Introduction

As part of the energy transition mega trend, clean energy via solar is an obvious choice to assume continued high growth. However, the sector has been volatile with production dominated by Chinese-based PV (photovoltaic) panels which may be more focused on capacity/scale growth than profitability and have driven PV prices to the point that most US manufacturers can’t compete. Some may call this a well-functioning free market, others dumping, but I prefer to analyze the situation objectively to identify investment opportunities. First Solar (NASDAQ:FSLR) is a market favorite, with substantial gains due to the impact of the IRA (Inflation Reduction Act) and more recent import tariff barriers. Based on consensus data, the stock is near full value.

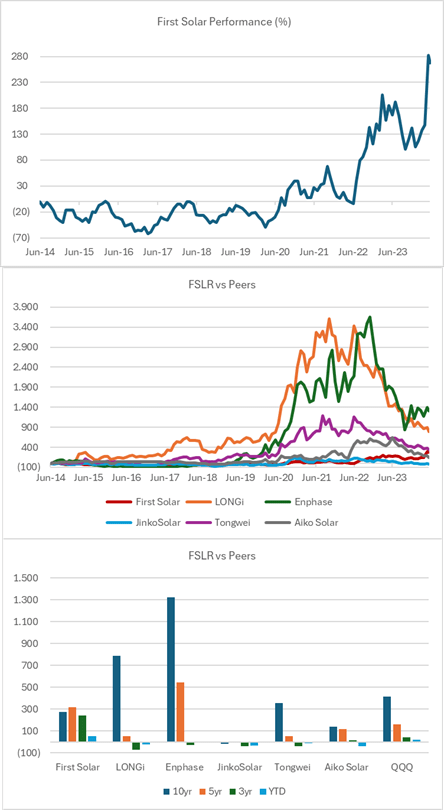

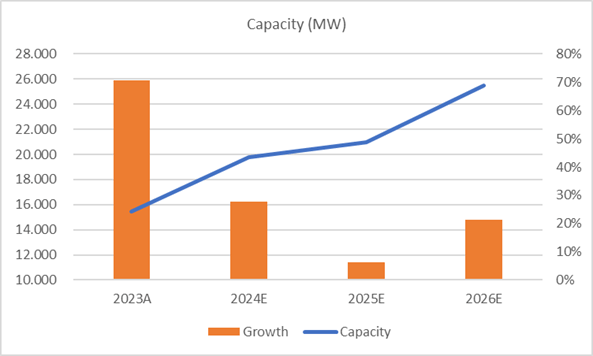

Performance

The solar energy sector has had considerable volatility and bubbles, as seen in the price performance charts below. FSLR did poorly from its IPO in 2014 to mid-2022 when IRA came into effect. The Chinese stock Longi Green and Enphase Energy (ENPH) had the largest gains during the pandemic years and then fell back to earth. The sector has grown capacity faster than demand, and that has resulted in lower prices and margins.

Created by author with data from Capital IQ

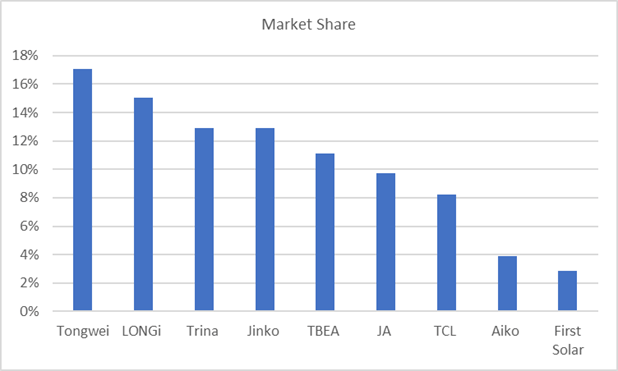

What is First Solar

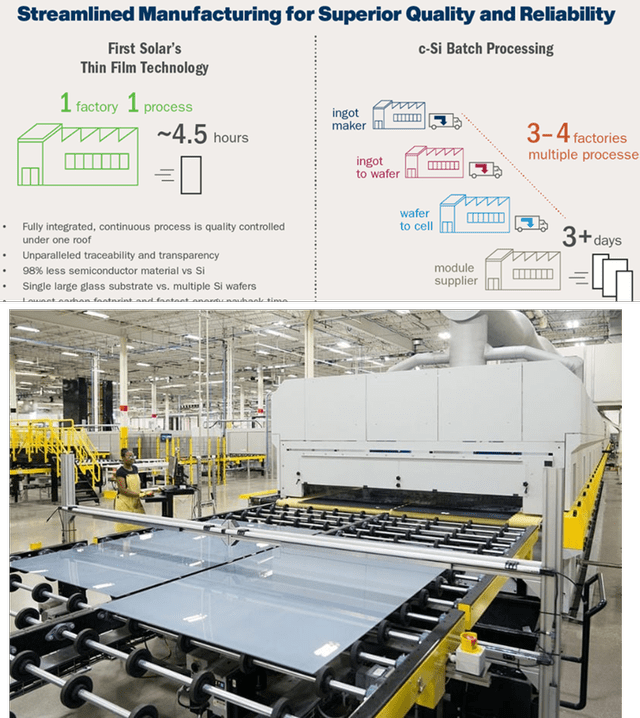

The company is one of a few remaining US-based manufacturers of PV cells with a distinct technology, its “panels” are thin film made from Cadmium Telluride (CadTel). According to reviews, the main differences vs. traditional crystal panels are that they are lightweight, easy to apply, have better resistance but produce lower loads, and require more area. FSLR grew capacity (measured in Mega Watts MW) by 70% in 2023 and is planning to spend US$3bn through 2026 to expand capacity by 50%.

Capacity (Created by author with data from FSLR)

First Solar

Solar Panel Market

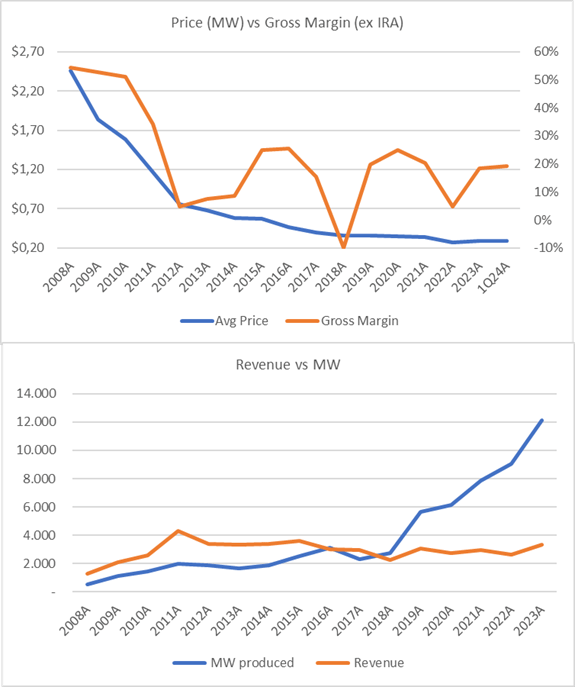

Despite the strong demand dynamics, the solar equipment sector, dominated by Chinese companies, has had significant volatility due to rapid capacity expansion focused on improving manufacturing scale. This has led to lower prices and, in the case of FSLR, a sharp drop in margins. Since 2008 prices have declined from around $2.5MW to $0.29MW while gross margin fell from 50% and fluctuated between 0% and 20% since 2011. At the same time, FSLR grew capacity at a 23% CAGR vs revenue growth of 7% which is a disastrous return on capital (ROIC).

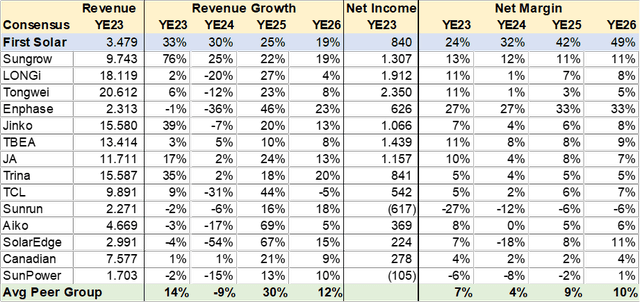

Consensus for the peer group suggests that Chinese companies are in a difficult environment, with revenue declining over 10% and net margins falling to under 5% before an estimated recuperation in 2025. This is in stark contrast to FSLR and Enphase that benefit from IRA tax credits and import barriers.

Market Share by Revenue 2023 (Created by author with data from Capital IQ)

Peer Comps (Created by author with data from Capital IQ)

Production, Prices & Margin (Created by author with data from FSLR)

Growth Turbocharged by IRA

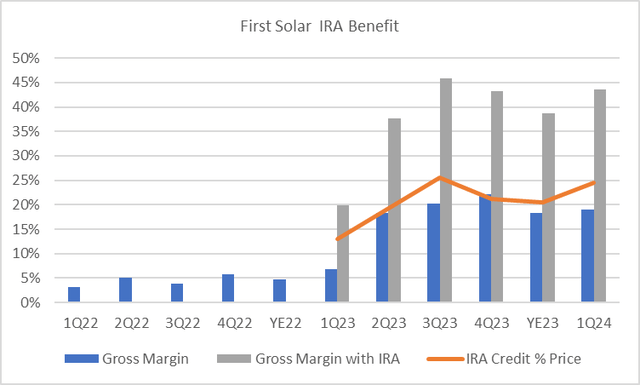

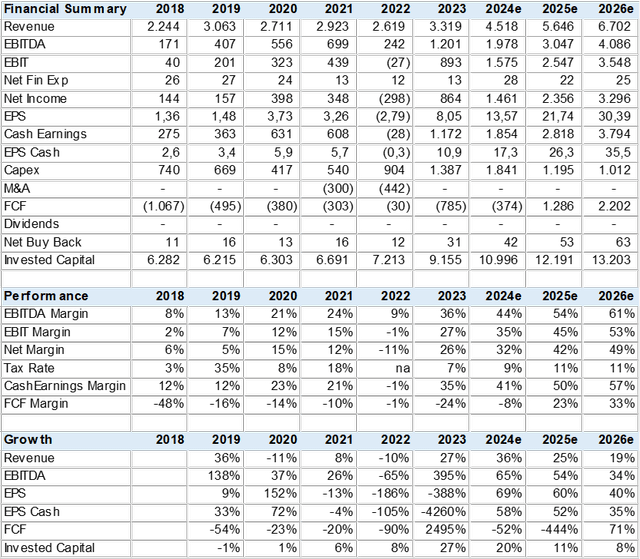

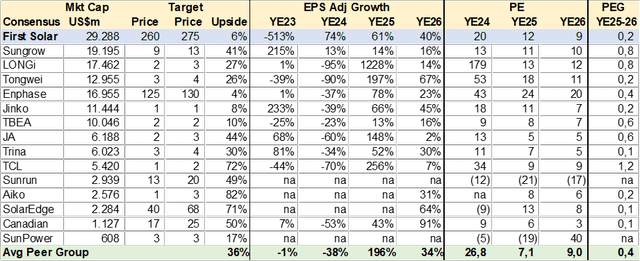

I gathered consensus forecasts from 29 analysts to gauge FSLR growth and profitability metrics. The market has incorporated considerably positive numbers with revenue growth of over 20% accompanied by margin increases that led to EPS growth of over 60% in the YE24-25 period. Much of this strength is due to the IRA tax credits that may add US$1bn to EBIT and earnings, according to the 1Q24 results report. In the chart below, I illustrate that around 20% of revenue has been “added” to EBIT since the implementation of IRA, which, is a tax credit on production. On the negative side, the company’s capacity expansion and capex drive FCF negative in 2024. Overall, the market estimates are aggressive and a function of a multi-year order book (78GW or 4yr production) dependence on IRA tax credits and import barriers for stable pricing.

Created by author with data from FSLR

Consensus Forecast (Created by author with data from Capital IQ)

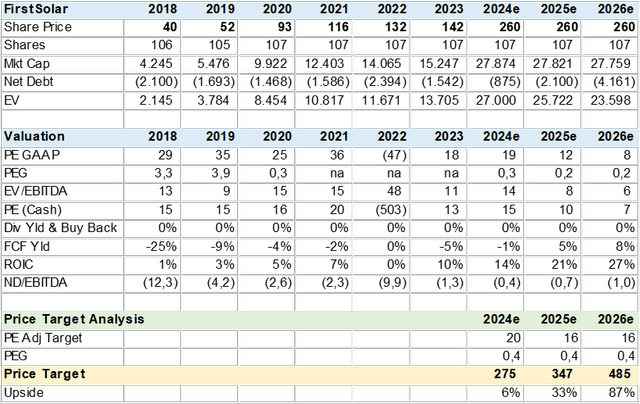

Valuation

First Solar is a cheap stock with a relative valuation of 0.3x PEG (PE to EPS growth). The current consensus price target of US$275 backs into an implied target PE of 20x and a PEG of 0.4x and provides a low upside potential. However, if I apply this PEG to 2025 and 2026 estimates the price target increases to US$347 +33% to YE25.

Given the high growth rate, investors may believe that a higher multiple is warranted, and normally, I would agree. Unfortunately, this sector has been discounted by the market, due to its poor earnings visibility, dependence on government subsidies, and protection that I believe carries political risks. Perhaps a sustained period of stability may lead to better valuations.

Consensus Valuation (Created by author with data from Capital IQ)

Created by author with data from Capital IQ

Conclusion

I rate FLRS a Hold. I see two problems with the stock. The first is political risk to earnings, given that about half of the company’s margins are derived from tax credits (IRA) while demand growth is boosted by trade barriers. The second dilemma is valuation, while seemingly cheap at 0.3x PEG (19x PE) this incorporates the sector’s volatility and poor ROIC (absent government subsidies). Perhaps as FLSR delivers on guidance and breaks with past earnings uncertainty, valuations can improve.

Read the full article here