Holding gold mining stocks as opposed to having a direct exposure to the precious metal has been a large disappointment over the past year. With gold hitting a new all-time high, investors were rightfully so, expecting that mining stocks would deliver much higher returns.

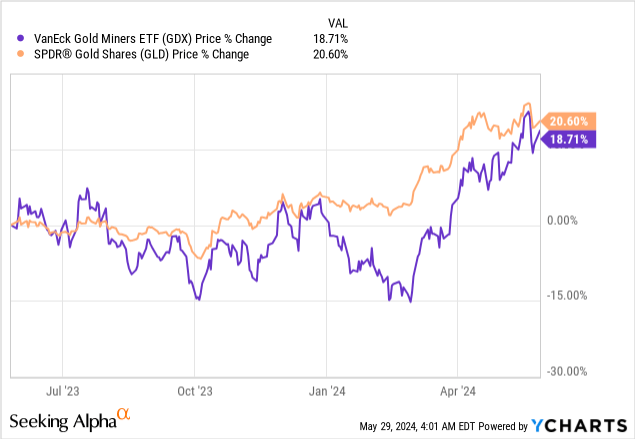

Unfortunately, the VanEck Gold Miners ETF (NYSEARCA:GDX) has been lagging the SPDR® Gold Shares ETF (NYSEARCA:GLD), which is up by more than 20% over the past 12-month period.

The GDX still outperformed the broader equity market, with the ETF delivering a total return exceeding 27% since I first covered it with a buy rating in September of last year.

Seeking Alpha

The difference between the GDX and the S&P 500 is even larger since my latest article on the ETF from February of this year, when I warned that poor performance recently should not distract investors. Since then, the GDX is up by more than 36%, while the S&P 500 appreciated by merely 4%.

Even though GDX investors fared better than the broader equity market recently, it still wasn’t enough to justify the higher risk associated with investing in gold mining stocks as opposed to direct exposure to gold.

But before we jump to conclusions, we should first take a closer look at what caused the GDX to underperform the GLD and evaluate the probability of this trend reversing going forward.

Rising Costs

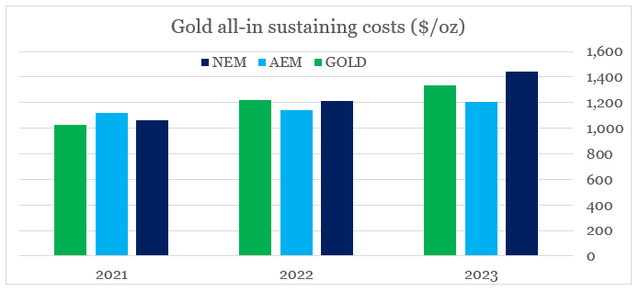

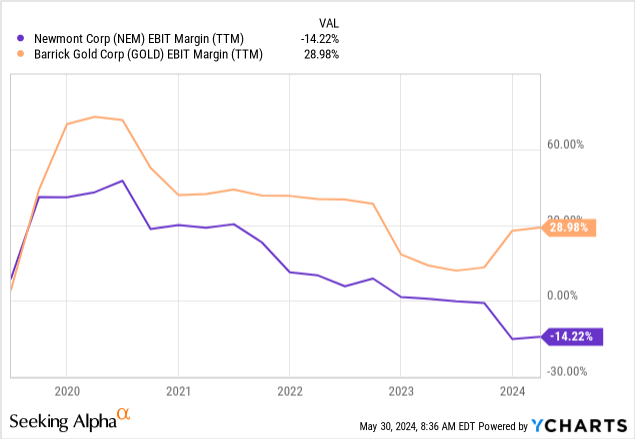

The most obvious reason why the GDX’s upside has been fairly limited over the past year or so are the rising costs. The top 3 holdings of the GDX – Newmont Corporation (NEM), Agnico Eagle Mines (AEM) and Barrick Gold (GOLD) have all experienced a notable increase in their all-in sustaining costs per ounce from an average of $1,070 in 2021 to $1,330 as of the end of fiscal year 2023.

prepared by the author, using data from annual reports

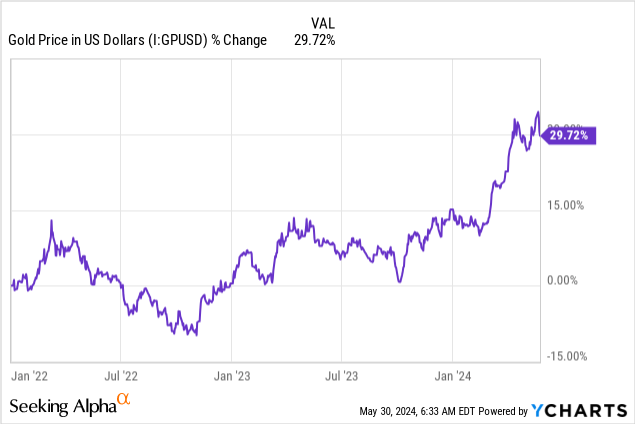

This increase in the average AISC for the three largest gold miners is roughly 24%, which is much higher than the equivalent increase in the price of gold (XAUUSD:CUR) for the same period. As we see from the graph below, from the 31st of December 2021 through the 1st of January 2024 the spot price of gold has increased roughly 15%. The very recent rally in gold has taken this increase to nearly 30% in the months of March and April of this year.

That is why, the 3 major gold miners have not managed to increase their margins recently and the upside of their share prices has been fairly limited.

prepared by the author, using data from Seeking Alpha

What’s In Store For 2024

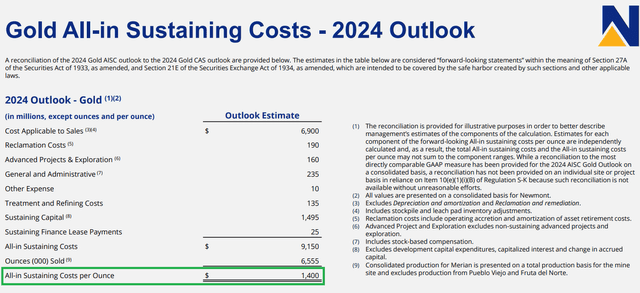

Looking ahead, however, should the price of oil & natural gas remain at their current levels, 2024 is gearing to be a strong year for gold miners as AISC is expected to be kept under control. Newmont’s management, for example, expects AISC to be at around $1,400 in FY 2024, compared to $1,444 in the previous year.

Newmont Annual Report

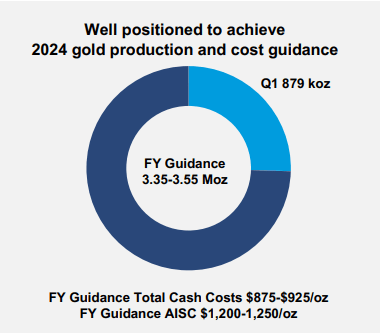

At Agnico Eagle Mines, as of the end of the first quarter of 2024 the management has guided for ASIC to be within the range of $1,200 to $1,250 for the full year.

Agnico Eagle Mines Q1 2024 Investor Presentation

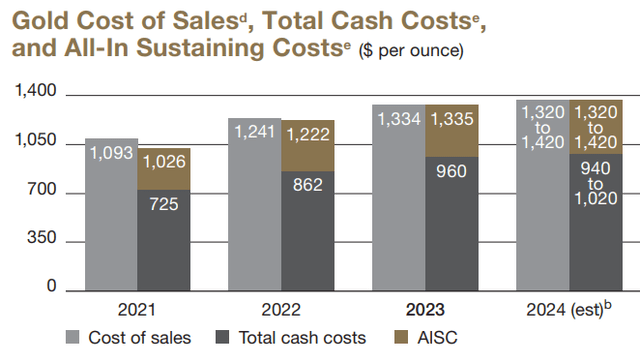

The mid-range of Barrick Gold’s guidance is also not materially different from the company’s reported AISC for 2023.

Barrick Gold Annual Report

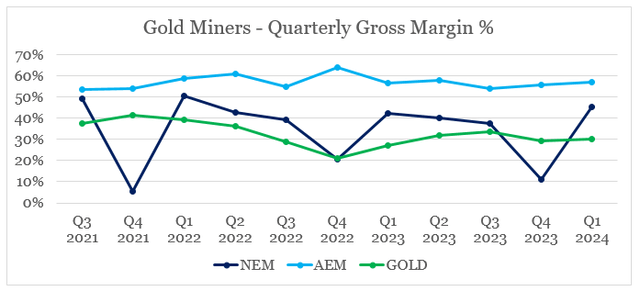

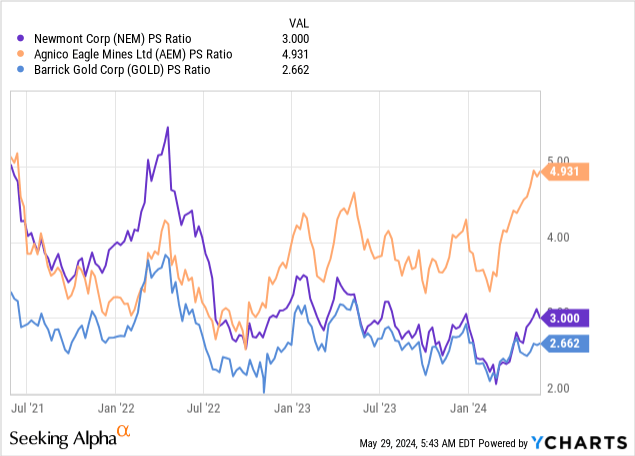

Thus, margins are likely to improve in the coming months and valuation multiples should follow suit. Except for AEM, which trades at a significantly higher sales multiple and close to fair value, the other two gold miners currently trade at significantly lower multiples to their 2021–22 highs.

Based on these lower multiples, it appears that the market is not pricing-in any meaningful margin improvement for NEM and GOLD, which could be a major tailwind for the GDX through the rest of 2024.

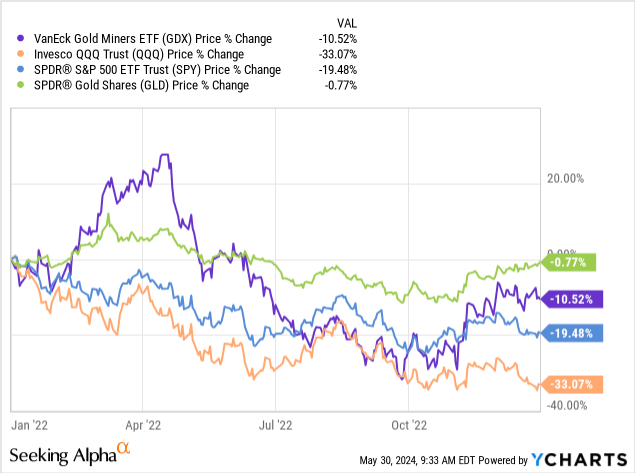

Lastly, there is the issue associated with the overall risk for equities. As opposed to having direct exposure to gold, the GDX is subject to stronger downward movements during periods of market sell-offs and with the broader equity market trading at near record-high levels, there is a higher risk for the GDX relatively to the GLD going forward. However, during the last market sell-off in 2022, the GDX fared far better than the S&P 500 and especially against the technology sector (see below).

Conclusion

Despite its disappointing performance relative to the price of gold, the GDX remains attractive for anyone who is not willing to take high idiosyncratic risk by picking individual gold miners. Through the rest of 2024 we are likely to see the GDX outperforming the GLD, provided that equities do not experience a major sell-off.

Read the full article here