Gladstone Capital (NASDAQ:GLAD) is a well-managed business development company that provides loans to lower middle market businesses and has an operating history dating back to 2001.

The BDC has seen solid portfolio growth in the last year due to new investments and has NII upside in a rising-rate environment due to its exposure to floating-rate loans. Since the latest ADP payroll report crushed expectations, the odds are in favor of more interest rate hikes in 2023.

Gladstone Capital covers its dividend with net investment income and has NII upside, which is why I have started a position in this 9.6% yielding BDC in my passive income portfolio.

Gladstone Capital Is A Growing And Well-Managed BDC

Gladstone Capital was founded back in 2001 and is therefore looking back on more than two decades of operating history. Since the BDC got its start in the industry, it has invested more than $2.5 billion in lower middle market companies across the United States.

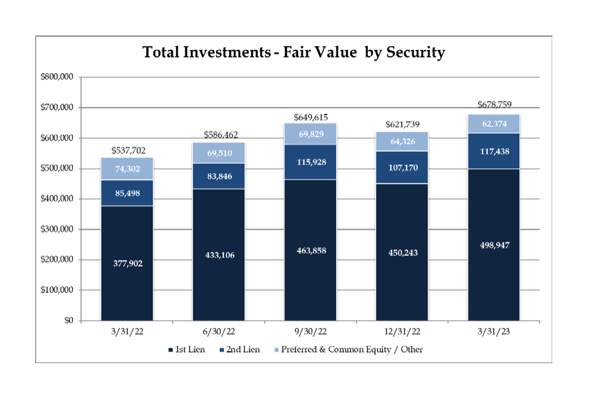

Like other BDCs, Gladstone Capital makes highly secured loans to lower middle market businesses in the United States which typically have an annual EBITDA of $3 million to $15 million. The BDC has a long-term uptrend in the size of its portfolio and just in the last year, Gladstone Capital grew its portfolio to $678.8 million, up 26% YoY, primarily due to new loan originations.

Gladstone Capital concentrates its investments in First and Second Liens which are the safest forms of debt that a BDC can invest in. Approximately 74% of all investments as of the end of March were invested in First Liens, while an additional 17% were invested in Second Liens, bringing the total of secured investments to more than 90%.

Total Investments – Fair Value By Security (Gladstone Capital Corp)

The key to Gladstone Capital’s growth is a strong origination platform and a steady deal flow. The BDC grew its portfolio value by 150 million in the last four quarters which I think is a respectable achievement considering that high interest rates have overall weight on industry origination activity.

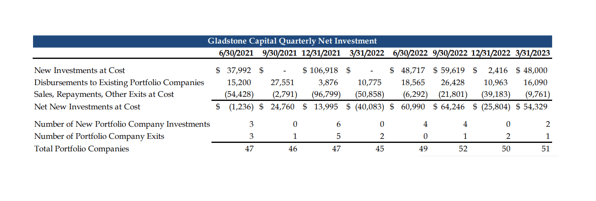

Total net new investments summed up to $153.8 million with net new investments exceeding investment exits and repayments in three out of the last four quarters.

New Net Investments (Gladstone Capital Corp)

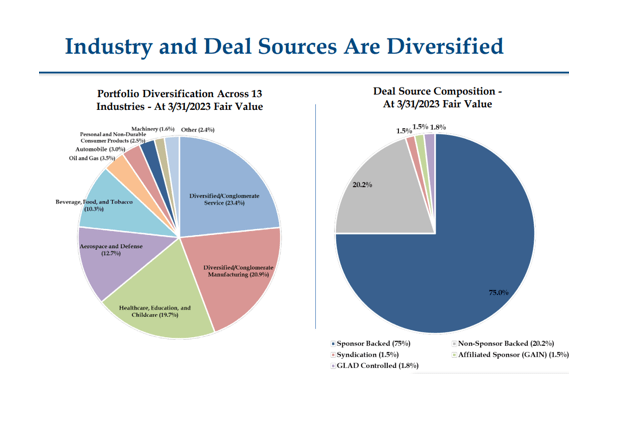

The portfolio is also well-diversified and primarily includes investments in recession-resistant industries that don’t see large changes in sales and cash flows during times of uncertainty and slowing economic growth.

The biggest three industries in Gladstone Capital’s investment portfolio are Diversified, Conglomerates and Healthcare/Education/Childcare, accounting for more than half (64%) of the BDC’s total investments.

Portfolio Diversification (Gladstone Capital Corp)

Gladstone Capital And Floating-Rate Exposure, ADP Report Indicating Rate Hike Potential

The kicker for NII growth relates to Gladstone Capital’s investment portfolio which is positioned towards floating-rate loans. At the end of the first quarter, a total of 91.5% of all investment loans contained floating-rate deal terms.

Most BDCs with floating-rate exposure are set to profit from the central bank’s rate hiking cycle, so while I wouldn’t consider this to be a competitive advantage for GLAD, it is a NII catalyst nonetheless.

Today’s much better-than-expected ADP report strongly implies that the central bank will continue to hike interest rates in the second half of the year, thereby giving GLAD an upside catalyst for NII growth. ADP’s payroll report today showed that the U.S. economy created 497K new private jobs, crushing the estimate of 220K new jobs.

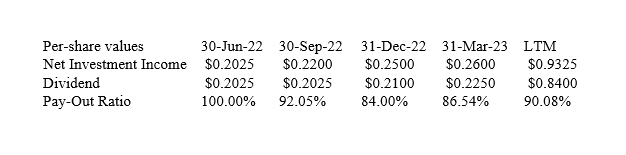

Gladstone Capital already raised its dividend two times in the last four quarters and the company has both an NII catalyst (interest rate hikes) as well as a moderate (LTM) pay-out ratio of 90% that leaves room for dividend growth. I think that management will continue to raise its monthly dividend as long as the BDC can defend its high level of credit quality.

At the end of the last quarter, only 0.5% of the BDC’s debt investments were classified as non-performing, reflecting an increase from 0.4% in the previous quarter.

Dividend (Author Created Table Using BDC Information)

BDCs are regulated as investment companies and must distribute over 90% of their profits to shareholders. Most BDCs I cover have pay-out ratios between 80-100% and I would rank GLAD in the middle.

This being said, I consider the 90% pay-out ratio as an indication that the company has room to grow its dividend, particularly if the central bank’s rate hiking cycle continues and improves Gladstone Capital’s pay-out metric.

Gladstone Capital Trades At A Deserved Premium To Net Asset Value

Valuations in the business development sector have rebounded in the second quarter and, in some cases, valuations have started to trade at premiums to net asset value again. The drivers of this upside price movement have been a strong jobs market as well as the growing potential for new rate hikes.

Gladstone Capital is well-managed, has good credit quality and a growing portfolio so I don’t see why GLAD couldn’t trade at a 15-20% premium to its net asset value. Based on a net asset value of $9.19 per share as of the end of the last quarter, this implies a fair value range of $10.57-11.03 per share.

The majority of BDCs that I cover trade at either small discounts or premiums to net asset value. Well-managed BDCs with strong growth histories like Hercules Capital Inc. (HTGC) or Main Street Capital Corporation (MAIN) trade at much higher premiums to NAV (34% or higher) because passive income investors have a high degree of confidence in their dividends.

What Would Cause Me To Reevaluate My Position On Gladstone Capital

Gladstone Capital has extensive experience in managing debt, reaching back to the early 2000s, meaning the company has relevant experience in evaluating credit investments and managing credit cycles.

The BDC’s credit quality looks good to me, but this may change moving forward if more borrowers default on the company’s predominantly floating-rate loans, something that I view as unlikely given the strength of the labor market. An uptick in the company’s non-performing loans and a change in the interest rate trajectory would cause me to reevaluate Gladstone Capital.

My Conclusion

I have added Gladstone Capital to my passive income portfolio, primarily for three reasons:

- The BDC has NII-upside related to its aggressive floating-rate positioning;

- The portfolio has grown at a healthy rate in the last year due to a strong origination business; and

- The BDC has raised its dividend twice last year, reflecting a shareholder-friendly attitude on the part of the BDC’s management.

Regarding the last point, NII upside (floating-rate exposure) and a moderate pay-out ratio strongly imply that management has room to grow its dividend moving forward.

Gladstone Capital is now trading at a premium to net asset value, like many BDCs now do again, but I think that the premium is justified when taking into account the BDC’s potential for NII growth in a rising-rate environment.

Read the full article here