash and cash equivalents with an additional $274M in securities available for sale and $215M in securities held to maturity. The fair value of the securities HTM is approximately $202M, which means there is an implied unrealized loss of approximately $13.5M.

FCCO Investor Relations

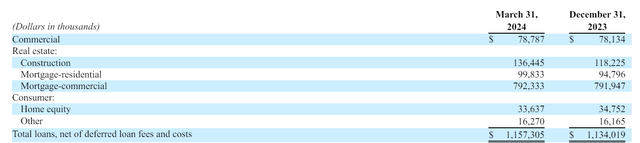

I’m more interested in the bank’s loan book, for two reasons. First of all, I am still pleasantly surprised by the low loan loss provisions. Secondly, in my previous article, I was also happy to see very few loans were registered as ‘past due’.

As you can see below, the vast majority of the loan book indeed consists of commercial real estate loans.

FCCO Investor Relations

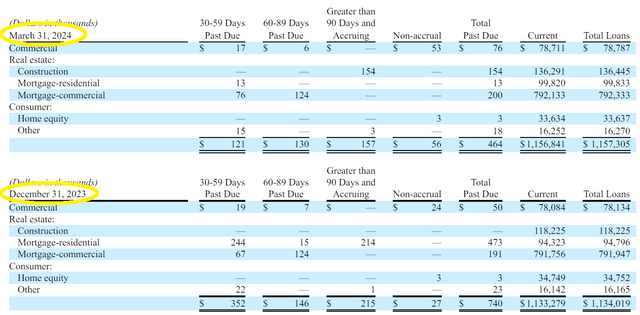

And once again, the bank’s loan book remains in excellent shape. As you can see below, only $56,000 of the loans were classified as no longer accruing, while the total amount of loans past due was just under $0.5M. That represents a negligible 0.04% of the $1.16B loan book. And of course even if all the loans default and the bank has to foreclose on the properties, this still doesn’t mean FCCO will lose the entire $464,000. Odds are the bank will recoup in excess of half that amount. And if you compare the Q1 2024 numbers with the year-end 2023 results, the total amount of loans past due actually decreases while the total size of the loan book actually increased.

FCCO Investor Relations

Needless to say it looks that although the bank’s loan book is overweight in commercial real estate, FCCO appears to be knowing what it’s doing as the vast majority of the loan book is performing as expected.

Investment thesis

At the end of the first quarter, the bank’s tangible book value increased to $15.51 per share which means the share price is currently trading at a premium of approximately 14% to the tangible book value per share. I don’t mind paying a small premium over book, but considering the earnings of the bank are still under pressure, I don’t really feel like paying a double digit multiple to the earnings.

I am still impressed with First Community’s strong loan book where defaults appear to be rare, even in the CRE segment. I will be keeping an eye on the bank’s performance but I am moving to a ‘hold’ due to the relatively weak earnings result and the premium to the tangible book value.

Read the full article here