Introduction

I like to invest in oil and gas royalty companies, as it is one of the most convenient ways to have exposure to the prices of those commodities. Royalty companies pay an upfront fee to acquire a royalty, but are not on the hook for any of the capex commitments or investments executed by the operator. Basically, the main risk for royalty companies is the operator doing a poor job.

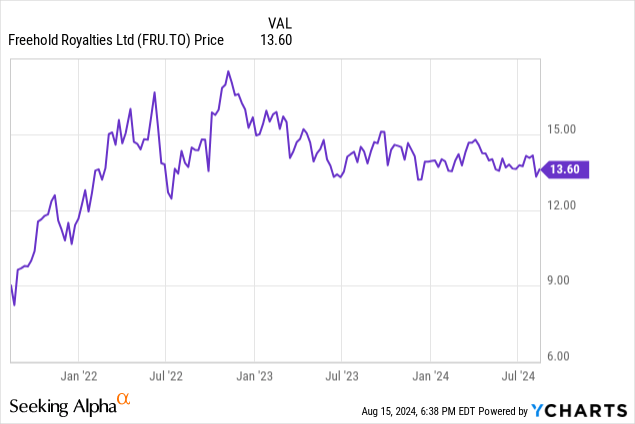

Freehold Royalties Ltd. (OTCPK:FRHLF, TSX:FRU:CA) is one of my favorite oil and gas royalty companies as the company combines attractive cash flows from its American and Canadian royalties with a generous dividend at an acceptable payout ratio. As I haven’t had my finger on the pulse yet for the past two quarters, I think this is an opportune moment to have another look at Freehold.

The beauty of royalty companies: a very high conversion of revenue into free cash flow

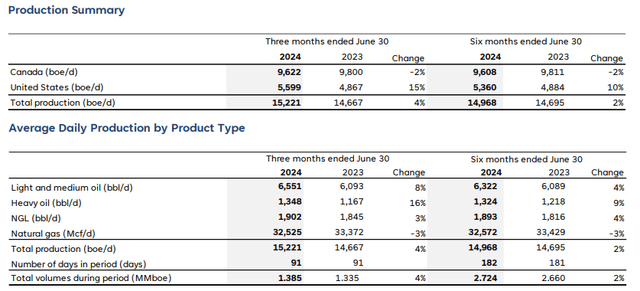

In the second quarter of the year, Freehold’s attributable production increased to 15,221 barrels of oil-equivalent per day, with approximately 63% of its attributable production coming from its Canadian assets.

Freehold Investor Relations

About 40% of the oil-equivalent production comes from light and medium oil, while heavy oil (which trades discounted to light oil) represents less than 10% of the oil-equivalent output. Natural gas represents about 36% of the attributable production, and it goes without saying the low natural gas price isn’t working in Freehold’s favor.

In fact, as you can see below, the average realized natural gas price was abysmal. The company received just C$0.82 per Mcf mainly due to the weak natgas prices in the USA as the average received price in Canada was slightly higher at C$0.90.

Freehold Investor Relations

Fortunately, the strong oil and NGL prices mitigated the impact of the low natural gas price. In fact, despite making up about 36% of the oil-equivalent production rate, natural gas contributed just 3% to the total royalty revenue, exactly due to the very weak pricing.

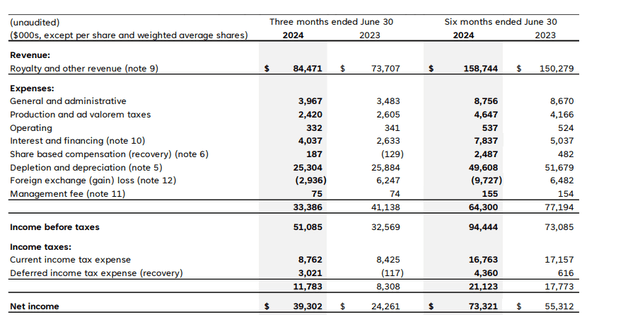

The total revenue was approximately C$84.5M, and as you can see below, the operating expenses are relatively low and predominantly consist of the depreciation and depletion expenses related to the assets Freehold owns a royalty on.

Freehold Investor Relations

This resulted in a pre-tax income of C$51.1M (boosted by a C$2.9M FX gain versus a C$6.25M FX loss in the second quarter of last year) and a net profit of C$39.3M. With just under 151M shares outstanding, the EPS came in at C$0.26 per share, and this brought the H1 2024 EPS to C$0.49.

Keep in mind, the depletion and depreciation expenses are non-cash expenses. Sure, the company will have to buy new assets to counter the impact of depletion on the existing assets. That’s why it is important to generate a strong operating cash flow, as that OpCF can be used to buy new assets.

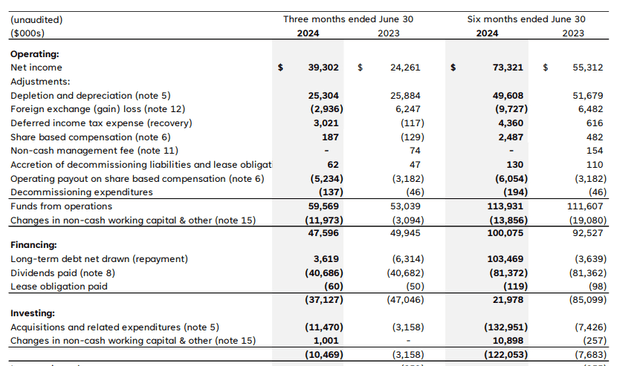

As the cash flow statement below shows, Freehold Royalties reported a total operating cash flow of C$59.6M before changes in the working capital position. And apart from an acquisition, there was no capex incurred during the quarter (which of course makes sense considering Freehold is a royalty company and does not need to contribute any capital to the exploration and development plans of the operators).

Freehold Investor Relations

Divided over the 150.7M shares that are currently issued and outstanding, the net FFO per share came in at C$0.395/share, which is C$1.58 per share on an annualized basis.

Freehold Royalties is currently paying a dividend of C$0.09 per share per month. Based on the Q2 FFO result, this means the payout ratio is approximately 68%. This also means that in any given quarter, the company retains approximately C$18M in cash, which is currently used to reduce the net debt (and which could be used for additional acquisitions).

Investment thesis

I own Freehold Royalties to have exposure to the oil and gas prices, but I obviously also like the monthly dividend payments. The C$0.09 per month is well-covered, and Freehold has a good history of acquiring new assets at acceptable prices to counter the impact of depletion. I don’t mind seeing the company using the incoming cash flow to reduce its net debt, and hopefully, it will be able to do new deals in the future.

I have a long position in Freehold Royalties.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here