Investment thesis

GitLab (NASDAQ:GTLB) went public in late 2021 and since then the stock price has declined more than 70%. Some people might be tempted to buy the dip, but I would like to make readers aware that the upside potential is insignificant compared to the level of risks and uncertainties. Moreover, the current harsh environment does not favor stocks with no profits, even if they demonstrate immense topline growth. I would not buy GTLB stock at current levels, but the company will be on my radar in the next several quarters to watch how the situation unfolds.

Company information

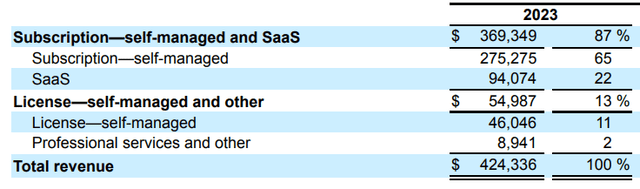

GitLab is a technology company offering the market its complete DevOps platform delivered as a single application. GitLab empowers teams and organizations to streamline their software development lifecycle, enhance collaboration, and accelerate software delivery. According to the latest 10-K report, the company has over 30 million registered users and over 50% of the Fortune 100 companies are GitLab customers. GitLab mainly generates revenues from selling subscriptions on both self-managed and SaaS models.

The company’s fiscal year ends on January 31. Self-managed subscriptions comprised almost two-thirds of the company’s total sales in FY 2023.

GitLab’s latest 10-K report

Financials

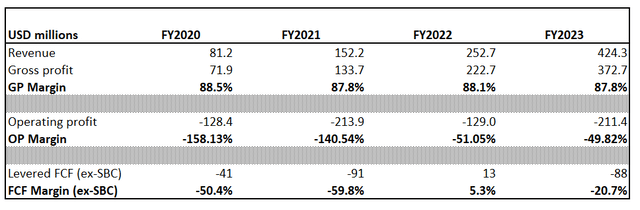

GTLB went public relatively recently, so the historical financial performance horizon is rather short, with only four full fiscal years available. The company delivered a staggering above 50% revenue CAGR, though comps were low and easy to beat. The gross margin looks immense, being close to 90%. The operating margin looks far from breaking even, but it improved significantly over the last four years.

Author’s calculations

For me, as a potential investor, the massive operating loss is a red flag, so I need to go into detail here. As you can see in the below table, SG&A expenses are huge and are higher than revenue.

Author’s calculations

I do not like that R&D expenses are much lower than SG&A. Marketing is essential for a young company like GitLab to create word of mouth, but underinvestment in product development might be costly in the long term.

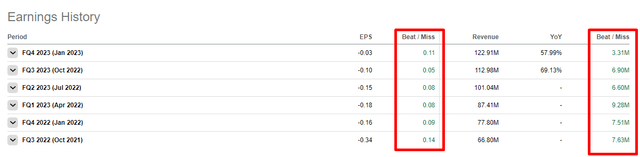

Narrowing down to the latest quarterly earnings, the company demonstrated a beat in revenue and EPS against consensus estimates. The company has never failed to beat consensus estimates since it went public, though the sample is relatively small to make a confident opinion regarding future quarters.

Seeking Alpha

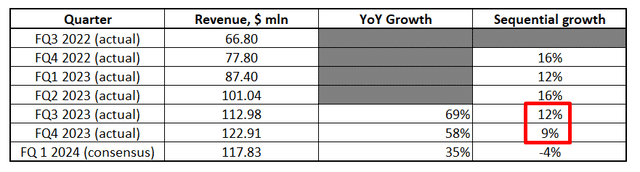

If we look at the revenue dynamics sequentially, we can see that topline growth is decelerating, and there is almost no data to compare YoY dynamics. In its latest 10-K report, the company claims that fiscal quarters 3 and 4 are usually more potent than the first two. Still, we can see that sequential growth decelerated notably in the last two quarters. YoY growth is also expected to decelerate significantly in Q1 FY2024. The earnings release is relatively close and is planned on June 6.

Author’s calculations

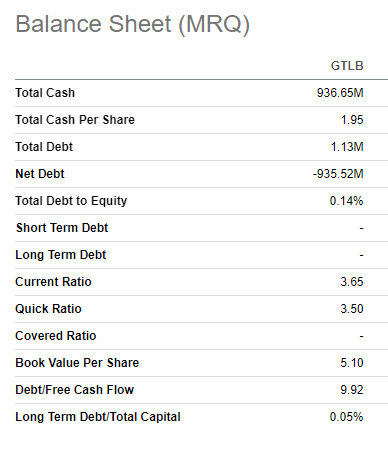

The company’s balance sheet looks strong with almost no debt and outstanding cash at about $1 billion is significantly higher than the last quarter’s cash burn rate of approximately $77 million. Current liquidity also is in good shape, so I believe GitLab is not likely to face the need to raise additional finance in the nearest future, which is a good sign given the current tight credit environment.

Seeking Alpha

Valuation

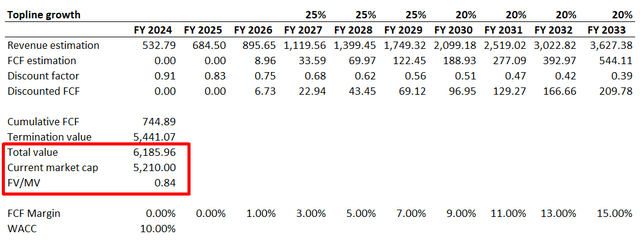

Gitlab is an aggressively growing company, so I use the discounted cash flow [DCF] approach for valuation. I use 10% WACC which is a round-up of GuruFocus’ estimate. I have revenue consensus estimates available for the nearest three fiscal years. For years beyond I project 25% revenue growth for the next three years after FY2027 and then expect it to decelerate to 20%. I expect the company to generate positive FCF in FY 2026 and assume the FCF margin will expand by two percentage points yearly.

Author’s calculations

As we can see, incorporating all assumptions into the DCF model gives us a fair value of the business at about $6.2 billion. It indicates an upside potential between 20% to 15%. If GTLB was a value stock with sustainable dividends and reliably estimated future cash flows, I would have invested immediately given the upside potential. But due to very high uncertainty about underlying assumptions, I consider the upside potential as not attractive.

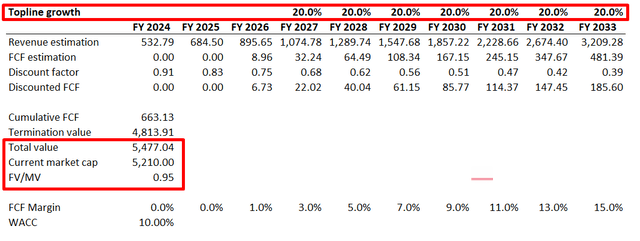

Moreover, let me also simulate less aggressive but still very optimistic revenue CAGR of 20%. Implementing a more modest revenue CAGR for years beyond FY 2027 gives only a 5% upside potential, which is definitely not sufficient for a growth stock with a high uncertainty level.

Author’s calculations

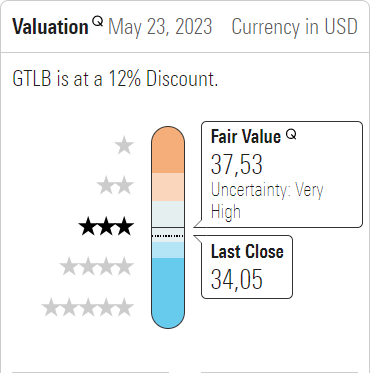

Overall, I do not consider the current stock price attractive. Moreover, Morningstar Premium estimates GTLB’s share price fair value at about $37.5, just about 10% higher than the actual share price. The uncertainty level is also very high, according to Morningstar.

Morningstar Premium

Risks to consider

The main risk that I see in the nearest term is the overall market volatility which an unfavorable macro environment can cause. Apart from the AI frenzy fueling the market this year, there are no other positive catalysts for the market. On the other hand, the war in Ukraine is still far from its end, there is uncertainty regarding when the Fed will stop its rate hike cycle, and Democrats and Republicans still cannot reach an agreement over the debt ceiling. All these seem vastly unfavorable for the stock market, and growth stocks suffer the most in overall market turmoil. S&P500 is about 10% lower than all-time highs and I believe the current harsh macro environment is not priced in.

The company’s high SG&A costs are also a big risk. During the latest full-year results, SG&A expenses were still higher than sales. It means that the company has been fueling its aggressive topline growth with aggressive marketing. Thus, there is high uncertainty about the ability to sustain aggressive revenue growth in case the management decides to optimize selling expenses. Also, I consider the company’s SG&A and R&D expenses mix, indicating that management might concentrate on short-term revenue growth more than long-term growth. It is not good for the long term and risks the company’s ability to keep up with technological advancements.

Last, GTLB heavily relies on open-source solutions, which can have benefits and risks. The most apparent risks for open-source are security vulnerabilities, licensing issues, and potential conflicts within the open-source community. This is also a risk that the management has to be able to manage to mitigate it.

Bottom line

Overall, I believe the upside potential for GTLB stock derived from my valuation analysis is not worth investing in at current levels. The uncertainty regarding future growth and the break-even timing is vague. The company is still far from becoming profitable, and all growth companies with no profits are highly vulnerable to adverse conditions in the macro environment. Since 2023 and the few subsequent years are expected to be challenging for the global economy, I also do not see how GTLB stock will grow under current circumstances. The stock is a hold at current levels, in my opinion.

Read the full article here