A Quick Take On Grid Dynamics

Grid Dynamics Holdings, Inc. (NASDAQ:GDYN) reported its Q2 2023 financial results on August 6, 2023, beating revenue and EPS consensus estimates.

The firm provides a range of IT consulting and related services to organizations seeking to improve their operational efficiencies.

I previously wrote about Grid Dynamics with a Hold outlook after its Q1 2023 financial results.

Company leadership seeks to diversify its client base by industry vertical to less cyclical industries.

While operating losses have been eliminated, revenue growth has stalled, so I remain Neutral [Hold] on Grid Dynamics Holdings, Inc. until management can reignite revenue growth while producing operating profits.

Grid Dynamics Overview

San Ramon, California-based Grid Dynamics was founded in 2006 to provide digital transformation consulting and related services to companies and other organizations worldwide.

The firm is headed by CEO Leonard Livschitz, who was previously president and CEO at LUXERA and VP of Marketing & Business Development at LedEngin.

The company’s primary offerings include the following:

-

Digital transformation

-

Technical consulting

-

Software design, development, testing

-

Internet services operations.

Grid acquires customers through its direct sales and business development efforts and through partner referrals and word of mouth.

According to a 2021 market research report by 360 Market Updates, the global market for digital transformation strategy consulting was an estimated $58.2 billion in 2019 and is forecast to reach $143 billion by 2025.

This represents a forecast CAGR of 16.2% from 2020 to 2025.

The main drivers for this expected growth in IT consulting are a large transition from on-premises, legacy systems to cloud-based environments with complex architectures.

There is also expected growth in the number of industries adopting digital transformation strategies, such as manufacturing, finance, and retail, as well as a growing demand for improved customer experience.

Also, the COVID-19 pandemic has likely pulled forward significant demand to modernize enterprise systems, resulting in increased growth prospects for digital transformation consultancies.

The growth of IT consulting is expected to continue due to the evolving digital landscape, increased demand for improved customer experience, the need to develop and maintain new or better business models, and the accelerated demand for modernization due to the pandemic.

Major competitive or other industry participants include:

-

Globant

-

Thoughtworks

-

EPAM

-

Slalom

-

Accenture

-

Deloitte Digital

-

McKinsey

-

BCG

-

Ideo

-

Cognizant Technology Solutions

-

Capgemini

-

Computer Task Group

-

Company in-house development efforts.

Grid’s Recent Financial Trends

-

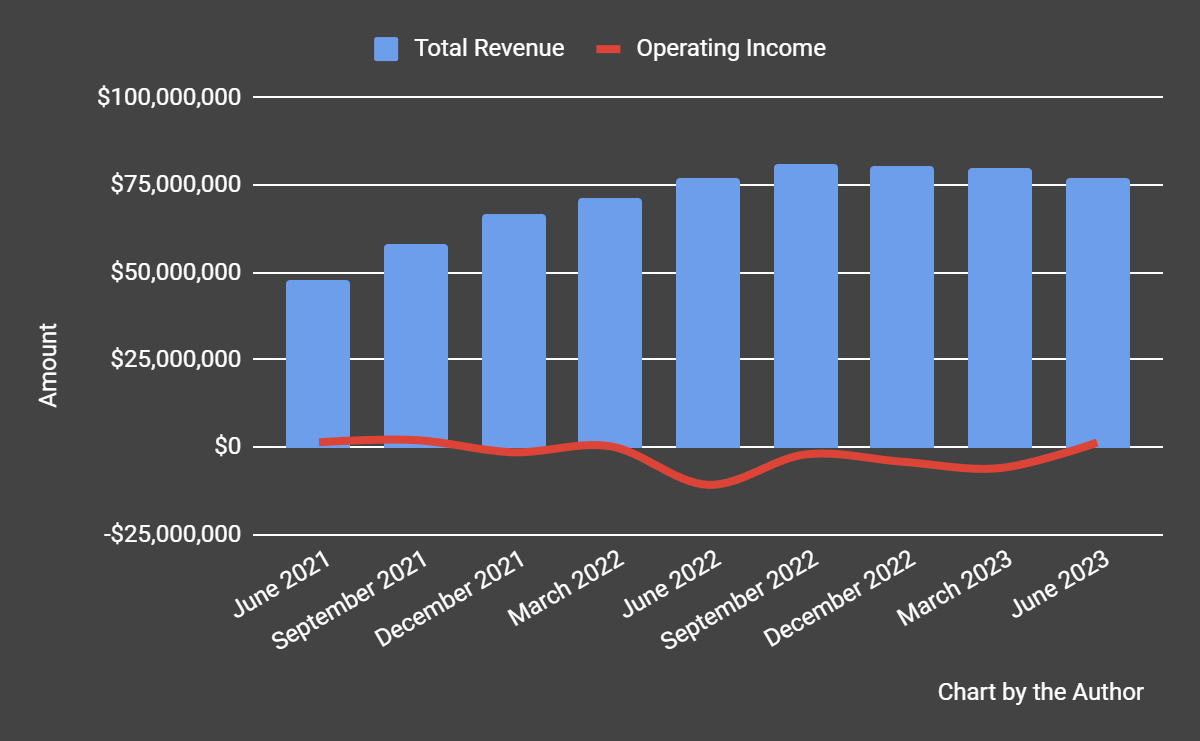

Total revenue by quarter has plateaued; Operating income by quarter has moved into positive territory in the most recent quarter.

Total Revenue and Operating Income (Seeking Alpha)

-

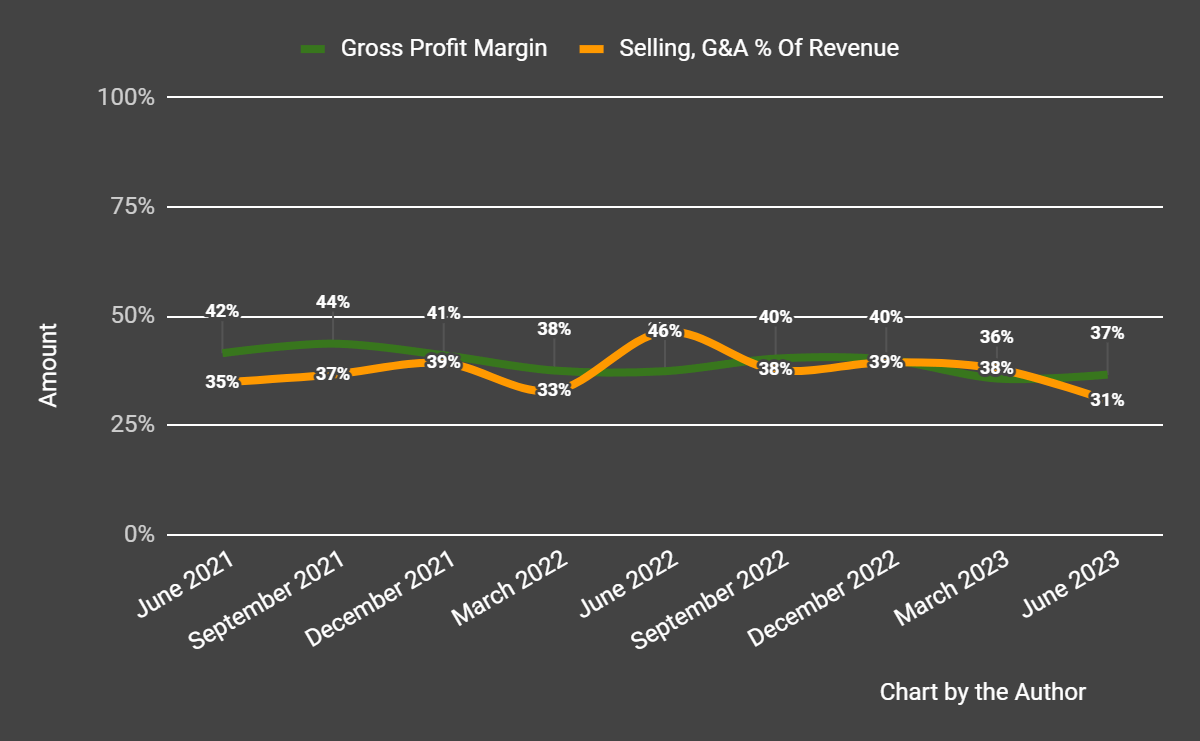

Gross profit margin by quarter has trended lower in recent quarters; Selling, G&A expenses as a percentage of total revenue by quarter have also moved lower more recently, a positive sign indicating improved efficiency.

Gross Profit Margin and Selling, G&A % Of Revenue (Seeking Alpha)

-

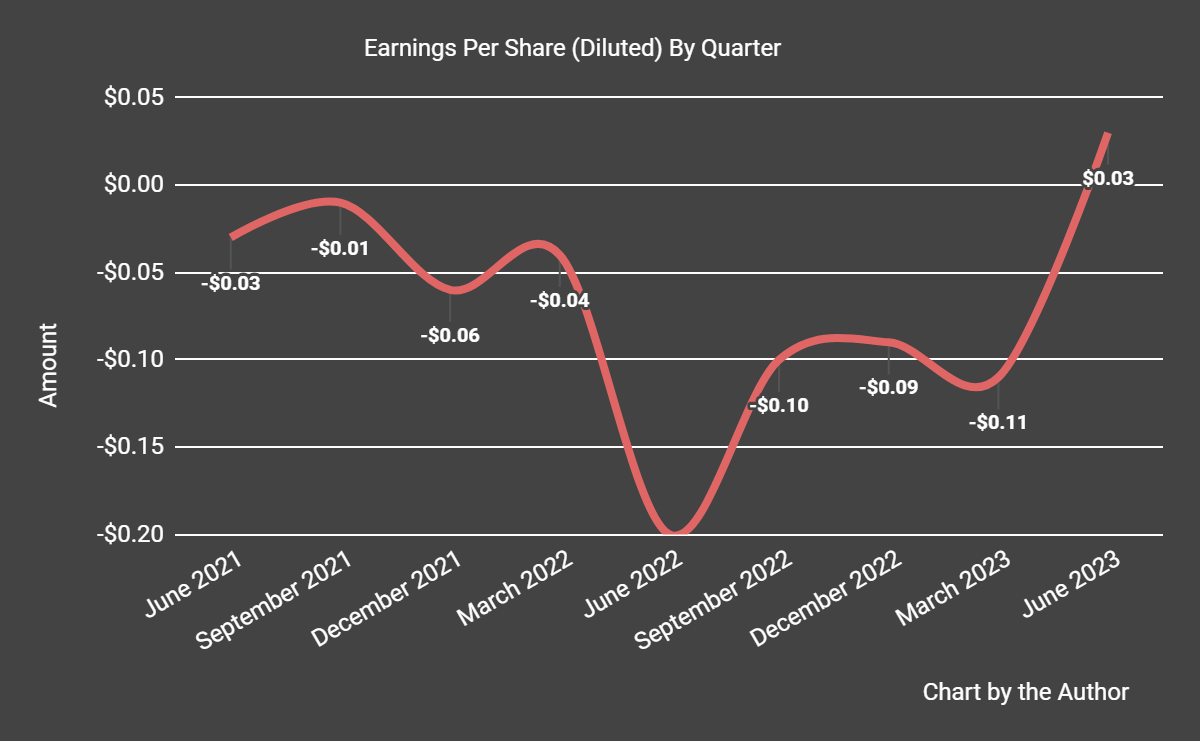

Earnings per share (Diluted) were positive in the most recent quarter.

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP.)

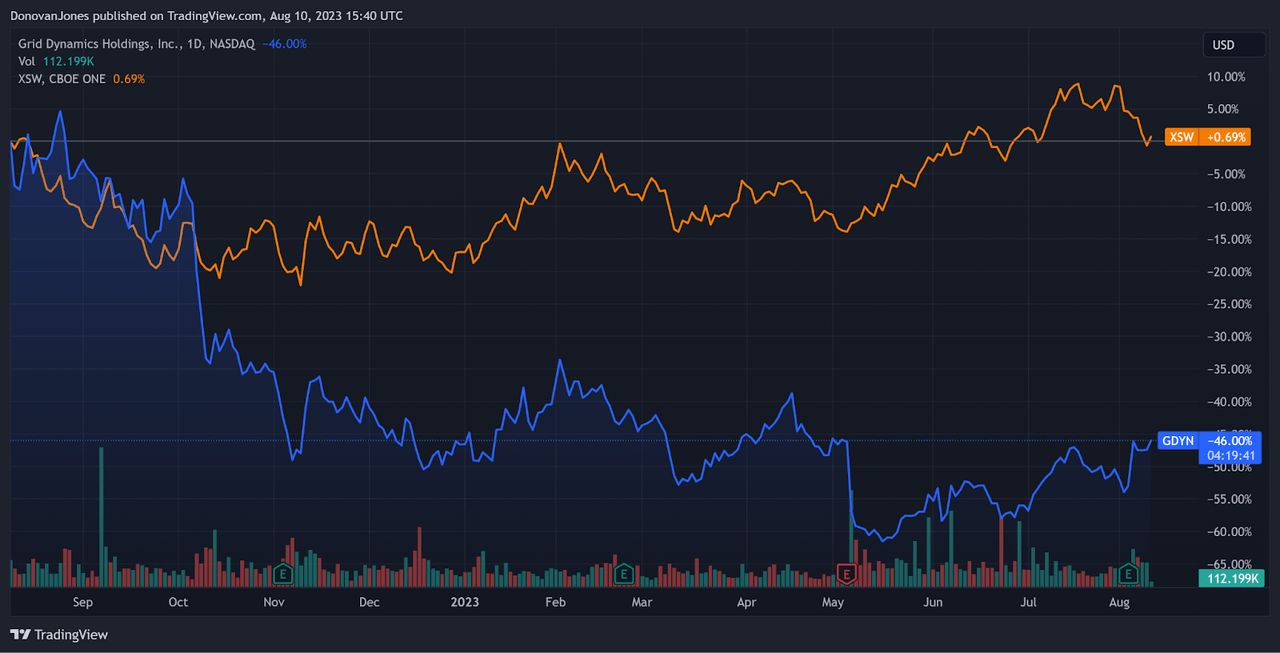

In the past 12 months, GDYN’s stock price has fallen 46% vs. that of the SPDR S&P Software & Services ETF’s (XSW) rise of 0.69%, as the chart indicates below:

52-Week Stock Price Comparison (Seeking Alpha)

For the balance sheet, the firm ended the quarter with $246.2 million in cash and equivalents and no debt.

Over the trailing twelve months, free cash flow was $32.3 million, during which capital expenditures were $6.6 million. The company paid $56.3 million in stock-based compensation in the last four quarters, the third highest trailing twelve-month figure in the past eleven quarters.

Valuation And Other Metrics For Grid Dynamics

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

1.9 |

|

Enterprise Value / EBITDA |

190.9 |

|

Price / Sales |

2.5 |

|

Revenue Growth Rate |

16.8% |

|

Net Income Margin |

-5.9% |

|

EBITDA % |

1.0% |

|

Net Debt To Annual EBITDA |

-79.4 |

|

Market Capitalization |

$830,960,000 |

|

Enterprise Value |

$596,620,000 |

|

Operating Cash Flow |

$38,910,000 |

|

Earnings Per Share (Fully Diluted) |

-$0.27 |

(Source – Seeking Alpha.)

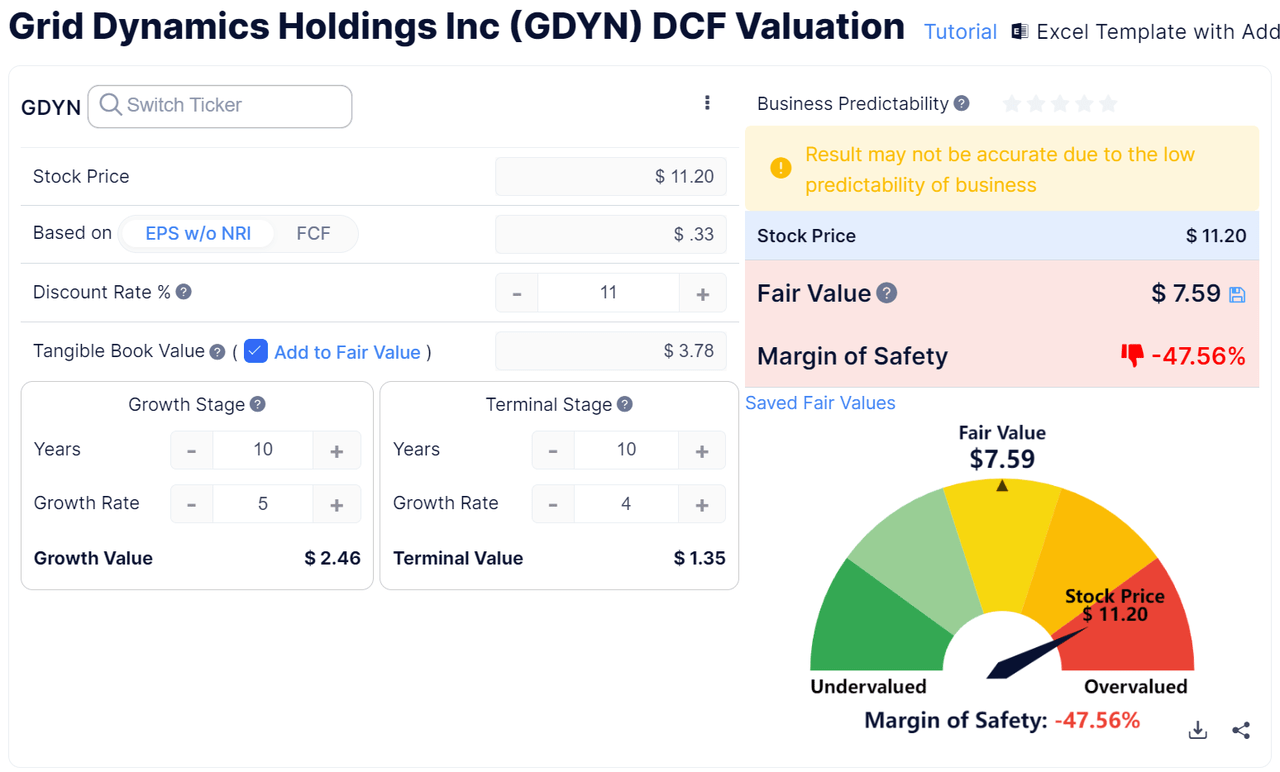

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm’s projected growth and earnings:

Discounted Cash Flow Calculation – GDYN (Guru Focus)

Assuming generous DCF parameters, the firm’s shares would be valued at approximately $7.59 versus the current price of $11.20, indicating they are potentially currently overvalued, with the given earnings, growth, and discount rate assumptions of the DCF.

As a reference, a relevant partial public comparable would be Computer Task Group (CTG); shown below is a comparison of their primary valuation metrics:

|

Metric [TTM] |

Computer Task Group |

Grid Dynamics |

Variance |

|

Enterprise Value / Sales |

0.5 |

1.9 |

246.3% |

|

Enterprise Value / EBITDA |

16.9 |

190.9 |

1030.0% |

|

Revenue Growth Rate |

-18.5% |

16.8% |

–% |

|

Net Income Margin |

0.82 |

-5.9% |

–% |

|

Operating Cash Flow |

$4,450,000 |

$38,910,000 |

774.4% |

(Source – Seeking Alpha.)

Commentary On Grid Dynamics

In its last earnings call (Source – Seeking Alpha), covering Q2 2023’s results, management highlighted its “record net income since becoming a public company” due to new logo customer wins and “deeper relationships with our partnership ecosystem.”

Customers are increasing their interest and demand for “AI” initiatives, however, leadership noted “continued recalibration of spending priorities and investments” as consulting clients across the industry focus on cost-takeout initiatives over “transformation” in their discretionary spending plans.

The firm is also seeing customers move operations offshore in an effort to reduce costs. Leadership believes this trend will be helpful to the company due to its significant offshore delivery capabilities.

Management didn’t disclose any company, customer or employee retention rate metrics, but employee headcount increased 3.2% sequentially, largely due to the acquisition of NextSphere Technologies.

Total revenue for Q2 2023 was flat year-over-year, while gross profit margin dropped slightly by 0.8%.

Selling, G&A expenses as a percentage of revenue dropped 15.8%, a positive sign indicating increased efficiency, and operating income moved into positive territory at $1.8 million.

The company’s financial position is strong, with ample liquidity, no debt and plenty of free cash flow.

Looking ahead, consensus full-year 2023 revenue expectations are at 0.2% growth over 2022.

If achieved, this would represent a sharp drop in revenue growth versus 2022’s growth rate of 80% over 2021.

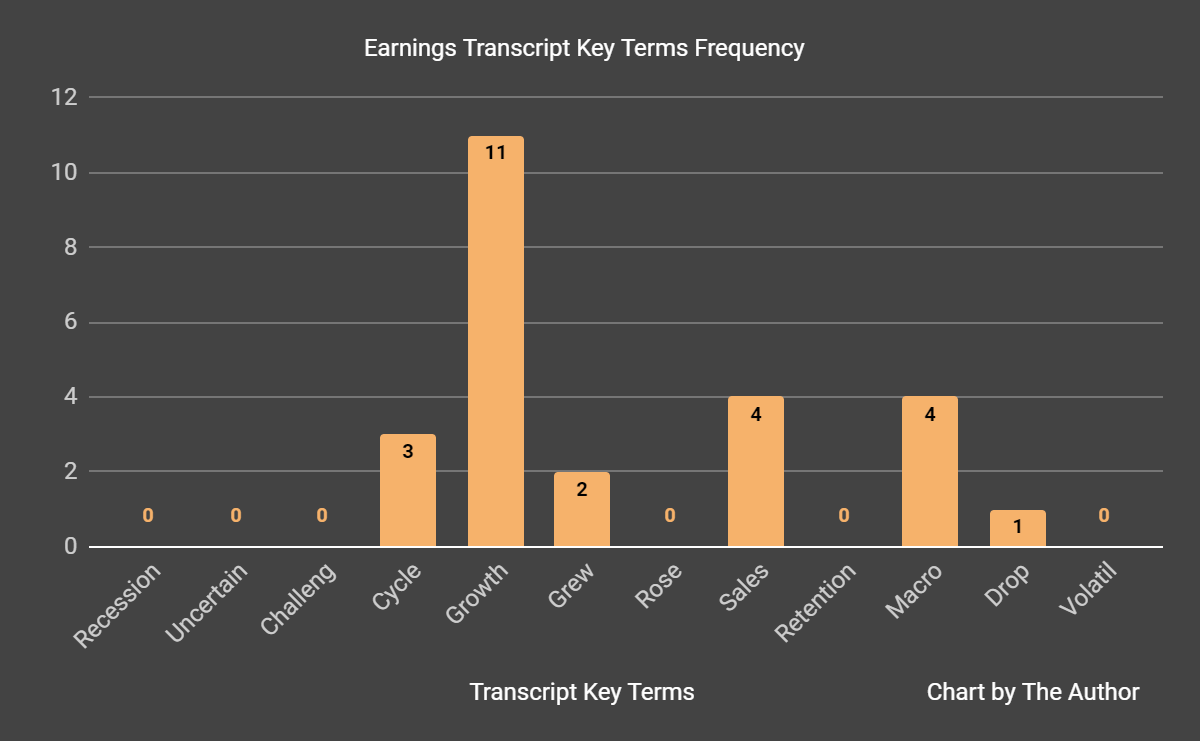

From management’s most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below:

Earnings Transcript Key Terms Frequency (Seeking Alpha)

I’m most interested in the frequency of potentially negative terms, so management or analyst questions cited “Macro” four times and “Drop” once.

Analysts questioned company leadership about its AI-related activities.

Management noted that it is seeing the strongest demand from the retail vertical. The company has been working on AI technologies for several years, so it believes it is ahead of competitors who are at the front end of their learning process.

Regarding valuation, my discounted cash flow calculation indicates the stock may be overvalued at its present price level of around $11.20, and that assumes a 5% revenue growth rate, which apparently the company will not achieve in 2023.

While operating losses have been eliminated, revenue growth has stalled, so I remain Neutral [Hold] on Grid Dynamics Holdings, Inc. until management can reignite revenue growth while producing operating profits.

Read the full article here