ETF Overview

Fidelity MSCI Consumer Staples Index ETF (NYSEARCA:FSTA) owns a portfolio of mostly large-cap consumer staples stocks in the U.S. The fund is defensive in nature but still has significant downside risk due to its already rich valuation and that during economic downturns, valuation compression is still quite possible. Over the long run, FSTA’s growth profile is also weaker than the broader market. Therefore, its risk and reward profile does not appear to be attractive right now.

YCharts

Fund Analysis

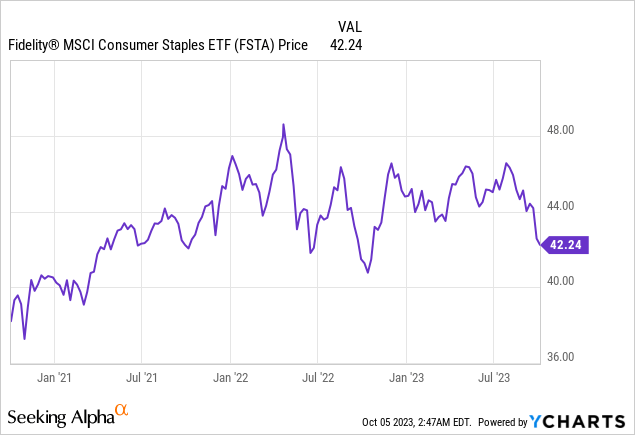

FSTA held up well in 2022 but its fund price appears to be weakening in 2023

Unlike many equity funds that suffered disastrous decline in 2022, FSTA has performed relatively well. The fund has declined by only 4% in 2022. In contrast, the S&P 500 index declined by 19.5% in the same year. However, things have reversed somewhat in 2023. FSTA has declined by another 5.7% year-to-date. In contrast, the S&P 500 index still rose 11% year-to-date despite the recent market correction. Overall, FSTA held up well in 2022, but appears to be weakening in 2023.

YCharts

FSTA offers better downside protection than the broader market

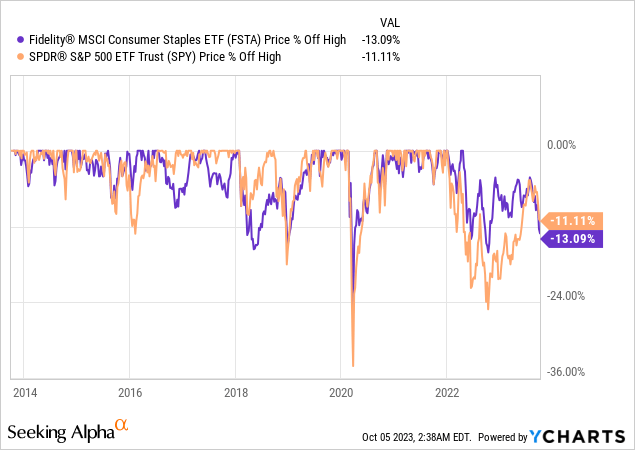

Consumer staples is defensive in nature. Therefore, they tend to perform relatively better during market turmoil. We have observed this in 2022. This is because these companies sell essential products used by consumers. Even during economic downturns, people still need to use these essential products. Because of its defensive nature, FSTA’s stock price tends to perform better than the broader market in economic downturns. However, it can still decline significantly. As can be seen from the chart below, FSTA’s fund price declined by about 26% in the initial COVID-19 outbreak in 2020. In contrast, the S&P 500 declined by nearly 35%.

YCharts

Weaker growth profile than the broader market

While FSTA is a good defensive fund to own during economic downturns, stocks in its portfolio generally do not have strong growth profiles relative to the broader market. This is not hard to understand as consumption of household goods, food, beverage, hygiene products, etc. tend to be very stable. There is only so much one person can consume these products every day.

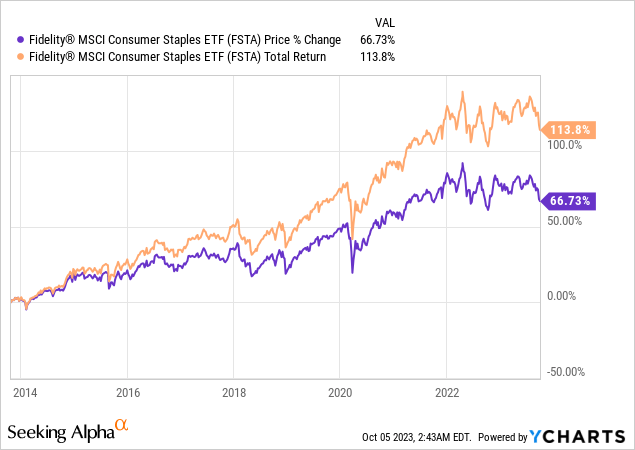

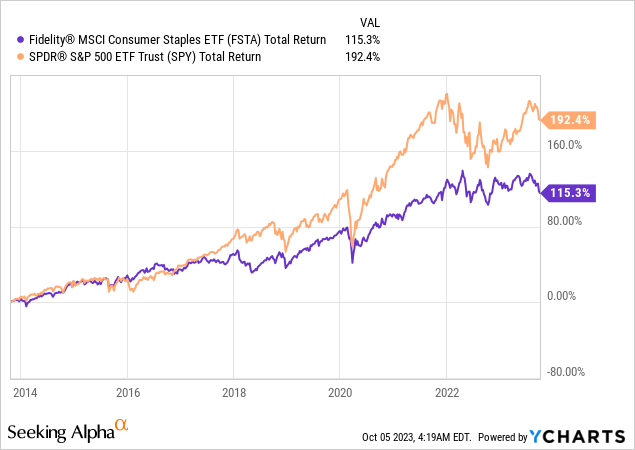

According to Morningstar, stocks in FSTA’s portfolio have historical earnings growth of about 7.5%. This mid-single digit growth may look not bad, but the number was significantly below the S&P 500 index’s 14.9%. This weaker growth profile has resulted in its weaker long-term total performance. As can be seen from the chart below, its total return of 115.3% since its inception in 2013 was significantly lower than the S&P 500 index’s 192.4%.

YCharts

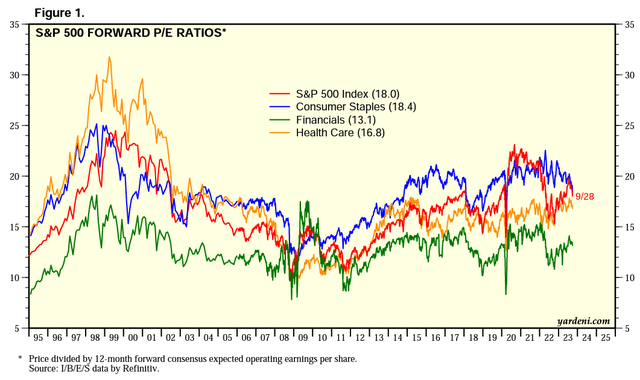

FSTA’s valuation has declined but still appeared rich

Since FSTA’s portfolio consists of mostly large-cap consumer staples, it is appropriate to check the valuation of consumer staples stocks in the S&P 500 index to gauge the portfolio’s valuation. This is because the S&P 500 index only consists of large-cap stocks. Therefore, FSTA and consumer staples sector in the S&P 500 index has significant overlaps. As can be seen from the chart below, the forward P/E ratio of consumer staples sector in the S&P 500 index is currently about 18.4x (blue line). While this valuation has come down from the high of 22x reached in 2021/2022, the current valuation of 18.4x is still towards the high end of its historical average in the past two decades. Although FSTA has better downside protection than the broader market due to the portfolio’s defensive nature, we may still see valuation compression during market turmoil. As can be seen from the chart below, the forward P/E ratio of consumer staples sector compressed significantly during the Great Recession in 2008/2009 and during the initial outbreak of the pandemic in 2020. In other words, there may still be some downside risks.

Yardeni Research

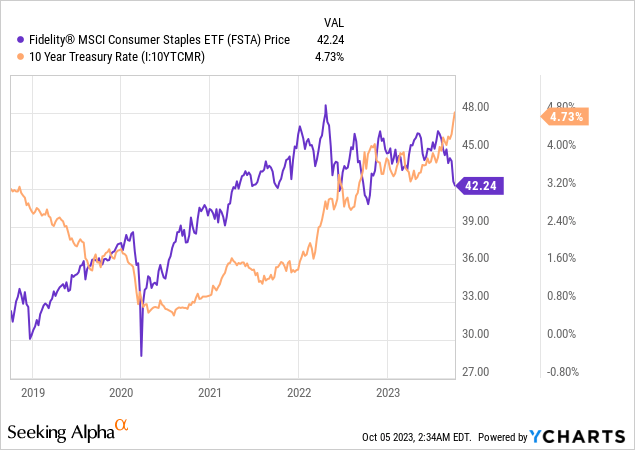

FSTA tend to be inversely correlated to treasury rate

Another interesting item about FSTA is that its fund price tends to be inversely correlated to the treasury rate. As treasury rate declines, FSTA’s fund price tend to increase. As treasury rate rises, FSTA’s fund price tend to be suppressed or even declined.

YCharts

Is it time to invest in FSTA?

We believe the U.S. economy may soon be heading for a recession due to the Federal Reserve’s higher for longer rate policy to combat inflation. As discussed in the previous section, this high-rate environment has already suppressed FSTA’s fund price. If inflation is proven to be very sticky and the Federal Reserve needs to raise the rate higher, we believe FSTA’s fund price will likely fall. In addition, higher for longer rate environment will likely tip the economy over to a recession. This will result in valuation compression of FSTA’s fund price. Hence, we see downside risks. Looking beyond the near-term possible recession, the fund may rebound if the economy gradually moves out of the recession. However, given its already rich valuation, upside potential may also be limited.

Investor Takeaway

FSTA may offer better downside protection than the broader market in economic downturns. Its valuation appears to be rich already. Therefore, it is prone to downside risk in an economic downturn. FSTA’s still rich valuation also means that there may not be much upside from this level even if macroeconomic condition improves. In addition, the fund’s long-term growth profile is weaker than the S&P 500 index. Therefore, FSTA’s risk and reward profile is not attractive at the moment. Investors may want to stay on the sidelines.

Read the full article here