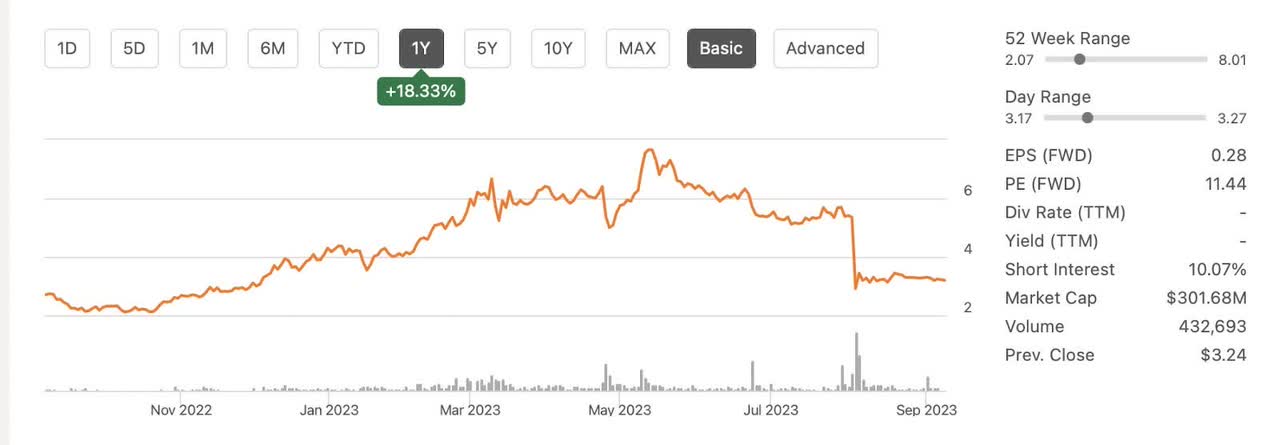

Many of my biggest winners in my portfolio come from biotech. The volatility in the sector creates extreme price movements and the herd mentality of many investors has them chasing the latest fad. Frequently data from drug trials is a boom or bust scenario where speculators call their shots and herds of followers run off the same cliffs. In regards to Assertio Holdings (NASDAQ:ASRT), this scenario has played out a few times in recent history. This year the stock has moved from a high of $8.01 to a low of $2.07. Given its current price of $3.05, we currently rate Assertio a strong buy and believe it could double.

Buying the hype in ASRT has almost always caused pain and buying the pain has almost always provided gains. Today even though Assertio is up 18% over the past year; its stock price appears to once again be reeling in pain. Call me a glutton for punishment but I love looking at these types of opportunities. I enjoy looking at the ghosts of bagholders past and looking for hidden gems.

Seeking Alpha

Assertio Holdings, Inc., a prominent player in the commercial pharmaceutical sector, specializes in delivering medications within the fields of neurology, rheumatology, and pain and inflammation. Their diverse pharmaceutical portfolio includes products like INDOCIN, an effective solution for various rheumatoid arthritis conditions, as well as treatments for seizures related to lennox-gastaut syndrome, migraines, pain relief, and more. This pharmaceutical company caters to a wide range of medical needs, ensuring patients have access to essential treatments across several therapeutic areas.

As a company that seeks to reduce patients’ pain, ASRT ironically has caused its investors quite a bit of pain throughout its history. This painful journey has promised many rewards but has yet to truly deliver. Despite this pain, consensus estimates believe growth will continue in 2024. If these earnings turn out to be true, ASRT should be worth over $5.

A rough calculation of earnings estimate of .46 times the current PE of 11 would place the value of ASRT at about $5.04. Although we acknowledge this to be a rough estimate, we are confident that it puts us within a fair value range. The real difficulty in evaluating ASRT is the unpredictability of earnings.

Seeking Alpha

Historically, ASRT predicted revenues have been fairly accurate but earnings have not been.

Revenue (Seeking Alpha) Earnings (Seeking Alpha)

This makes predictions difficult. The good news is that ASRT has surprised to the upside recently and financially appears to be in a better position than it has been in the past and the company is already priced for revenue loss as opposed to growth. This presents a margin of safety of around 27% if estimates are proven true. The downside risk would be any difficulties integrating spectrum or loss of revenue from drugs facing competition due to the loss of exclusivity. I believe these concerns are possible but not probable.

The acquisition of Spectrum should improve growth and drive revenue estimates. ROLVEDON’s 34% quarterly growth alone should drive earnings growth in 2024. With only 2% of market share, ROLVEDON’s prospects for growth are quite good and are a primary catalyst for the combined company to reach earnings estimates in 2024. This also allows for surprises to the upside in ASRT’s current line-up of FDA-approved drugs and makes ASRT a possible deep value play when looking at the future potential sales.

With the following eight drugs approved by the FDA, Assertio has made continued profitability possible but it must execute.

Assertio Website

This shows tremendous growth because a mere 3.5 years ago, Assertio found itself in a precarious financial position, saddled with debt and having strategically invested in only two assets, CAMBIA and ZIPSOR. According to CEO Dan Peisert, the company is in a much better position now, “Today, those two assets together represent only 7% of our second quarter net product sales and only 4.6%, if you improve over down sales. In that time, we’ve acquired two businesses and two additional assets and paid off $195 million of debt. Our financial discipline and specifically our focus on cash flows is what has contributed to this success to date.

Now, with a healthier balance sheet and a growth asset, that discipline will still be there to help foster this company toward sustainable growth. We’ve proven we can manage through the ups and downs of loss of exclusivity, and we’ve built and now acquired a first-class commercial team from Spectrum. That can only enhance our capabilities to grow assets and scale.

Assertio’s ability to pivot and diversify its asset portfolio, thereby reducing overreliance on a select few products makes a big difference. Such diversification is paramount in the pharmaceutical industry, given the potential impact of patent expirations and evolving market dynamics on a company’s financial stability.

The improved balance sheet positions Assertio favorably for future growth endeavors. With a stronger financial foundation, the company is better poised to capitalize on emerging opportunities, be they organic growth initiatives or strategic acquisitions. The unwavering commitment to financial prudence ensures that ASRT will continue to pursue a sustainable growth trajectory, with the utmost consideration for shareholder interests.

The adept management of challenges such as the loss of exclusivity demonstrates Assertio’s resilience in navigating industry headwinds. This track record inspires confidence in the company’s ability to weather uncertainties and consistently deliver value to shareholders. Moreover, the acquisition of a world-class commercial team from Spectrum augments Assertio’s capabilities to drive asset growth and expand its market footprint.

Assertio’s transition from a heavily concentrated portfolio to a diversified, financially robust entity is impressive. This transformation positions the company for sustained growth and underscores its capacity to thrive in a dynamic industry environment. With a solidified balance sheet and a strategic vision for expansion, Assertio stands poised for a promising and prosperous future if it can continue to deliver on its promises.

Highlights From Recent Earnings Call

-

ROLVEDON’s launch trajectory remains highly positive.

-

Q2 2023 net sales reached $21 million, a 34% increase from Q1.

-

Third consecutive quarter of exceptional performance.

-

Credit to the experienced team for differentiation in a competitive market.

-

Significant progress in expanding customer base in terms of breadth and depth.

-

Targeted accounts purchasing ROLVEDON increased by 50% in Q2.

-

Expansion into the second largest GPO, representing approximately 40% of the Community Oncology business.

-

Successful execution of the focused launch strategy.

-

ROLVEDON currently holds approximately 2% market share in the long-acting GCSF market.

-

Withdrawal of guidance due to FDA approval of a generic indomethacin product.

-

Announcement of a single competitor receiving CGT status, granting them exclusivity for 180 days.

-

Assertio’s preparedness and readiness for generic entry.

-

Successful performance in retaining market share after losing exclusivity for CAMBIA.

-

Outstanding execution of commercial team and market access programs.

-

Confidence in retaining market share for INDOCIN with only one competitor.

-

Discontinuation of OXAYDO, marking the company’s exit from the opioid business.

-

Positive progress in opioid litigation, with dismissals from a significant portion of cases.

-

Growth and trends in SYMPAZAN, including higher strength product demand and increased net revenues.

-

Recovery and growth in OTREXUP volumes and net revenues, emphasizing smart and disciplined contracting and market access strategies.

From a deep value investor’s perspective, several critical points emerge from the provided information. First and foremost, the withdrawal of guidance due to the FDA’s approval of a generic indomethacin product highlights the dynamic and sometimes unpredictable nature of the pharmaceutical market. It underscores the need for prudent risk management in the face of regulatory changes and competitive pressures.

The announcement of a single competitor receiving CGT status, granting them a 180-day exclusivity period, introduces an element of uncertainty but also an opportunity for Assertio to demonstrate its resilience. The company’s preparedness for generic entry, as mentioned, suggests a proactive approach to mitigate potential revenue impact.

The successful retention of market share after losing exclusivity for CAMBIA is a testament to Assertio’s strong execution capabilities. This achievement, in the face of competition and market dynamics, reflects the company’s ability to adapt and maintain a foothold in the pharmaceutical space.

The announcement of discontinuing OXAYDO and exiting the opioid business marks a significant strategic shift. While this decision may have a short-term drag on financial results, it aligns with broader industry trends toward responsible opioid management, which could be seen positively by investors looking for ethical and sustainable business practices. It also will make sure that the company limits exposure to future liability and dedicates itself to non-opioid pain management.

The positive progress in opioid litigation, with dismissals from over 40% of cases without financial penalties, signifies a potential reduction in future legal liabilities for the company. This could contribute positively to Assertio’s financial stability and long-term value and demonstrates that perhaps Assertio’s culpability in the production of opioids will be less than other companies. If the overhang of future lawsuits becomes more limited this would improve the company’s future prospects quite a bit.

The growth and trends in SYMPAZAN, along with the focus on profitable volumes, are noteworthy. It suggests a strategic approach to product management and revenue generation, which can be attractive to investors seeking sustainable growth.

The recovery and growth in OTREXUP volumes and net revenues, in contrast to a competitor’s declining performance, highlight Assertio’s effective business strategy. This approach, grounded in smart and disciplined contracting, could be seen as a key driver of profitability and long-term shareholder value.

These points offer a nuanced view of Assertio’s operational dynamics, resilience in a competitive environment, and strategic shifts that may influence its long-term investment appeal for value-focused investors.

The Risks

Generic Competition: The FDA’s approval of a generic indomethacin product poses a significant risk to Assertio’s revenue and market share, particularly if the competitor launches successfully and gains a substantial foothold. The exclusivity period granted to the competitor further compounds this risk.

Market and Regulatory Uncertainty: The pharmaceutical industry is subject to regulatory changes and market dynamics that can be challenging to predict. The withdrawal of guidance due to the generic approval illustrates the uncertainty inherent in the industry, making it difficult for the company to provide accurate forecasts.

Legal Liabilities: While Assertio has seen progress in opioid litigation, it remains exposed to potential legal liabilities related to past products and practices. Unforeseen legal developments could result in financial penalties or reputational damage.

Product Discontinuation: The decision to discontinue OXAYDO and exit the opioid business, while aligned with ethical considerations, may have a negative impact on the company’s financial performance in the short term. There is a risk that this move could lead to revenue loss and necessitate the development of alternative revenue sources.

Competitive Pressures: The pharmaceutical industry is highly competitive, and Assertio faces challenges in maintaining and growing its market share, particularly in crowded therapeutic areas. Competitive pressures can impact pricing, market access, and profitability.

Market Access and Reimbursement: Assertio’s success relies on securing favorable market access and reimbursement agreements. Changes in reimbursement policies or difficulties in securing agreements with payers could adversely affect revenue.

Product Concentration: The company’s revenue may be concentrated in a few key products, as seen with CAMBIA and ZIPSOR. Overreliance on a limited product portfolio increases vulnerability to generic competition and market fluctuations.

Execution Risks: Assertio’s ability to defend its market share and execute strategies effectively, such as its response to generic competition, relies on the performance of its commercial teams and market access programs. Any missteps in execution could result in revenue erosion.

Market Shifts: Shifts in market trends, such as changes in prescribing practices or treatment preferences, could impact the demand for Assertio’s products. Staying aligned with evolving market dynamics is crucial.

Supply Chain and Operational Risks: Supply chain disruptions or operational challenges, as experienced with OXAYDO, can disrupt product availability and negatively affect financial performance.

Regulatory Compliance: Compliance with evolving pharmaceutical regulations is critical. Any failure to meet regulatory requirements could result in penalties or product recalls.

Integration Challenges: The integration of Spectrum and the continued launch trajectory of ROLVEDON pose risks related to operational integration, cultural alignment, and execution.

Final Thoughts

Assertio Holdings, Inc. presents a complex investment opportunity with both promising aspects and inherent risks. From a historical perspective, it’s evident that investing based on market hype or the herd mentality has often led to pain for shareholders. However, taking a contrarian approach and buying during challenging periods has frequently yielded gains. The current environment suggests that ASRT might be trading near a current bottom and sentiment is not very good. The uncertainty regarding liability and competition provides an opportunity to buy shares at a reasonable price.

Despite the extreme price volatility of Assertio, the company exhibits a commitment to growth and diversification, transitioning from a precarious financial position to a more robust one over a relatively short period. Key drivers of this transformation include disciplined financial management, strategic acquisitions, and a focus on cash flows.

While the company has shown resilience in the face of generic competition and has demonstrated its ability to manage through industry challenges, it remains exposed to several risks. The approval of a generic indomethacin product, market and regulatory uncertainties, legal liabilities, and the discontinuation of certain products pose immediate challenges. Assertio’s success hinges on its ability to navigate these risks effectively.

In evaluating Assertio Holdings as an investment, investors should carefully weigh the potential rewards against the inherent risks. The company’s ability to adapt to a changing pharmaceutical landscape, capitalize on growth opportunities, and manage its risks will be crucial factors in determining its long-term performance. The successful integration of Spectrum and the continued trajectory of ROLVEDON will play pivotal roles in shaping the company’s future. Investors considering Assertio should conduct thorough due diligence and consider their risk tolerance and investment horizon carefully. Although we currently rate ASRT as a strong speculative buy, we acknowledge that the price will move in a large range. Investors looking to avoid uncertainty and volatility should look elsewhere. As always please do your own due diligence before buying any positions and good luck investing. If you liked this article, please follow and like. Thank you for reading.

Read the full article here