Investment Outlook

Guidewire Software (NYSE:GWRE) recently reported its FQ3 2024 financial results, beating both revenue and earnings consensus estimates.

I previously wrote about GWRE in February with a Buy outlook due to an improving insurer outlook and scalable revenue mix.

Since then, most of the company’s performance improvement has come from negative operating margin reduction and its stock has been heavily re-rated by the market over the past 12 months.

I’m not certain whether management can continue to produce upside in a possibly fully valued stock price with essentially static revenue growth, so I’m now Neutral (Hold) on Guidewire Software, Inc.

Guidewire’s Model And Market

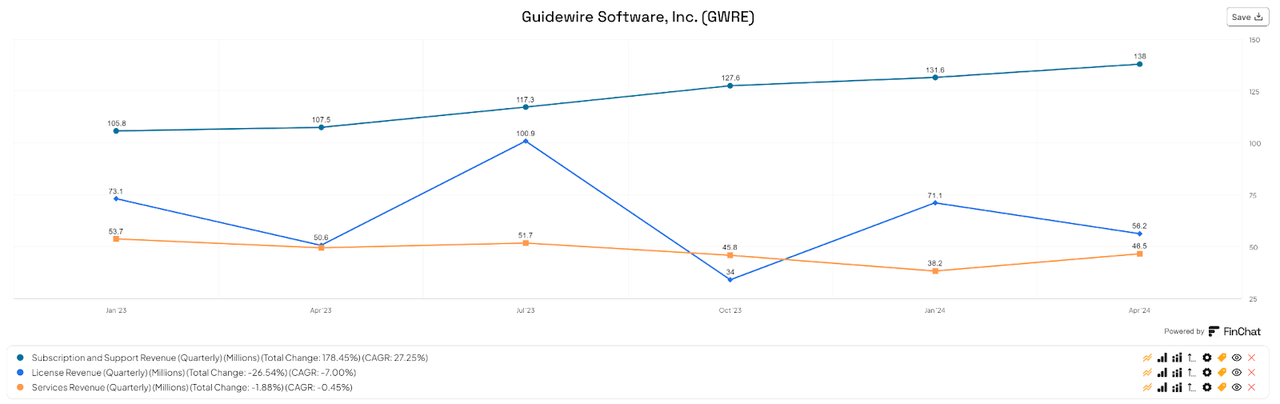

Guidewire’s primary revenue sources are subscription & support, licenses and professional services, with subscription and support revenue being the primary revenue driver as the chart shows here:

FinChat.io

The company still has a significant customer base on its legacy, on-premises, perpetual license offerings, but management continues to encourage these customers to migrate to the cloud.

Global insurance operations software was an estimated $11.6 billion market in 2021 and is expected to exceed $32 billion by 2032, per a market research report by Business Research Insights.

This expected growth rate would represent a CAGR of 9.73% from 2022 to 2032.

The main reasons for this forecasted growth are the demand from Property & Casualty insurance companies to increase efficiencies in their underwriting, risk assessment and claims processes via digital processes.

AI-enabled features will also likely provide growth opportunities for software companies and clients through improved data collection and analysis on a faster and sometimes near real-time basis.

Recent Financial Trends

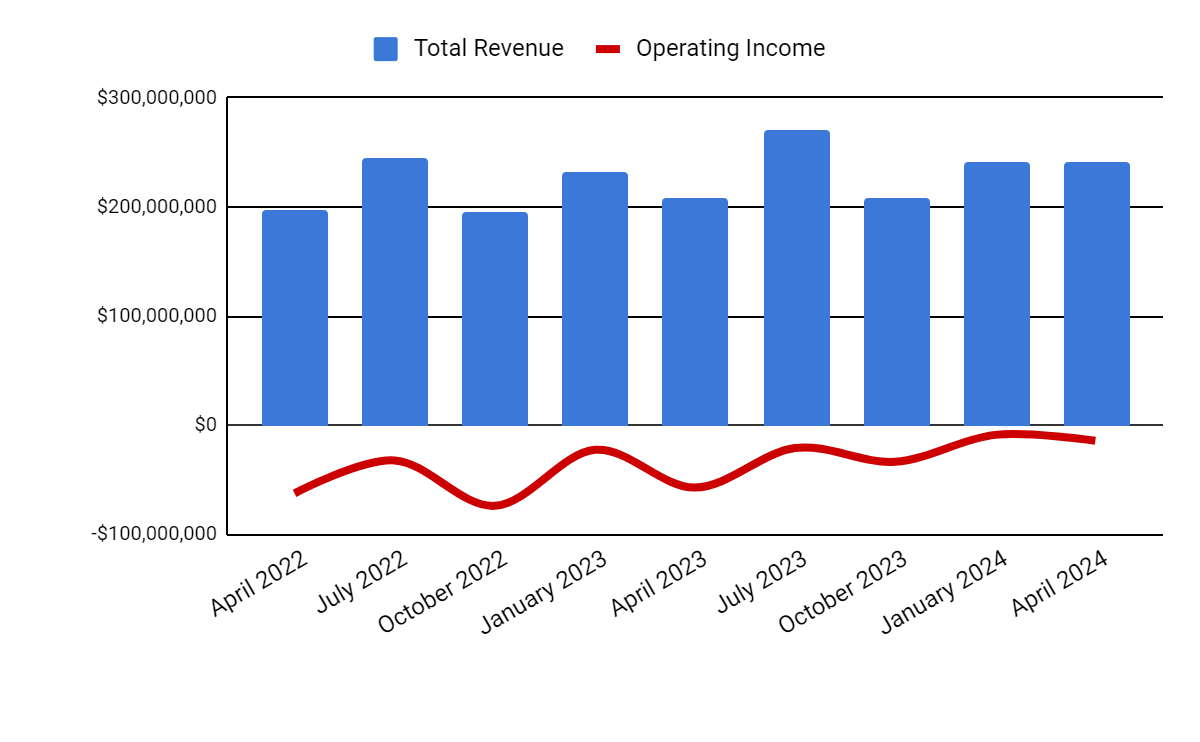

Total revenue by quarter (columns) has risen year-over-year due to stronger demand from insurance companies becoming more comfortable with longer-term decision-making as inflation pressures have eased; Operating income by quarter (line) has trended closer toward breakeven because of lower than expected operating expenses as a function of revenue growth.

Seeking Alpha

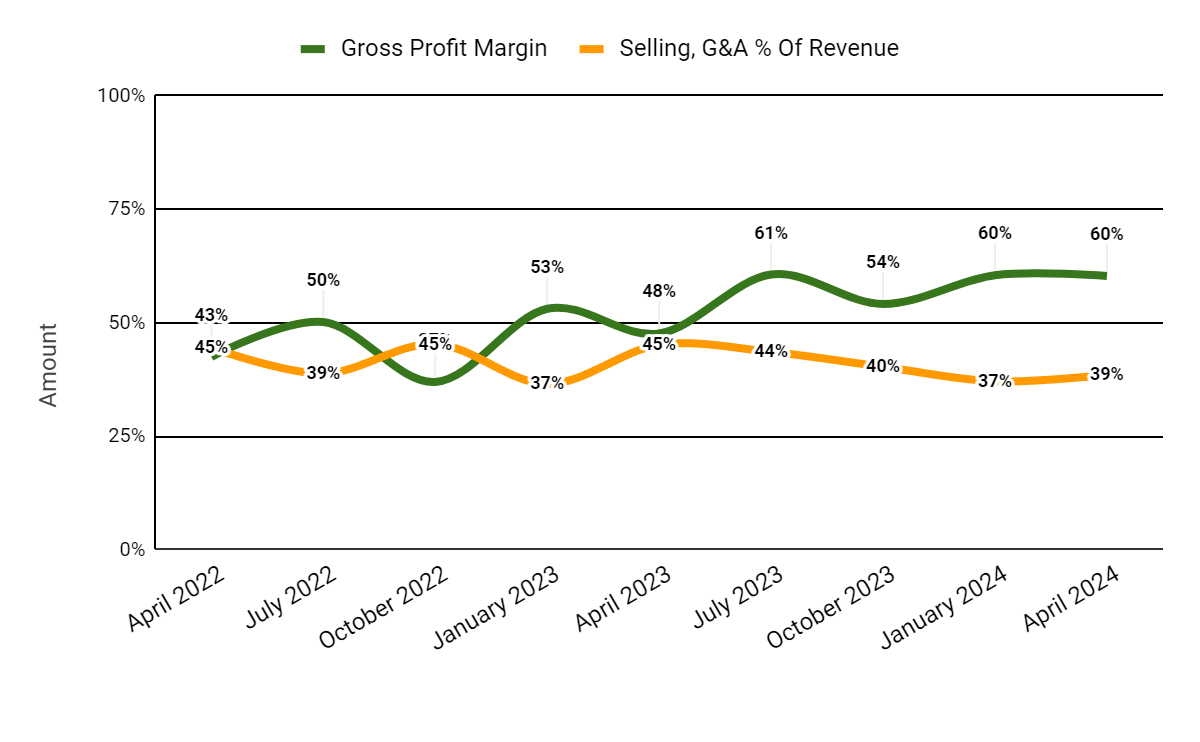

Gross profit margin by quarter (green line) has continued to rise as a result of improved economies of scale; Selling and G&A expenses as a percentage of total revenue by quarter (orange line) have dropped due to year-over-year revenue growth on existing cost structures.

Seeking Alpha

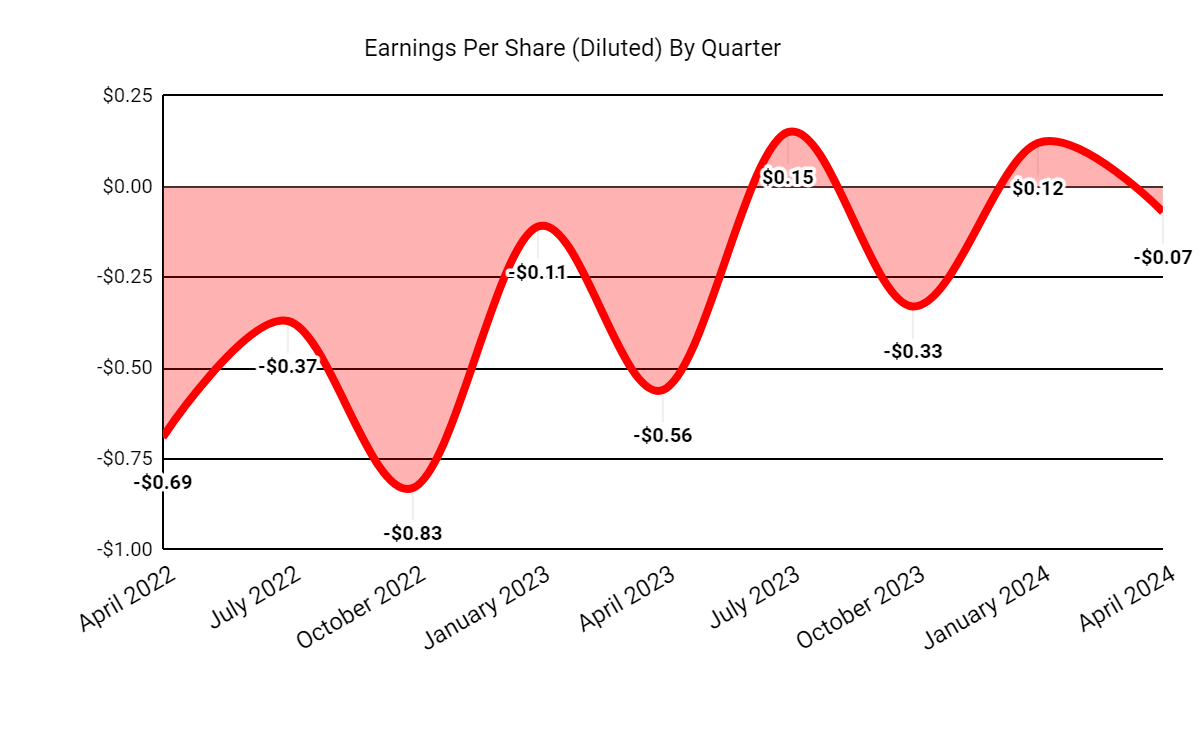

Earnings per share (Diluted) have continued to trend unevenly higher as a result of seasonal factors and continued subscription revenue growth.

Seeking Alpha

(All data in the above charts is GAAP.)

For balance sheet results, GWRE ended the quarter with $782.3 million in cash, equivalents and short-term investments and $398.5 million in total debt, all of which is due in less than 12 months (current portion).

Over the trailing twelve months, free cash flow was $167.3 million and capital expenditures were only $7.9 million. However, Guidewire has paid a hefty $145.7 million in stock-based compensation in the last four quarters.

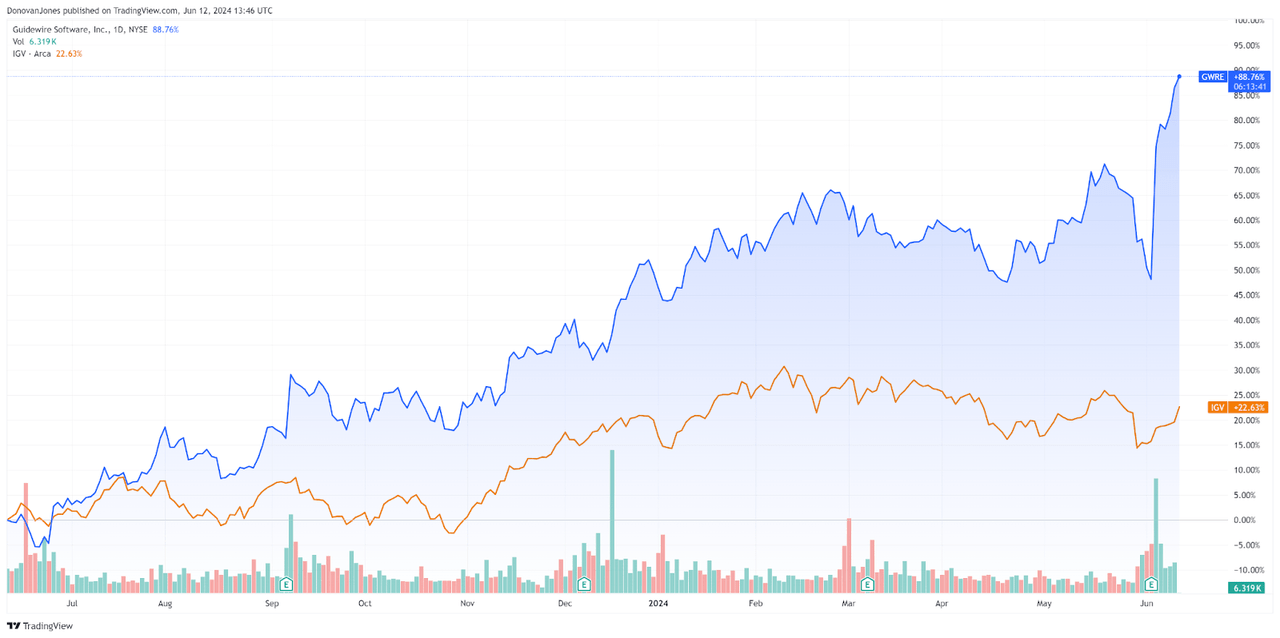

In the past year, GWRE’s stock price has risen by 88.8% vs. that of the iShares Expanded Technology-Software ETF’s (IGV) gain of 22.6%, as the chart shows below.

TradingView

Here is a major financial and operating metrics table indicating an increasing forward revenue growth estimate and a “Strong Buy” score from Seeking Alpha’s Quant calculation.

|

Metric |

Amount |

|

EV/Sales (“FWD”) |

10.9 |

|

EV/EBITDA (“FWD”) |

89.4 |

|

Price/Sales (“TTM”) |

11.3 |

|

Revenue Growth (“YoY”) |

9.0% |

|

Net Income Margin |

-1.1% |

|

EBITDA Margin |

-4.6% |

|

Market Capitalization |

$10,930,000,000 |

|

Enterprise Value |

$10,590,000,000 |

|

Operating Cash Flow |

$175,210,000 |

|

Earnings Per Share (Fully Diluted) |

-$0.13 |

|

2024 FWD EPS Estimate |

$1.27 |

|

Rev. Growth Estimate (“FWD”) |

10.4% |

|

Free Cash Flow/Share (“TTM”) |

$1.89 |

|

Seeking Alpha Quant Score |

Strong Buy – 4.82 |

(Source: Seeking Alpha.)

GWRE’s Rule of 40 performance has improved markedly from the first fiscal quarter to the third, but all the improvement has been from operating margin, which has been reduced from negative (16.1%) to negative (5.9%), as the table shows here:

|

Rule of 40 Performance (Unadjusted) |

FQ1 2024 |

FQ3 2024 |

|

Revenue Growth % |

9.0% |

9.0% |

|

Operating Margin |

-16.1% |

-5.9% |

|

Total |

-7.1% |

3.1% |

(Source: Seeking Alpha Data.)

Why I’m Neutral On Guidewire Software

Guidewire is seeing a rebound in demand from insurance companies that are less hesitant to make spending decisions, now that the ‘great inflation’ period of the post pandemic era continues to abate.

The company is seeing increasing strength in the Asia Pacific region, with four cloud migration deals in Australia and growing engagement by prospects in the UK and Japan.

GWRE closed eight InsuranceSuite cloud deals in FQ3, growing its backlog by 33% YoY and highlighting the focus on its subscription business and revenue model

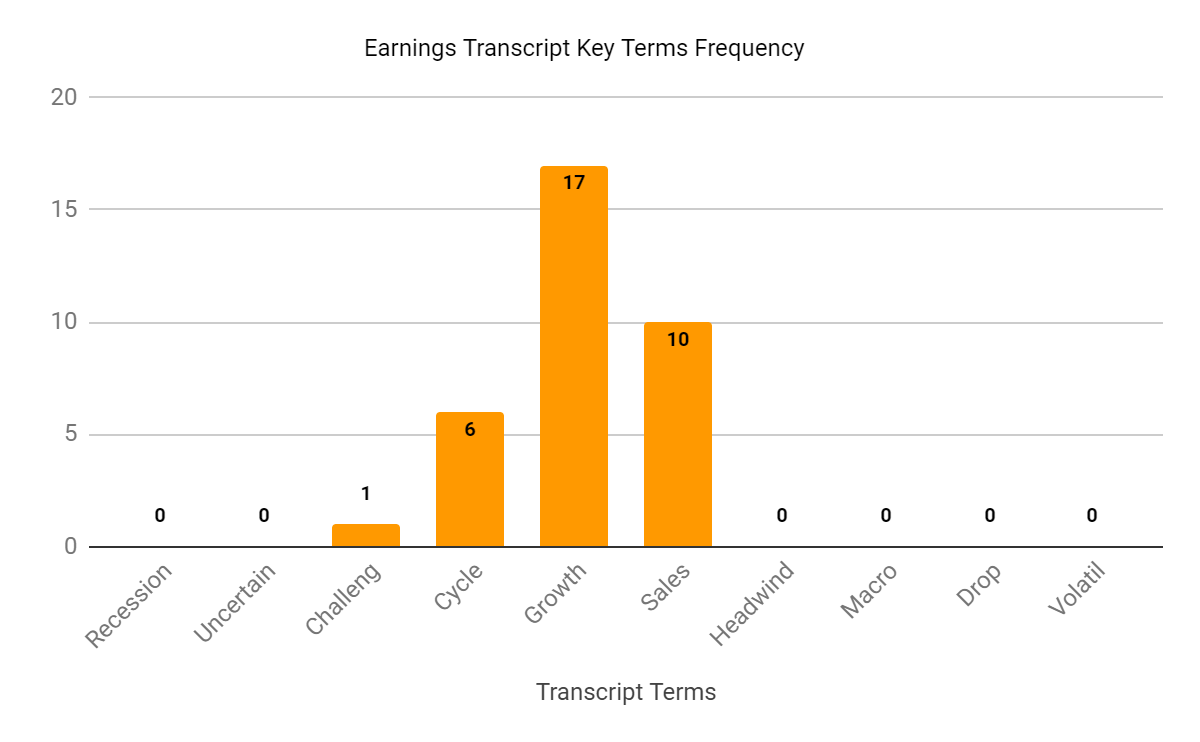

The graphic below shows the frequency of various keywords and terms cited in the most recent management conference call with analysts.

Seeking Alpha

I’m interested in the frequency of negative terms and the chart indicates few of these terms, either from management or from analyst questions, so I see a positive sentiment indicator for Guidewire.

Management sees generative AI as an important avenue for growth and launched its Jutro platform for clients to build various capabilities on top of its platform and data sources.

As to valuation, the market is valuing GWRE at an EV/Sales multiple of about 11x on an estimated NTM revenue growth rate of 10.4% against a median Meritech SaaS Index implied ARR growth rate of around 18% (Source).

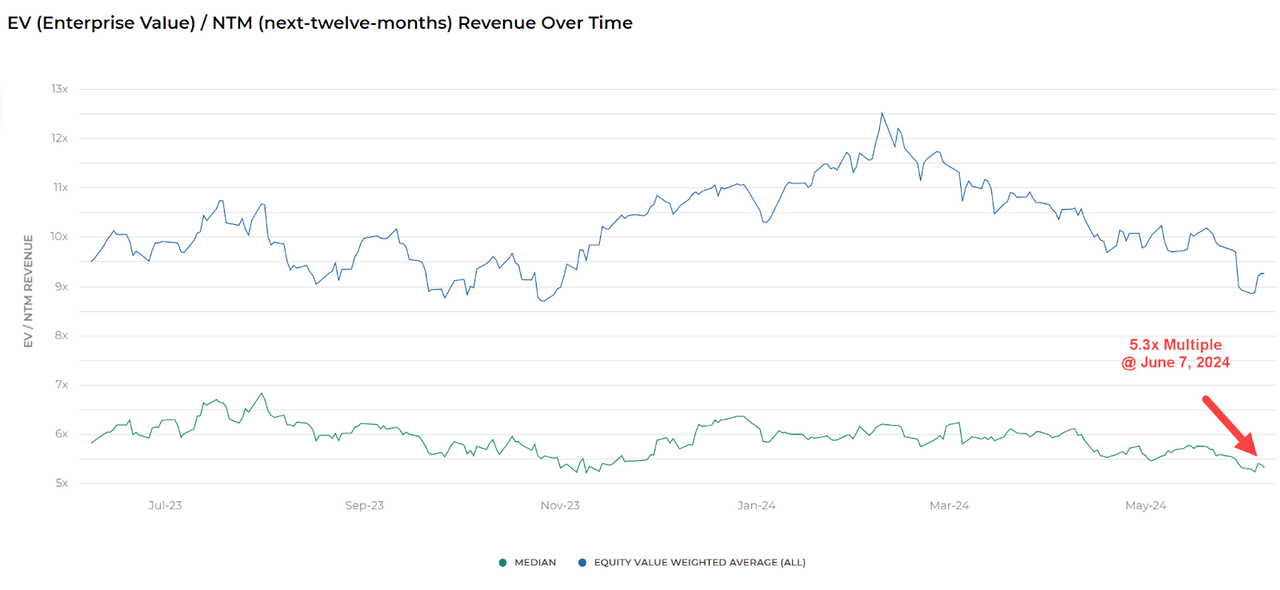

The Meritech Capital Index of publicly held SaaS application software companies showed a forward EV/Revenue multiple median of around 5.3x on June 7, 2024, as the chart shows here:

Meritech Capital

So, by comparison, GWRE is presently being valued by the market at more than double the broader Meritech Capital SaaS Index, as of June 7, 2024.

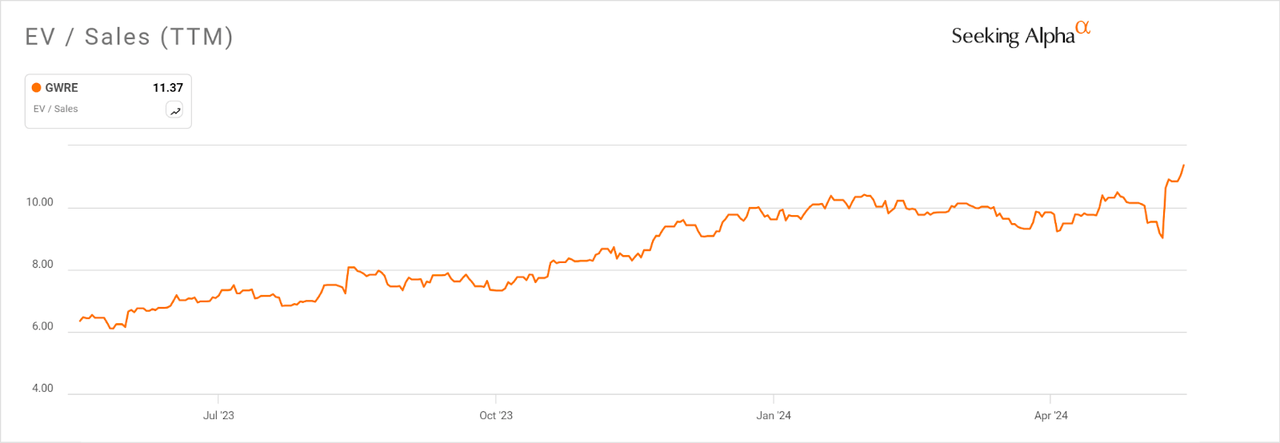

Furthermore, GWRE’s EV/Sales multiple has almost doubled in the past year, as the Seeking Alpha chart shows here:

Seeking Alpha

So, the market has re-rated GWRE’s EV/Sales multiple as inflation has cooled, insurers have begun making buying decisions and the company’s operating losses have been reduced.

But does GWRE have a significant price growth runway for upside ahead? I suppose it depends on whether you believe inflation will continue to abate further and the company will make additional progress on earnings per share.

I confess to being in a ‘wait-and-see’ mode, as over the past year, we may have seen previously delayed buying decisions, i.e., pent-up demand, show up in the company’s revenue figures and forward growth may be more muted.

All the company’s Rule of 40 performance improvement has come from reduced negative operating margin, not a strong increase in revenue growth.

While this development has been a welcome one, I’m more cautious about the company’s ability to drive further performance and stock upside.

So, in the short term, I’m Neutral (Hold) on GWRE as we wait to see whether its operating margin continues to improve.

Read the full article here