Introduction

The regional banks industry has not had a very easy time this year so far as the industry was shocked when two of the leading companies went under. There was a ripple effect that went through the broader financials sector and many companies have not managed to recover, Glacier Bancorp (NYSE:GBCI) being one of them.

The wipeout in valuation left a lot of great opportunities and companies at decreased values and strong yields for investors. In the case of GBCI though I think that it still doesn’t offer a good buying incentive, even after dropping over 40% in price the last 12 months alone. The rise in interest rates doesn’t seem to have positioned the company any better in growing its earnings and the market has punished the company for this. It would be said though that GBCI has a decent dividend yield right now at around 4.6% which I think is worth taking part in at least, so a hold rating will be my decision for GBCI.

Company Structure

In its latest quarterly report, Glacier Bancorp emerged as the parent company overseeing a diverse portfolio of subsidiaries, collectively boasting a robust presence across 222 locations spanning a wide geographical expanse. This impressive network extends its reach to encompass the states of Montana, Idaho, Utah, Washington, Wyoming, Colorado, Arizona, and Nevada. Operating through a dynamic set of 17 distinct bank divisions, in addition to its corporate arm, the company prides itself on delivering a comprehensive spectrum of financial services to its valued customers.

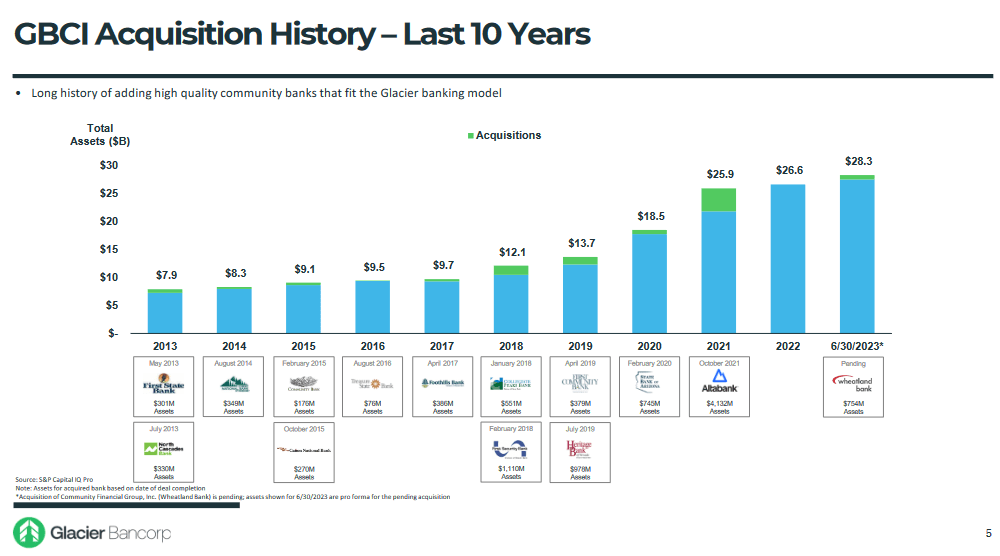

Acquisitions (Investor Presentation)

A driving force behind the expansion of GBCI has been acquisitions over the years which have been plenty. The company most recently acquired Community Financial Group in Spokane Washington and I think this will further add some earnings potential for the business.

Earnings Transcript

Going off the last earnings call from GBCI the CEO Randy Chesler had some good insight on the recent performance and how the company aims to better itself.

-

“We remain very optimistic about the long-term position of the company, despite the lingering headwinds impacting the banking industry today. The eight Western States in which we have a presence are among the strongest economies in the U.S. We have ample liquidity, a high quality loan portfolio, a proven banking model, and M&A expertise that is well positioned to take advantage of the market when conditions are right”.

I think that the market position and location that GBCI is in is a key driver for the long-term prospects of the company. Even if they lack some margin expansion, they should be able to see deposits grow from the simple fact the economics they are in is some of the largest ones in the US right now.

-

“Interest income of $247 million in the current quarter increased $15.5 million or 7%, over the prior quarter interest income of $232 million. Interest income in the current quarter increased $47.7 million or 27% — 24% over the prior year second quarter. Net income was $55 million for the current quarter, I’m sorry, net income was $55 million for the current quarter, a decrease of $6.2 million or 10%, from the prior quarter net income of $61.2 million”.

Seeing GBCI finally able to capitalize on the growing interest rates has been a very nice touch I think. Many regional banks are already far ahead and have grown their bottom lines way faster. The net income may have dropped but the interest income increase is helping offset some of that at least. With GBCI further increasing market share by purchasing Community Financial Group I think will further add some fuel to the EPS expansion.

Valuation & Comparison

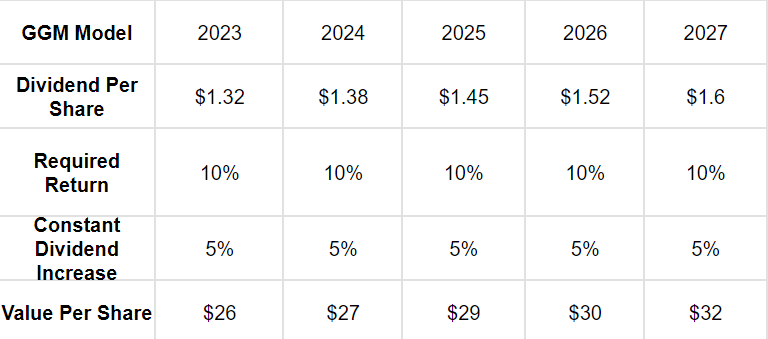

GGM Model (Author)

Looking at the GGM model above here for GBCI I think it further highlights some of the lacking incentives that are present with the share price right now for a buy case. The target price I have comes out at $26 which is around 10% below the current one. This estimate is also accounting for a market-beating return of at least 10% and a terminal increase to the dividend of 5%. Now, historically over the last 5 years, GBCI has raised the dividend by over 20% annually instead. I think it’s likely we don’t see a similar increase over the long term as the payout ratio is already quite high at 52%. To conclude though, I think that GBCI does offer some value, but at the right price, as it is not there yet. Around $26 I would start to be more interested instead. But for now, it remains a hold I think.

Risk Associated

At the outset of the previous year, Glacier found itself in a less-than-ideal financial position as it grappled with the challenges posed by an increasing interest rate environment. Notably, the company’s balance sheet bore the weight of a substantial available-for-sale (“AFS”) securities portfolio as of December 2021, accounting for a significant 38% of its total earning assets. Unfortunately, this strategic asset allocation came with consequences as the company incurred substantial unrealized mark-to-market losses due to the upward trajectory of interest rates.

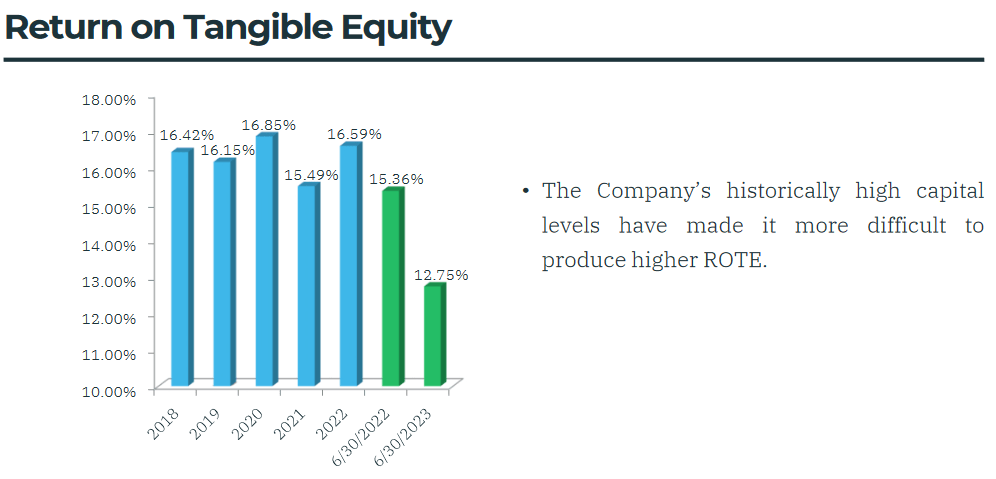

ROTE (Investor Presentation)

The lack of cheap capital seems to have been hurting the ROTE for the business which has been decreasing heavily on just a quarterly basis. The lack of activity for GBCI has been a big culprit for this I think. Going forward, I wouldn’t expect a swift recovery and tailwinds such as decreasing interest rates seem necessary as well before GBCI will be heading higher.

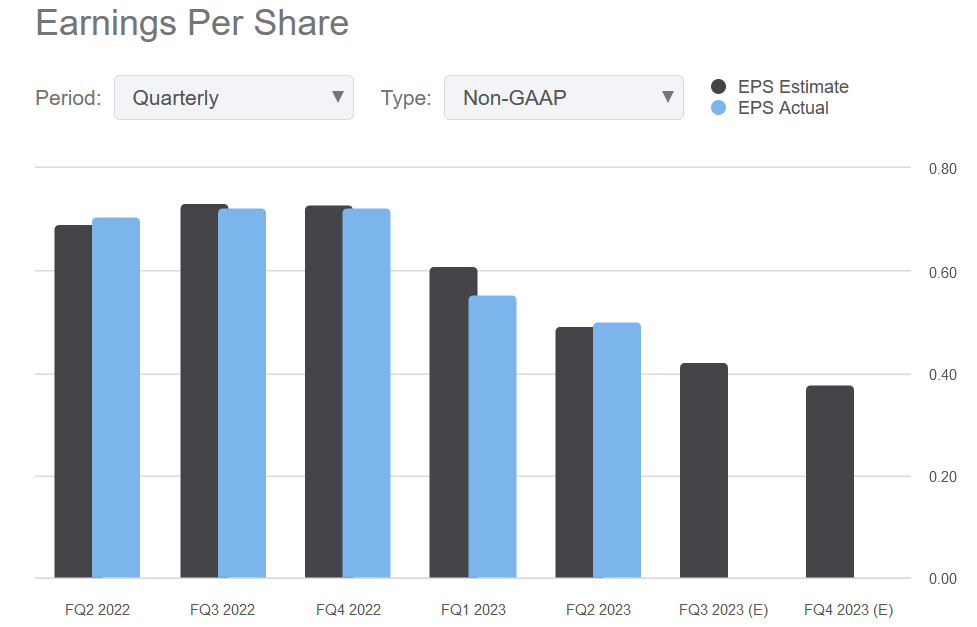

EPS Results (Seeking Alpha)

The expectations are that GBCI will continue to post worse and worse EPS results with no reversal in sight and I tend to agree with this. My view on the interest rates is that they will remain largely the same for the better half of 2024, before possibly going down after the summer. The Fed has been quite hawkish in their statements and I think they will continue to be so. A quick switch around in their stance, I see it as highly unlikely.

Investor Takeaway

The regional bank industry has been in turmoil this year and a lot of companies have seen their valuation heavily decrease. The share price for GBCI has decreased by over 40% and I don’t think we are going to see a swift recovery unfortunately. For the moment though, GBCI does have a solid dividend yield of 4.6% which I think is sustainable. This adds some shareholder value and makes holding on to a position in the business reasonable. This led to me issuing a hold rating for GBCI stock.

Read the full article here