I last covered the GraniteShares 2x Long COIN ETF (NASDAQ:CONL) for Seeking Alpha in April of this year. At that time, the crypto market was near the highs of 2024 as investment demand for Bitcoin (BTC-USD) spot ETFs in the US had taken BTC from $38k per coin in late-January to over $73k per coin by mid-March. The move in Coinbase (COIN) stock was even more impressive than that of BTC with COIN rallying more than 140% from early-February to late-March. However, since then most of these assets have gone nowhere. And the scenario that has played out for CONL is essentially exactly why I said investors should aim to avoid:

20 days of back and forth 5% trading sessions in COIN shows how quickly CONL can begin to decay. Even if the GraniteShares 2x COIN fund works as designed and doubles the returns of COIN, it only takes a few weeks before CONL starts underperforming due to market chop. So while the leverage can work very well in a sustained uptrend, the fund will decay over time from daily rebalancing without a strong uptrend.

Though not in a straight line, COIN’s stock price has declined since that April 19th article. In this CONL update, we’ll look at the ETF’s recent performance against COIN. We’ll also re-examine whether now could be the time to long COIN or CONL after the pullback from highs earlier this year.

The Proof Is In The Pudding

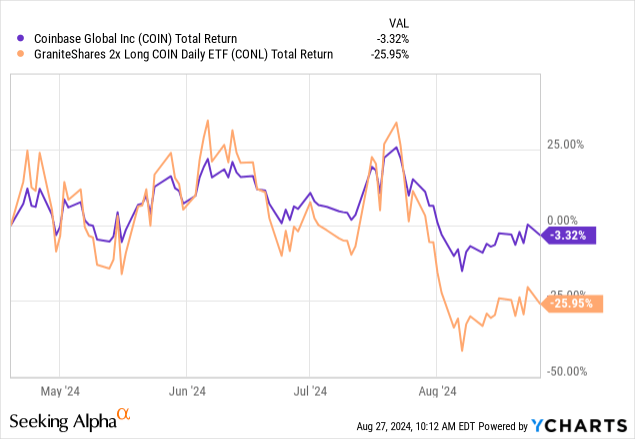

In the chart above, I’m showing total return for both CONL and COIN going back to April 19th when my previous article was published. It’s clear purely from judging the total return as of August 26th that CONL has performed quite badly. COIN is down a little over 3.3% since April 19th while CONL is down by just under 26%. This isn’t a 2x negative return, this is more than an 8x negative return over a four month period.

COIN vs CONL, 4/19/24 – 8/26/24 (Seeking Alpha)

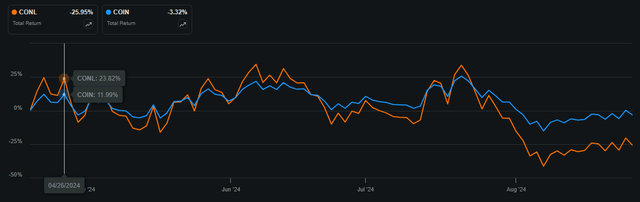

The other thing to consider is the fact that CONL outperformance to the upside is almost non-existent over this four month period. You can see in the screengrab above that CONL did indeed have close to a 2x return on April 26th when it had a 23.8% return versus 12% for COIN. It still isn’t exactly 2x, but it’s close enough to make shareholders happy in my personal opinion. But that’s as close to positive 2x territory the fund ever got to COIN over the last 4 months.

COIN vs CONL, 4/19/24 – 8/26/24 (Seeking Alpha)

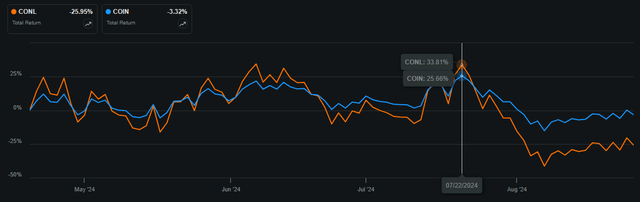

Even when CONL was briefly outperforming COIN in late-July, at 33.8% to 25.7% the total return for CONL was nowhere close to 2x that of COIN going back April 19th. I think this four month window of chop in COIN shows why CONL is a bad long term investment instrument. Something else that I think helps make the point crystal clear is the year to date performance comps:

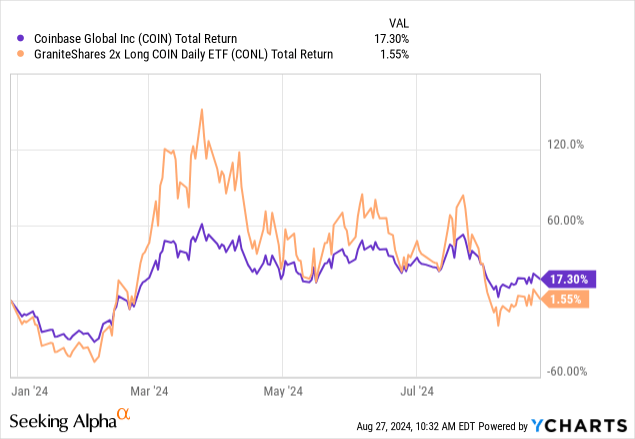

Since the beginning of 2024, COIN is up by over 17% while CONL is barely positive. Again, this is due to the daily rebalancing of the 2x leveraged shares. Now it’s important to point out that when COIN is in a sustained uptrend, CONL should actually work quite well as a short term trade – we can see that reflected above in the outperformance during March and April. The key is getting the timing on the trade right. So the question today is are we close enough to a bottom in COIN that it might justify a speculative long position in CONL?

Is Coinbase A Buy?

I’m going to keep this simple; I don’t think COIN is a buy today. I was actually asked about this specifically in my recent appearance on Seeking Alpha’s Investing Experts podcast. Here’s what I said in that mid-August recording:

MF: I would love Coinbase if it was priced a bit lower. I think that Coinbase is one of the more interesting stocks in the crypto space. I’ve been in and out as a trade. I don’t currently hold it. But I see this being almost, I don’t want to say a ‘too big to fail,’ because that’s not the right phrase. It’s a very important part of this ecosystem, especially domestically. So I expect that it will be going forward as well. But I would like it to be cheaper.

RS: How much cheaper?

MF: Last I looked, it was about 10 times sales. I don’t know, we can cut that in half and I’d be more interested.

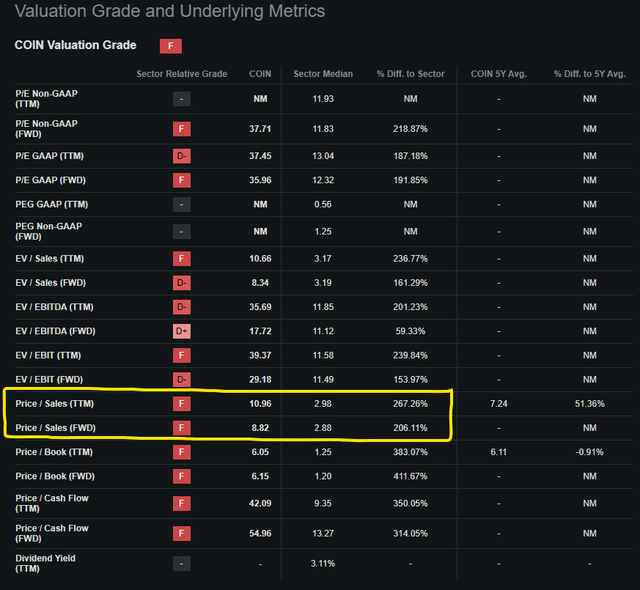

Turns out, COIN stock is actually closer to 11 times sales if we’re looking at the metric on a trailing twelve month basis:

COIN Valuation Grades (Seeking Alpha)

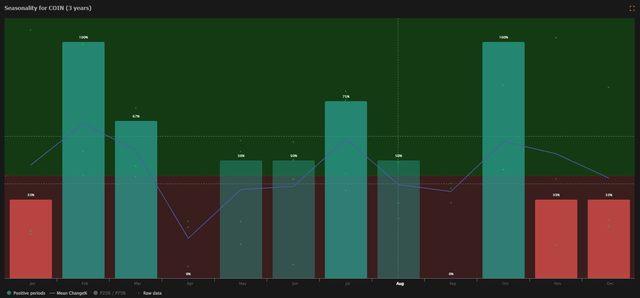

The forward multiple is a little less awful at 9x sales, but either way this is a very expense stock based purely on traditional valuation metrics compared to financial sector medians. Most individual metrics get the ‘F’ grade from Seeking Alpha and the aggregate valuation grade is clearly ‘F.’ But beyond the overvaluation, which can admittedly continue for far longer than what more value-oriented investors may expect, Coinbase is also up against bad seasonality as we prepare to enter September 2024:

COIN Seasonality (TrendSpider)

While it’s definitely a small sample size as the company only went public in 2021, COIN has never had a positive return during the month of September in three previous instances. Beyond that, the -7.1% mean change in the month makes September the second worst month of the year for COIN historically speaking. This could be, in part, due to September being a bad month for risk assets broadly over the last few years. Bitcoin has struggled in September recently, as has the S&P 500.

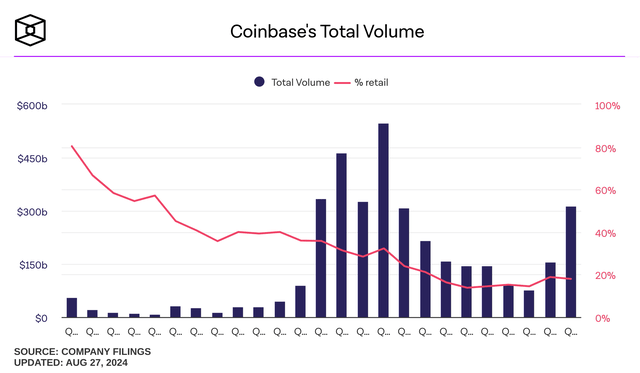

But specifically for Coinbase, weakness in digital assets likely isn’t good for growth in the company’s volume metrics:

COIN Volume vs Retail % (The Block)

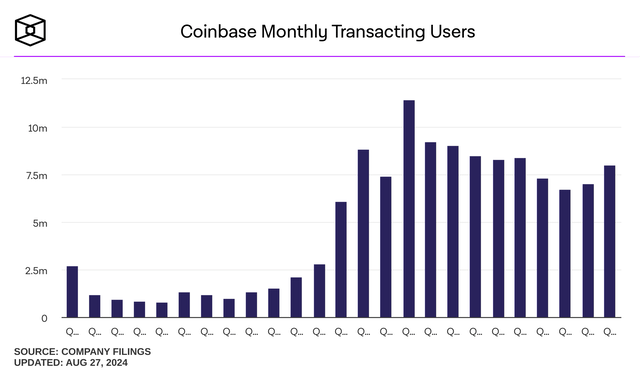

Coinbase did $312 billion in total volume during Q1-24. It was the largest amount of quarterly volume for the company since Q4-21 when BTC’s price peaked during the last cycle. Despite surging volume, just 18% of it came from retail traders. Furthermore, at just 8 million in the quarter, transacting users of Coinbase was actually down 4.7% year over year in Q1-24:

COIN Transacting Users (The Block)

In my view, the company needs another significant leg higher in crypto asset prices from coins like Bitcoin and Ethereum (ETH-USD) for retail buyer demand to return. Until that happens, I suspect COIN’s share price will struggle. By extension, CONL will struggle as well.

Closing Thoughts

In a little over four months since I last covered CONL for Seeking Alpha, it’s evident that the fund is a poor choice for long term holding. In times of strong uptrends for Coinbase stock, CONL will likely perform very well. But even then I can’t recommend holding CONL for a longer period of time. Holding should likely be measured in days or at most a couple weeks. COIN stock looks weak to me and I see a poor setup from both seasonal and valuation standpoints. In my view, long term investors who want exposure to Coinbase are better off just buying COIN directly and waiting for confirmation of an uptrend before they consider adding CONL for stronger upside. But again, I don’t think we’re at that point yet. CONL is still a ‘sell.’

Read the full article here