Investment Thesis

Fortune Brands Innovations (NYSE:FBIN) is expected to benefit from easier Y/Y comps in the second half of 2023. Further, the recovering demand across its end markets with the improvement in the new residential construction market and normalizing inventory levels in the Repair and Remodel channels should help sales. The continued focus on high-growth categories and accretive M&As should also help drive revenue growth. Margins are expected to benefit from volume leverage and initiatives like productivity improvement, nearshoring and site consolidation. The valuation is also reasonable. This, coupled with promising growth prospects, makes FBIN stock a buy.

Revenue Analysis and Outlook

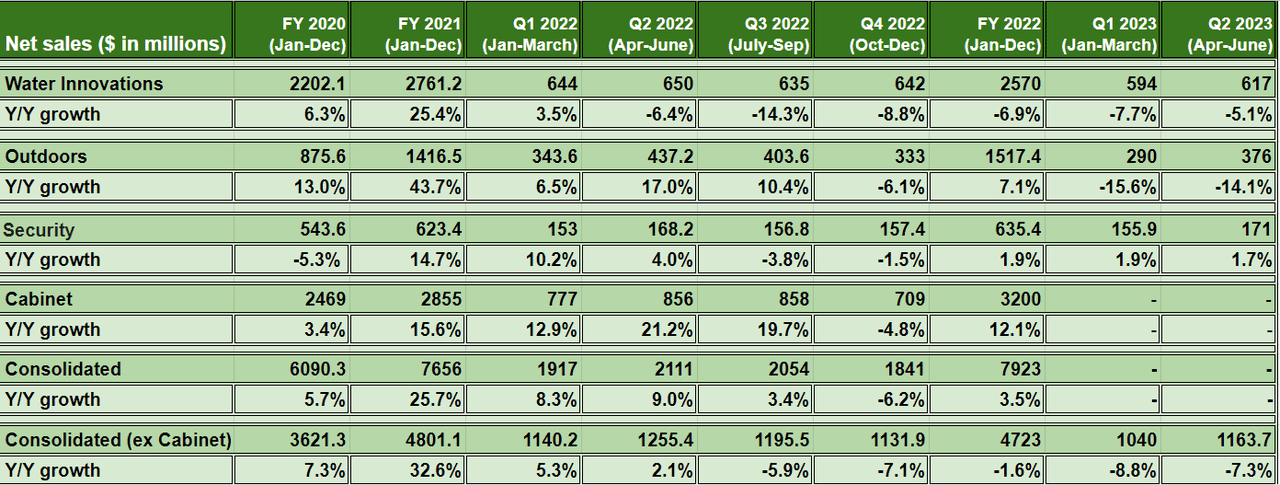

Earlier this year, I wrote a bullish article about FBIN. At that time, the company was facing inventory destocking from its channel partners, and I predicted that the destocking would likely bottom in the first half of FY23. The company has reported its 1Q23 and 2Q23 results since then, and management talked about normalizing inventory levels on its 2Q23 conference call. While revenue declined 7.3% YoY 2Q23, the company has shown sequential improvement in this quarter as compared to 8.8% YoY decline in 1Q23.

In the second quarter of 2023, the Water Innovations segment’s sales declined 5.1% Y/Y to $617 million due to the lower sales volume primarily in the U.S., which more than offset the volume increase in China due to the non-recurrence of 2022 COVID lockdowns, the $13 million contribution from the Aqualisa acquisition, and benefits from pricing. In the Outdoors segment, sales decreased 14.1% Y/Y to $376 million, driven by lower sales volume for the door and decking products, partially offset by benefits from pricing. Meanwhile, the Security segment’s sales increased 1.7% Y/Y to $171 million, driven by the benefits from pricing and robust growth in the commercial safety business, which more than offset the lower sales volume in retail locks and retail safe businesses. On a consolidated basis, the net sales declined 7.3% Y/Y to $1163.7 million due to lower sales volume in the U.S., partially offset by the benefits from pricing and $13 million contribution from the Aqualisa acquisition.

FBIN’s Historical Revenue Growth (Company data, GS Analytics Research)

Looking forward, I believe FBIN sales should benefit from easing comps, improving new housing starts and strong Repair and Remodel fundamentals. Further strong execution, which is driving above market growth, and M&As should also drive growth.

If we look at FBIN revenues, they posted steep correction starting back half of FY22 as that is when inventory destocking in its channels started. Compared to 5.3% Y/Y growth in 1Q22 and 2.1% Y/Y growth in 2Q 22, the company’s sales declined 5.9% Y/Y in Q3 22 and 7.1% in Q4 22. So, as we enter the second half of this year, the company’s revenues should see easier Y/Y comparisons.

Further, the company’s end markets are also improving. The new residential housing starts data from July showed both Y/Y as well as sequential improvement. The long term fundamentals of the housing market are really strong thanks to significant underbuild of new homes post the great housing recession of 2008. This is helping the strong trend in the market despite high interest rates. I expect further acceleration once the interest rate cycle reverses.

One thing which is helping the company in its new construction business is its exposure to large production builders as opposed to custom home builders. The large production builders are seeing strong demand compared to others as they are focused on offering affordable homes. Higher home prices are forcing homebuyers to look for affordable options driving higher than industry growth for production builders and FBIN’s exposure to them is helping the company’s growth.

The Residential Repair and Remodel market is also seeing strong trends with record high levels of home equity and aging housing stock. Further after almost four quarters of inventory destocking the channel inventory is lean and the company should benefit from it.

The company also has a history of strong execution and posting above market growth. I have discussed this in my previous article. According to management, the company’s growth outpaced the end market growth by 50 bps last quarter and I expect this outperformance to continue in the coming quarters as well.

I believe easing comps together with strong end markets and execution should help the company return to Y/Y organic growth in the back half of this year. This coupled with the recent acquisitions of ASSA ABLOY’s Emtek and Schuab as well as August and Yale brands make me optimistic about the company’s growth prospects

Margin Analysis and Outlook

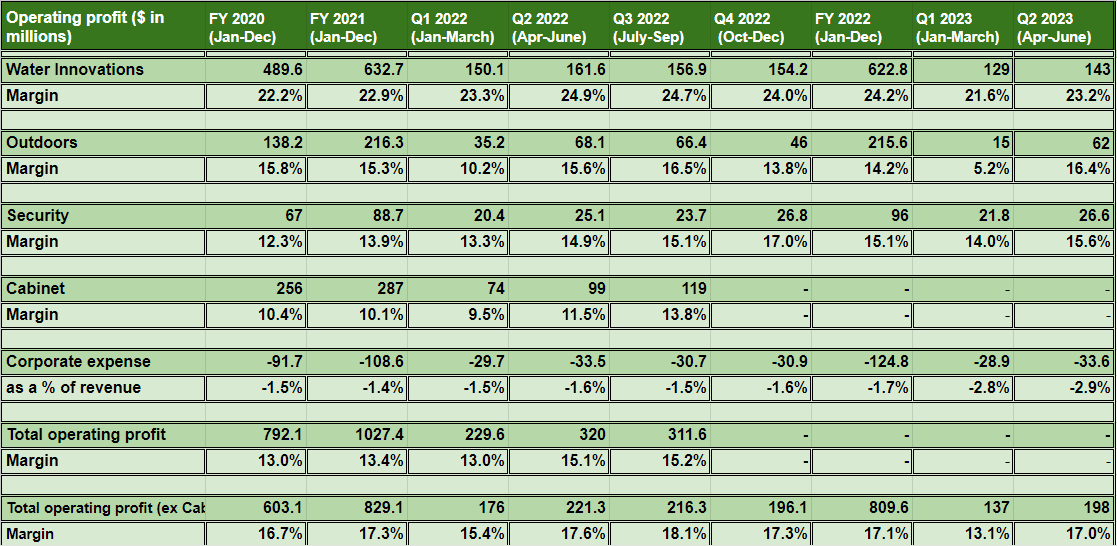

During Q2 2023, the company’s operating margin declined 60 bps Y/Y to 17% due to production inefficiencies and under absorption of fixed costs related to inventory destocking, which more than offset the benefits from cost savings and raw material cost deflation. On a segment basis, the Water Innovations segment witnessed a 170 bps Y/Y margin decline due to volume deleverage, partially offset by the benefits from pricing and productivity gains. The performance of the Outdoors segment was strong and despite revenue decline, the operating margin in the Outdoors increased by 80 bps Y/Y. The Security segment margin increased 70 bps Y/Y, respectively, driven by sales leverage, benefits from pricing, and plant production efficiencies.

Historical margin performance (Company data, GS Analytics Research)

Looking ahead as volume recovers in the back half of this year, the company’s margin should recover, benefitting from volume leverage. Further, while the first half margins were impacted from production curtailment, its impact on the back half of this year should be much less. Overall management is guiding for 16% to 16.5% operating margins for the full year, implying the second half of margins will be better than the first half. In the medium to long term, management is targeting 300 -500 bps operating margin improvement through initiatives like productivity improvement, nearshoring, site consolidation etc. Overall, I am optimistic about the company’s margin growth prospects ahead.

Valuation & Conclusion

FBIN is currently trading at 18.15x FY23 consensus EPS estimates of $3.87 and 15.79x FY24 consensus EPS estimates of $4.45. The company has historically traded at a 5-year average forward P/E of 15.74x.

While the valuation on FY23 consensus estimates (which is bottom of the cycle) is higher compared to its historical averages, the company’s P/E on FY24 consensus estimates is almost in line with historical averages. One thing investors should note is that late last year, the company divested its kitchen cabinet business which was more cyclical due to the big-ticket nature of its product. That business usually gets a low valuation multiple. So, after the divestiture, the rest of the company deserves higher P/E multiple. I believe the stock can continue to trade at a P/E in the high teen range. If we apply 18x P/E multiple to FY24 consensus EPS estimate of $4.45, we get a target price of ~$80 which implies ~13.86% upside over the next year. This coupled with ~1.32% yield takes the total return to mid teens range over the next year which is attractive. Further, the company has good medium-to-long-term growth prospects, supported by factors such as pent-up demand in the housing market, strength in R&R channels, synergy benefits from M&As, and productivity gains. With promising growth prospects and a reasonable valuation, I have a buy rating on the stock.

Read the full article here