The Hershey Company (HSY) manufactures and sells candies and snack products through a range of brands, including Hershey’s, Kit Kat, Reese’s, and Jolly Rancher among a number of other names.

Amid slowing inflation and discretionary spending, ERP implementation, cocoa prices shooting up, and other factors piling against Hershey, the company’s Q2 report showed significant financial weakness after the company’s incredibly resilient long-term financial history. I believe that Hershey is well positioned to push through the headwinds with Hershey’s great positioning in the industry.

The stock has returned well, appreciating at a CAGR of 7.8% in the past decade in the low-risk industry despite the stock still trailing well below the 2023 peak level. On top, Hershey pays a dividend with a current yield of 2.79%.

Ten Year Stock Chart (Seeking Alpha)

Hershey’s History Shows Resilient Growth

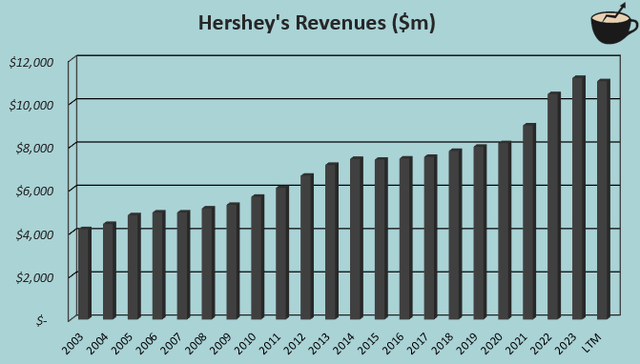

Hershey’s long-term history doesn’t show notable hiccups in performance – the company has grown its revenues at a CAGR of 5.0% from 2003 to 2023 with periods of higher and lower growth. The company’s very extensive portfolio of brands has worked as a foundation to build on new brands and categories while maintaining sales with the company’s more established names.

Author’s Calculation Using TIKR Data

Coupled with stable revenue growth, Hershey has pushed its margin level into an incredibly good level over the long term. In 2023, the operating margin stood at a great 22.7% level, even higher than the company’s historical level as Hershey still seems to be achieving slow operating leverage at its large scale.

As such, Hershey’s earnings growth profile has been incredibly stable and good over the long term. Hershey’s five-year average return on capital of 17.5% is incredibly good in the low-risk industry.

Headwinds Are Piling Against Hershey

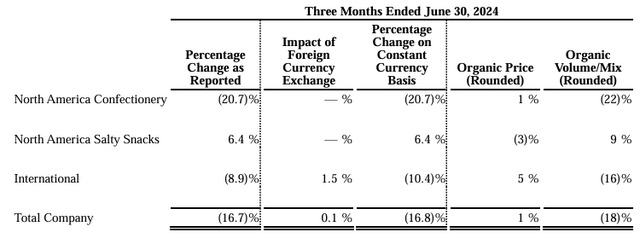

Yet, despite a strong and stable history, headwinds are now increasingly piling against Hershey, ranging from temporary to potentially more persisting threats. The company’s Q2 results showed a -16.7% revenue decline and a -48.7% operating income decrease, being Hershey’s largest quarterly hiccup at least in the past decade. The company also lowered its 2024 guidance from 2-3% sales growth to ~2%, and lowered the adjusted earnings per share to “down slightly” from a previously flat expectation.

Hershey’s Q2 Segment Performance (HSY Q2 Press Release)

Several factors piled onto the results and guidance, including:

1. ERP Implementation & Retailer Inventory Balancing

The most notable, and very temporary factor contributing to Q2 weakness, was Hershey’s ERP system implementation – the implementation of a new management system is expected to streamline operations going forward, but caused manufacturing and delivery disruptions that Hershey estimates to have contributed for around 9 percentage points of the -16.7% Q2 decline. The ERP implementation could still cause sales turbulence in the future, but the largest part of the negative impact seems to have been in Q2 with the April implementation. For the long term, the ERP implementation only looks to streamline Hershey’s operations and earnings, not being a persistent risk.

Retailers’ inventory management was also estimated to have had around a 7 percentage point adverse sales effect in Q2, but is expected to reverse in the second half of 2024; combined, the ERP implementation and retailer balancing contributed to most of the decline.

2. Lower Inflation

Food inflation is slowing down near a halt – after Hershey achieved significant growth from 2021 to 2023 aided by around a 6.4% CAGR in food inflation in the United States, food inflation has now slowed down into just 1.1% in July. The lower inflation looks to push Hershey’s growth back closer to the company’s historical rate, with 2024 food inflation so far even being below the long-term rate of 1.8% from 2004 to 2019.

More than just affecting top line growth, the lower food inflation could deteriorate margins as well. Labor costs are still growing at an elevated rate, as in June compensation costs for private industry workers increased 3.9% year-on-year – Hershey may not be able to push the still-growing costs to consumers with the lower food inflation, pushing profitability slightly down. In Q2, Hershey only raised its pricing 1% year-on-year.

3. Elevated Cocoa Prices

Also pushing down margins, cocoa futures and prices have skyrocketed in the past year after being nearly stagnant for a decade prior to the start of 2023.

Behind the increase, weather conditions in West Africa have recently been incredibly poor, contributing to an incredibly weak supply of Hershey’s most critical ingredient.

Cocoa Futures (Seeking Alpha)

While the futures have already fallen notably from the April high as weather conditions in West Africa are seen to start improving, cocoa prices remain at incredibly elevated levels. Manufacturers have had very lean cocoa stock management due to the price surge, leading to a near record-low stock-to-consumption ratio leaving demand for cocoa likely elevated for some time in the future as well. The demand will likely cause cocoa prices to remain elevated for some time.

As a result of higher cocoa prices and other factors, Hershey’s Q2 gross margin stood at 40.2%, down a dramatic 5.3 percentage points year-on-year. Commodity derivative losses and negative operating leverage from lower revenues also pressured the margin, but high cocoa prices were also communicated to have had a very clear adverse effect. Mondelez (MDLZ) reported an even higher 5.9 percentage point decline in Q2 with similar factors behind the decline. Tootsie Roll (TR) on the other hand managed to elevate the gross margin by 0.6 percentage points, seemingly as cocoa isn’t as critical for the company as for Hershey.

The cocoa price issue should subside at some point for Hershey, potentially through higher industry pricing as well. Yet, prices remain elevated for the time being, being a risk for the company and pressuring margins. In Q2, confectionery pricing was only pushed up 1% in line with overall food inflation in the US.

4. Lower Discretionary Spending

Hershey also related a part of the Q2 weakness to weak discretionary spending – the US consumer sentiment remains at a less-than-optimal level, which has been communicated to have the industry’s demand as well.

I don’t think that lower discretionary spending is a very large factor in Hershey’s Q2 decline as the industry is incredibly defensive – Hershey’s stable performance during the 2008-2009 great financial crisis also shows the company’s incredible resilience during turbulent macroeconomic trends. The rising recession worries could still pile onto Hershey, but I don’t think that weaker discretionary spending’s impact on Q2 has been large, and likely won’t be even in a clearly recessionary period.

Hershey Is Positioned Well Against the Headwinds

The headwinds don’t in my opinion pose a threat for Hershey over the long term despite potentially causing some further short-term hiccups after Q2 as well – Hershey’s high margin level makes earnings more resilient to changes in cocoa prices or other cost inflation, and the recession-resistant industry doesn’t look likely to be disturbed by changes in discretionary spending. With the ERP implementation, Hershey’s operations should be further streamlined to resist against industry challenges.

Hershey’s interest-bearing debt of $5.3 billion also doesn’t seem like too large of a threat with the company’s stable earnings profile, although the debt does slightly leverage the headwinds’ effects on shareholders.

Still, growth looks to stabilize at a considerably lower level than in prior years due to slowing food inflation; Hershey’s growth wasn’t very great leading into the pandemic at a revenue CAGR of just 1.5% from 2014 to 2019. Hershey should achieve a better growth rate in the future through snack sales growth, but a fall back to very low growth is still possible. Lower price increases amid elevated labor inflation are also likely to have at least a small negative effect on margins in upcoming quarters.

Hershey’s Valuation Comes at a Fair Margin of Safety

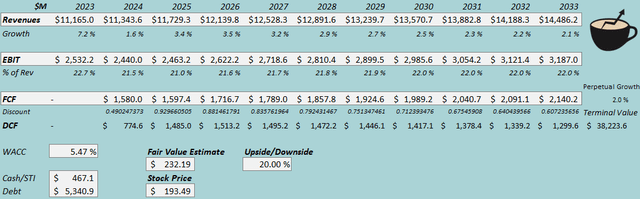

As usual, I constructed a discounted cash flow [DCF] model to estimate a fair value for the stock. In the model, I estimate slow 1.6% revenue growth in 2024 but a better overall CAGR of 2.6% from 2023 to 2033 and 2.0% perpetual growth afterwards amid low inflation and a stable volume growth outlook.

With commodity price pressures and the other headwinds including labor inflation, I estimate Hershey’s EBIT margin to fall to 21.5% in 2024 and further to 21.0% in 2025. With ERP implementation and the estimated growth, though, I estimate the EBIT margin to rebound into a 22.0% level slowly afterwards.

Hershey’s capital expenditures are quite elevated compared to D&A over the long term, and the company’s growth has historically required quite a hefty amount of capital through working capital increases. As such, I estimate the cash flow conversion to be at a fair level, but not at a significantly good one.

DCF Model (Author’s Calculation)

The estimates put Hershey’s fair value estimate at $232.19, 20% above the stock price at the time of writing – the stock’s headwinds seem to have created some undervaluation in the stock. I believe that a small margin of safety in the valuation is still fair as headwinds have piled onto Hershey.

Hershey’s 14.8 forward EV/EBITDA is at a very similar level to Mondelez’s 15.1 and Tootsie Roll’s trailing 14.4 EV/EBITDA, indicating a fair valuation.

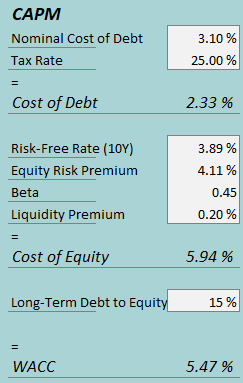

CAPM

A weighted average cost of capital of 5.47% is used in the DCF model. The used WACC is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

In Q2, Hershey had $41.4 million in interest expenses, making the company’s interest rate a low 3.10% with the current amount of interest-bearing debt. I estimate a similar amount of debt in financing to continue with a long-term debt-to-equity ratio of 15%.

To estimate the cost of equity, I use the 10-year bond yield of 3.89% as the risk-free rate. The equity risk premium of 4.11% is Professor Aswath Damodaran’s estimate for the US, updated in July. Yahoo Finance estimates Hershey’s beta at 0.35, but I add a 0.10 margin of safety to the estimate into a 0.45 beta estimate, more in line with competitor Mondelez’s 0.54 beta. With a liquidity premium of 0.2%, the cost of equity stands at 5.94% and the WACC at 5.47%.

Takeaway

Hershey’s stable long-term history was disturbed in Q2. The company is now facing headwinds from a cocoa price surge, lower consumer spending, low food inflation but higher labor inflation, as well as the adverse Q2 effects from ERP implementation and retailers’ inventory management. Hershey’s high margins and good brand portfolio are still positioned to ride through the headwinds well, although the lowering inflation does pressure Hershey’s growth back into a significantly lower level and could have an adverse effect on margins.

The stock’s valuation is comparable to industry peers and comes with a reasonable margin of safety. As such, I initiate The Hershey Company at a Hold rating.

Read the full article here