Elevator Pitch

My investment rating for Full Truck Alliance Co. Ltd. (NYSE:YMM) stock is a Buy.

Earlier, I touched on Full Truck Alliance’s Q4 2023 financial performance in my prior write-up published on March 10, 2024. This latest article reviews YMM’s Q1 2024 financial results and analyzes the company’s shareholder capital return.

I have decided to upgrade my rating for YMM from a Hold to a Buy. Full Truck Alliance’s potential shareholder yield is attractive, and the company’s recent quarterly metrics exceeded expectations.

First Quarter Results Surpassed Expectations

YMM disclosed the company’s Q1 2024 financial numbers with a press release issued on May 21.

Full Truck Alliance’s key financial metrics for the most recent quarter turned out to be much better than what the sell side had expected. The company’s actual first quarter top line and normalized earnings per ADS (American Depositary Share) in local currency or RMB terms beat the analysts’ consensus projections by +6% and +46% (source: S&P Capital IQ), respectively.

Revenue for YMM increased by +33% YoY to RMB2,268.7 million in the first quarter of the current year. Also, the company’s non-GAAP adjusted EPS rose by +50% YoY from RMB0.48 in Q1 2023 to RMB0.72 for Q1 2024.

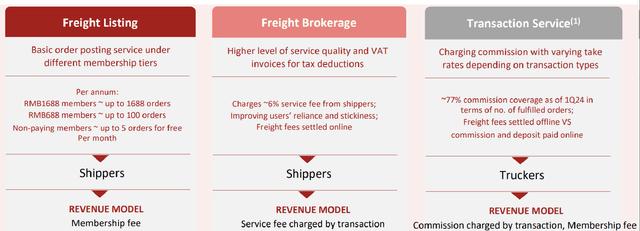

The strong growth in Full Truck Alliance’s high-margin transaction service revenue stream was the most important driver of its above-expectations results. In its results press release, YMM noted that its transaction service revenue is derived from the “monetization” of “truckers related to our freight matching service.”

YMM’s transaction service revenue jumped by +62% YoY to RMB691.0 million in the first quarter of 2024. In contrast, Full Truck Alliance’s freight listing service revenue and freight brokerage service revenue expanded by relatively more modest growth rates of +7% YoY and +25% YoY, respectively for Q1 2024.

YMM’s Key Revenue Streams At A Glance

Full Truck Alliance’s Investor Presentation Slides

At the company’s Q1 2024 earnings call, Full Truck Alliance highlighted that its “revenue mix continued to improve as transaction service revenues” grew. This implies that YMM’s transaction service revenue stream boasts relatively higher margins than its other revenue streams like freight brokerage service and freight listing service.

YMM highlighted at its most recent quarterly results briefing that the company “rolled out the commission model in 30 new cities” to 234 cities in total and utilized “big data analytics” to “identify high-quality order postings.” This explains why the company was able to achieve a substantial increase in transaction service revenue in the latest quarter. Moving ahead, Full Truck Alliance is likely to report a similarly good set of results for the second quarter with these actions it has taken to boost transaction service revenue.

YMM has guided for a +30% growth in its top line to RMB2,685 million (mid-point of guidance) in Q2 2024, which was also +4% higher (source: S&P Capital IQ) than the prior consensus Q2 revenue estimate.

Stock Offers An Attractive Forward Shareholder Yield

Full Truck Alliance boasts an appealing potential shareholder yield of 4.5% based on my calculations, which is a key investment merit for the stock.

YMM distributed a maiden dividend per ADS of $0.1444 for FY 2023 on April 19, 2024. The stock’s consensus FY 2024 dividend yield is 1.3% as per the consensus current fiscal year dividend forecast of $0.12 per ADS. The $0.12 dividend per ADS forecast for the current year assumes a reasonably conservative dividend payout ratio of 24%.

Separately, the company has approximately $296 million remaining from its current share repurchase authorization, which expires on March 12, 2025. Assuming Full Truck Alliance completes its buyback program by March next year, the stock’s forward buyback yield (buybacks divided by market capitalization) will be around 3.2%.

Full Truck Alliance spent a meaningful $200 million on share buybacks for the one-year period between March 3, 2023 and March 6, 2024. Also, YMM stressed at the company’s latest quarterly earnings briefing that it will “continue to evaluate share repurchases as part of our comprehensive shareholder return initiatives going forward.” YMM’s share buyback track record and its recent management comments provide support for the assumption that the company will complete its existing share repurchase plan by March next year.

Therefore, I estimate that Full Truck Alliance’s potential shareholder yield is 4.5%, which is the sum of the company’s dividend yield (1.3%) and buyback yield (3.2%).

Key Risks

YMM’s future financial results and shareholder capital return are expected to be the main factors affecting its stock price performance.

Expectations regarding Full Truck Alliance’s future growth are high, following the company’s robust top-line expansion and revenue beat for the recent quarter. A significant slowdown in YMM’s top-line growth in the coming quarters due to a weak Chinese economy or execution issues might lead to a substantial pullback in the company’s share price.

On the other hand, YMM’s actual shareholder yield could be less enticing, if the company’s dividend payout ratio is lower than expected and the pace of buybacks is slow.

Final Thoughts

I have turned bullish on Full Truck Alliance. My opinion of YMM’s recent financial performance and shareholder capital return outlook is favorable, and this has prompted me to raise my rating for the stock to a Buy.

Also, YMM is now valued by the market at an undemanding Price-to-Earnings Growth or PEG multiple of 0.61 times. This is based on Full Truck Alliance’s consensus next twelve months’ normalized P/E ratio of 17 times and the company’s consensus FY 2024-2026 normalized EPS CAGR estimate of +28% as per S&P Capital IQ data.

Read the full article here