Investment Thesis

Genpact Limited (NYSE:G) recently revealed an average headcount increase of 9.7% in the last quarter, new investments in sales and marketing to support growth, and operations in the growing global artificial intelligence market. For these reasons, and the current amount of cash in hand, I expect an acceleration in unlevered FCF from 2025 to 2029. I also think that the ongoing stock repurchases at current price levels, EPS growth expectations, and recent dividend increases could bring demand for the stock.

Price Target: My price target is $66-$67 per share, which was obtained using a DCF model. However, previous M&A transactions implied a valuation of more than $129 per share. In any case, I think that the company is quite undervalued at the current price mark.

Business Overview: Geographic Diversification

Genpact Limited is a global professional services firm offering digital-led innovation and digitally-enabled intelligent operations to Fortune Global 500 clients.

Company’s Website

With over 131,000 employees in more than 35 countries, Genpact appears to have, in my view, a diversified business profile, which will most likely make future net sales growth less volatile than other peers with less geographic diversification.

The company reports three business segments: Financial Services, Consumer and Healthcare, and High Tech and Manufacturing. So, there is also diversification in the type of clients served.

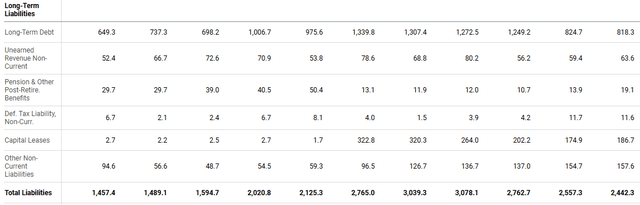

A Lot Of Cash In Hand, And Limited Debt

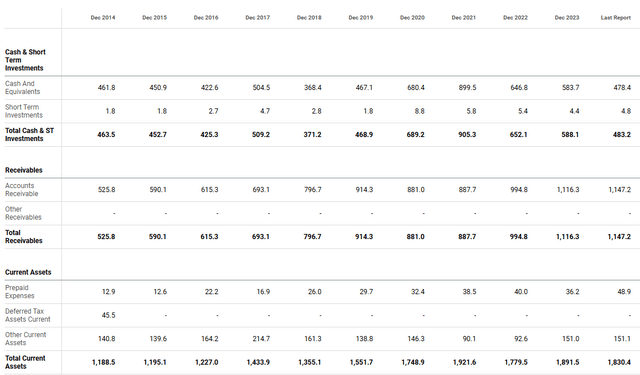

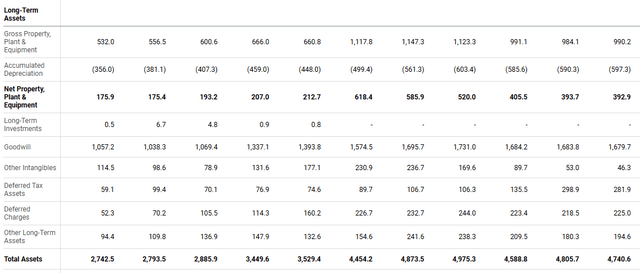

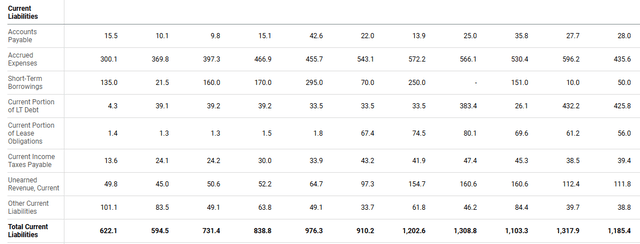

Genpact Limited receives money from clients and pays its employees using these dollars. Hence, the balance sheet reports a significant amount of cash and accounts receivable, which mainly comprised the largest part of the total amount of assets.

Seeking Alpha Seeking Alpha

The company does not really need a lot of debt financing because clients finance the ongoing operations. The asset/liability ratio is larger than 1x, and the net leverage appears limited. Overall, in my opinion, the balance sheet appears quite stable. The company appears to have sufficient financing to hire more employees and finance marketing campaigns to sustain future growth.

Seeking Alpha Seeking Alpha

EPS Growth And Net Sales Growth Are Expected In 2025 And 2026

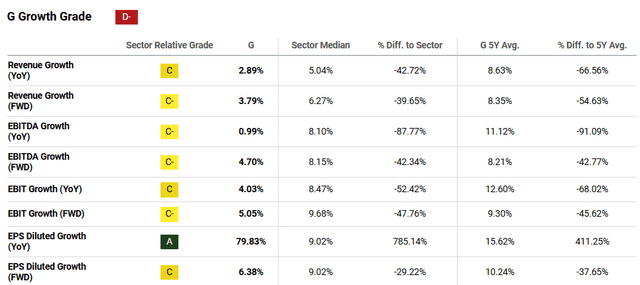

In the last quarter, the company reported an actual EPS GAAP of $0.64 and sales of $1.13 billion. Both figures were better than expected. Analysts are also expecting net sales growth in 2024, 2025, and 2026. According to information from Seeking Alpha, EPS growth could stand at 8% in 2025 and 11% in 2026.

Seeking Alpha

The company is currently trading at 10x forward 2024 earnings, which I think is cheap for a company that could grow at 11% YoY in 2026. Net sales growth is expected to be 3% in 2024, 5.8% in 2025, and 8% in 2026. I think that the current valuation could increase as soon as expected net sales growth and EPS growth are delivered.

Seeking Alpha

My DCF Model With Very Conservative Assumptions: $66-$67 Per Share

The company reports a significant amount of revenue from target markets that are growing at a large pace. The global artificial intelligence market is expected to grow at a CAGR of 36.6% from 2024 to 2030. Besides, the global artificial intelligence consulting market could grow at a CAGR of 26.49% from now to 2031.

In my view, with these target markets growing at this pace, the company’s net sales will most likely accelerate in the coming years. I used lower net sales growth in my DCF model than in the market because I tried to be as conservative as possible. The recent net sales growth reported by the company was not that large.

Seeking Alpha

The company’s average headcount increased by 9.7% in Q1 2024. The company receives revenue from services given by the employees to other organizations. Hence, in this case, I think that headcount growth is linked to financial performance and revenue. We can expect revenue growth in coming years because headcount growth continues to trend higher.

Our average headcount increased by 9.7% to approximately 130,500 in the first quarter of 2024 from approximately 119,000 in the first quarter of 2023. Source: 10-Q

Seeking Alpha

I think that the company may receive net sales growth thanks to the Financial Services segment, which is seeing a large deal ramp-ups and demand growth for financial crimes services.

The global financial crime and fraud management solutions market was valued at around USD 1.30 billion in 2023. The industry is further expected to grow at a CAGR of nearly 5.7% between 2024 and 2032. Source: Expert Market Research

In the last quarter, the company also saw a significant increase in supply chain engagements, mainly in the Consumer and Healthcare segment, which saw an increase of 4.6% in its quarterly revenue. In my DCF model, I assumed that these services will most likely continue to drive net sales growth up.

SG&A expenses recently increased because management invested a significant amount of dollars in the sales and marketing teams to support growth. In my view, these initiatives could bring net sales growth from 2024 and 2025.

SG&A expenses as a percentage of total net revenues increased from 19.9% in the first quarter of 2023 to 20.8% in the first quarter of 2024. SG&A expenses were $235.0 million in the first quarter of 2024, up $18.5 million, or 8.6%, from $216.5 million in the first quarter of 2023. The increase in SG&A expenses was primarily due to increased investments in our sales and marketing teams to support growth. Source: 10-Q

I think that the ongoing stock repurchases authorized in 2015 will most likely bring stock demand, and may lower the cost of equity. According to the last quarterly report, the company repurchased 59,043,000 of its common shares at an average price of $31.85 per share since 2015. Recently, the company also bought shares at $34.67 per share. In my view, the fact that the company is buying shares at the current valuation indicates that management is aware of the company’s current undervaluation.

During the three months ended March 31, 2023, and 2024, we repurchased 630,605 and 864,925 of our common shares, respectively, on the open market at a weighted average price of $47.57 and $34.67 per share for an aggregate cash amount of $30.0 million and $30.0 million, respectively. Source: 10-Q

Recent dividend increases could also accelerate the demand for the stock and lower the cost of capital. In 2023, dividend increased by 10% to $0.125 per common share. In 2024, dividend also increased by 11% to $0.1375 per common share.

On February 8, 2024, our board of directors approved an 11% increase in our quarterly cash dividend from $0.1375 per common share to $0.1525 per common share. Source: 10-Q

On February 9, 2023, our Board of directors approved a 10% increase in our quarterly cash dividend from $0.125 per common share to $0.1375 per common share. Source: 10-Q

For the assessment of future unlevered FCF, I took into account revenue growth close to 3% and 5%, EBITDA growth between 5% and 8%, and FCF growth close to 5% from 2025 to 2029.

The company reported growing unlevered FCF from 2014 to 2023 with some declines in FCF growth, however, FCF was always positive. I do not see why unlevered FCF growth would decline in the coming years.

Seeking Alpha

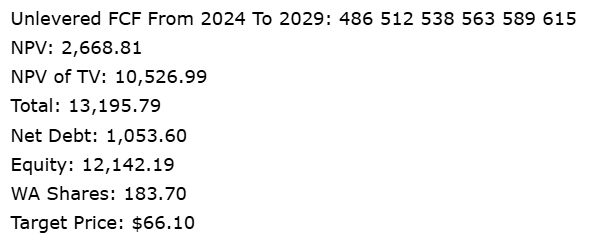

My expectations include 2025 FCF of $512 million, 2027 FCF of $563 million, and 2029 FCF of $615 million. I also used a conservative long-term growth of 2% and WACC of 6.2%, which is not far from the interest rate signed for the 6.000% senior notes due 2029. The total implied enterprise value would stand at about $10 billion, and my price target would be $66 per share.

Author’s Work

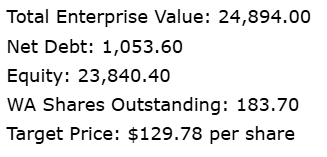

Review Of Previous Transactions: $129 Per Share

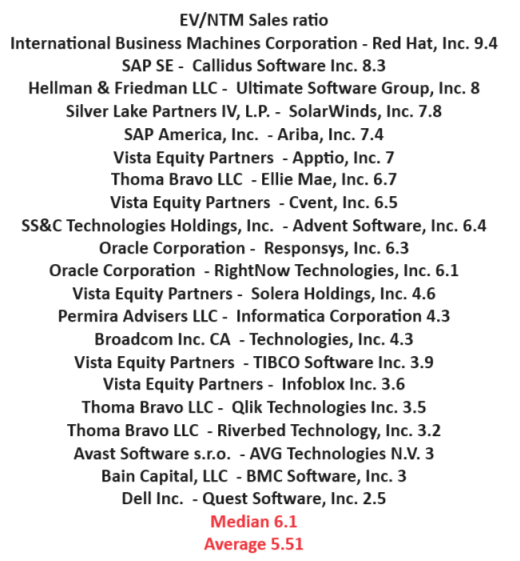

I reviewed some of the previous transactions of companies in the tech industry. Companies out there were bought for close to 9x, like Red Hat, Inc. Callidus Software Inc. was bought for 8.3x, Cvent was acquired for 6.5x, and Informatica Corporation was bought for 4.3x. The list of transactions that I consulted included a median EV/NTM Sales ratio of 5.51x.

Author’s Compilations

If we assume a net revenue of $4,518.8 million, Genpact would have an implied enterprise value of $24,894 million or 5.51x $4,518.8 million. The implied total valuation would be $129 per share.

Author’s Work

Comparable companies include Infosys Limited (INFY), Accenture plc (ACN), Wipro Limited (WIT), Cognizant Technology Solutions (CTSH), and Atos (OTCPK:AEXAF). Most of them trade at richer valuations than that of Genpact. I do not think these companies would buy Genpact because the company is not small. However, investors currently buying shares of these competitors may soon buy shares of Genpact. As a consequence, we may soon see the stock price trend higher again.

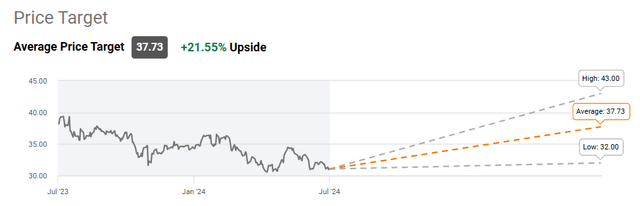

Equity Research Review Also Indicates Certain Upside Potential

I reviewed the work of other analysts. According to S&P, There are close to 12 analysts covering the stock. The average target price is $37 per share. I think that the upside potential is significantly larger than the price proposed by most analysts out there. In my view, they believe that the slow growth seen in 2024 may continue in 2025 and 2026.

Seeking Alpha

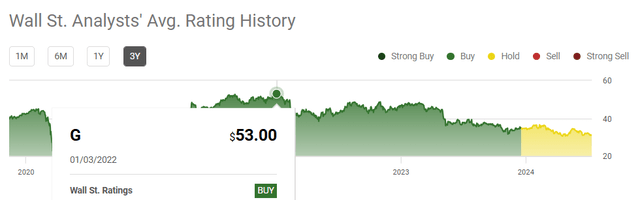

Given the target market growth, in my view, Genpact will most likely see again the FCF growth that we could observe in the last 10 years. In this regard, I would remind market participants that in 2022, the average price target was close to $53. It is not far from the price target obtained from my DCF analysis.

Seeking Alpha

Risks

In my view, changes in the labour conditions and overall increase in salaries could be very detrimental for Genpact Limited. Shareholders may suffer a decrease in the profit margins and a decrease in net income. If a sufficient number of analysts detect the decrease in profitability, I would be expecting a decrease in EPS expectations and FCF growth. Consequently, the stock price could fall.

The company operates in the innovative AI technology market, in which many peers may offer better products or more innovative products than Genpact Limited. The company may also have issues in selling products, even though they may be innovative. Besides, future revenue growth from the AI market could be lower than expected. If analysts lower their expectations with regard to this market, I would be expecting a decline in the stock price.

The market for AI technology and services is highly competitive and rapidly evolving. We face significant competition from our traditional competitors as well as other third parties, including those that are new to the market or our industry, and our clients may develop their own AI-related capabilities. We may also be unable to bring AI-enabled products and solutions to market as effectively, or with the same speed or in the same volumes, as our competitors, which may harm our competitive position. Source: 10-K

The company reports a large amount of assets, employees, and personnel located in India. Changes in the regulatory environment in India or changes in the economic environment in this country could push the company’s net income growth down. Management discussed extensively about this risk factor in the annual report.

Various factors, such as changes in the central or state Indian governments, could trigger changes in India’s economic liberalization and deregulation policies and disrupt business and economic conditions in India generally and our business in particular. Source: 10-K

Conclusion

Genpact Limited recently reported that the company’s average headcount increased by 9.7% in the last quarter. Besides, the company’s operations are linked to the global artificial intelligence market, which is expected to grow at a CAGR of 36.6% from 2024 to 2030. Genpact reported a significant amount of dollars invested in the sales and marketing teams to support growth. For all these reasons, I would be expecting unlevered FCF growth from 2024 to 2029.

My DCF model indicated that the company could be worth around $66 per share. However, a review of previous transactions in the industry implied a total valuation of $129 per share, and most analysts believe that the stock is undervalued. In my view, recent dividend increases and the ongoing acquisition of shares could accelerate the demand for the stock and enhance the total valuation.

Read the full article here