Helios Towers (OTCPK:HTWSF) is a telecommunication tower company focused on African and Middle-East regions. The business model of the tower companies is rather simple. Purchase a portfolio of towers, operate them efficiently and add more tenants on the towers, which elevates return on invested capital.

While the stock has been sliding downwards along with the other tower companies, the business performance of Helios is developing in the right direction. Although the company has taken on more debt, it was used to establish a stronger platform in the Middle East region.

In different timeframes, the potential catalysts for share price appreciation are deleveraging and continued growth, initiation of shareholder returns and being a potential acquisition target.

Solid track record of growth

Helios Towers was established in 2009 and the company is a composition of various acquisitions of tower portfolios from different mobile network operators (MNO) in Africa. Helios has been listed on the London Stock Exchange since 2019. At the time of the IPO, Helios had 6880 towers and 14 100 tenancies. Today, the company has 13 870 towers and 25 880 tenancies in nine countries. By 2026 the company aims to own 22 000 towers.

For a tower company, Africa offers multiple tailwinds. The growing population, increasing penetration of smartphones and upgrade of networks to newer generations should drive the investments to mobile networks in the long run. Most of the towers in Africa and Middle East are still owned by the MNOs, which provides an opportunity for Helios to grow inorganically.

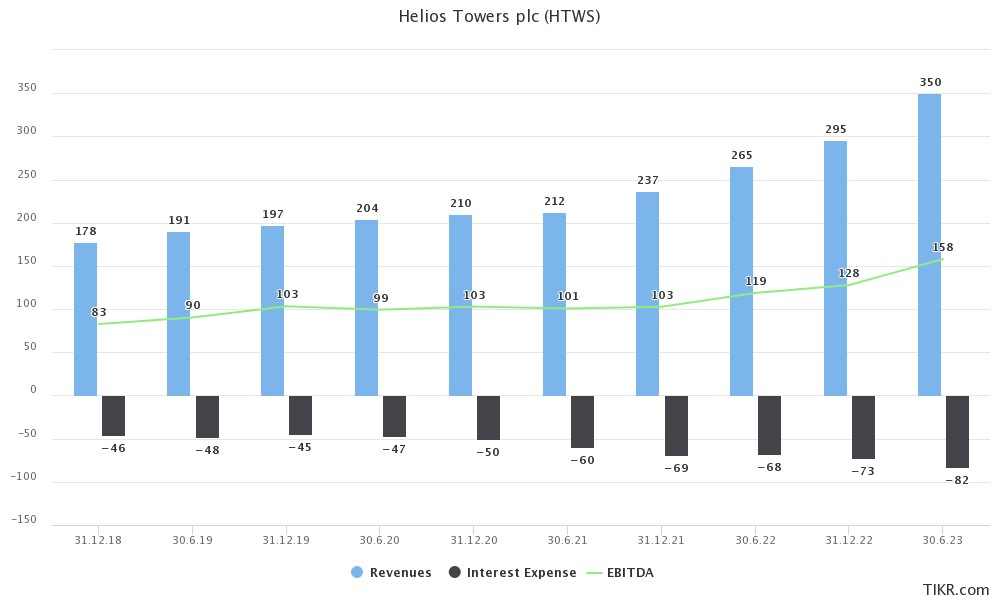

Revenue, EBITDA and interest expense development by half year. (Tikr)

Helios has a steady track record of revenue and EBITDA growth. As the business model has relied on inorganic growth by asset acquisitions, the debt and interest expenses have increased along with the growth. In the end of 2022 the company closed its most recent acquisition in Oman, 2500 towers for approximately $500 million and with an EV/EBITDA multiple of 12.4x.

Together with the acquisition and good underlying development of existing assets, showed excellent year-on-year growth at the end of Q2. Sequentially, the business went in the right direction with the best improvements in the bottom lines.

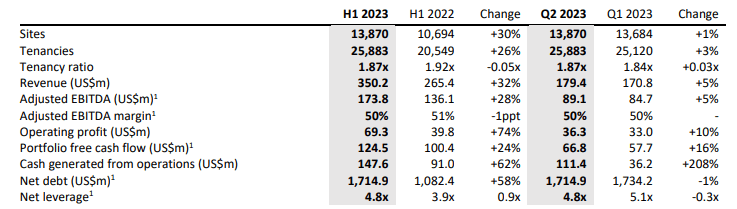

H2 financial performance. (H2 press release)

Potential catalysts to drive the shares higher

Deleveraging and continued growth

Due to the asset acquisition in Oman, the immediate growth potential of Helios is limited by its debt position and the current interest rate environment. Currently, Helios’ debt stands slightly above its target range of 3.5-4.5x. At the end of the H1 2023 its leverage ratio stood at 4.8x and quarter on quarter basis the leverage ratio was reduced by 0.3x.

Therefore, it is likely that for the next 2-4 quarters, the company focuses on deleveraging and improving financials of its newly acquired assets. Last year, Helios spent $765 million on capex and this year the company expects to spend $180-210 million. With an adjusted full year EBITDA of $355 million, up from $283 million in 2022, Helios has room for debt repayments. At the end of H2, the company had net debt of $1.7 billion (including capital leases). 83% of Helios’ debt is fixed rate and has four years average remaining life.

At the time of purchase the tenancy ratio, i.e. the number of tenants per tower, of the acquired portfolio in Oman was low 1.2. Now, the company needs to sell tenancies to the two other MNOs in the country, Ooredoo Oman and Vodafone Oman. Promisingly, the tenancy ratio already ticked 0.1 higher during H1 in Oman.

Helios is also in the process of developing the rather newly acquired portfolios in Senegal, Madagascar and Malawi, which have in total 2718 towers. Increasing the tenancy ratio of these towers provides Helios an opportunity to grow organically and elevate ROIC.

A hint about shareholder returns

Currently, Helios doesn’t pay a dividend nor do share repurchases. However, in the latest Q2 2023 earnings call the management was flirting with potential shareholder returns in the short or medium term.

So as long as we continue to de-lever getting within our desired range preferably towards the middle of that at least then we would actually start to look at some kind of shareholder disbursements if not a little bit sooner. -Manjit Dhillon, CFO

As the tower companies in the U.S. are in the favor of income investors, a dividend would surely draw more attention to the stock. Meaningful share repurchases could be difficult to conduct due to the limited free float and low trading volumes.

Certainly becoming a dividend payer is where we want to get to. And on this trend we got there reasonably soon in the more short to medium term. -Tom Greenwood, CEO

The statements by the management are fairly puzzling. The company has an ambitious growth vision and high debt load, so distributions to shareholders appear an odd plan. The management certainly has the confidence to simultaneously reduce the debt and distribute capital, however

We’ll be able to — in our opinion we’ll be able to do both potential paydowns, but also look at actually distributing capital to shareholders. We should be able to do a bit of both in short. But again it all comes down to the decision point at the time. It also comes down to what opportunities are available for the company in terms of organic and M&A growth as well. -Manjit Dhillon, CFO

Potential acquisition target

The largest owners of Helios are primarily private equity or asset management firms focused on emerging markets. Four out of the five largest owners have been involved with the company since it was founded or its listing. That could be one of the reasons for the urge to shareholder distributions. Five of the largest shareholders are:

-

Newlight Partners has nearly 15% ownership in Helios Towers.

-

Helios Investment Partners owns 7.5% of the shares

-

IFC Asset Management Company, a member of the World Bank Group, owns 7.4% (8.4%) of the shares .

-

J. Rothschild Capital Management Limited, a listed investment vehicle of Rotschild family, holds 5% of the shares.

-

Rivulet Capital 4.5%

All of the owners appear patient investors. However, sooner or later they would like to see returns on their investment either in the form of value appreciation or shareholder returns. There’s a lot of available funds and dry-powder among private equity. With a market cap of less than 1.2 billion dollars is a small target for the largest PE firms, such as Brookfield, which have been acquiring much larger tower portfolios with EV/EBITDA valuations above 20x.

Downside considerations

In the western hemisphere, the MNOs have been reducing their capital expenditures. This trend has worked against the tower companies, which need to rent space on their towers for new communication equipment. In the markets where Helios operates, the mobile network operator business is growing as population grows, data usage increases and MNOs upgrade their networks still from 2G and 3G, which still have a share of 70-80%, to more advanced technology.

Rising interest rates, currency depreciation in the different markets and pressure on multiples are key risks to the investment thesis. There are some mitigations. 64% of the company’s revenues are denominated in USD or Euro. Helios is more often than not able to pass on inflationary pressures to its customers with a time lag. This reduces the relative profitability as costs are simply invoiced through.

Upside potential is existing if market continues to value EBITDA

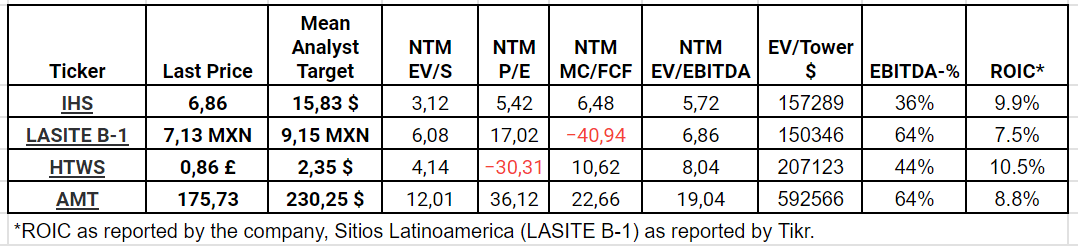

Helios Towers is not the cheapest tower company focused on emerging markets. IHS Towers, which I have covered multiple times, is still one of the most interesting opportunities in the sector. However, Helios is less exposed to an individual country (Tanzania has 30% of the towers), its markets have suffered less from currency depreciation and it has better operational efficiency.

Multiples of Helios and its peers and two selected performance measures. (Tikr, company materials)

The thesis regarding the valuation is rather simple. The company continues to grow EBITDA by price increases, adding new tenants on existing towers, building new towers and occasional portfolio acquisitions. Historically, Helios has grown its EBITDA by over 10% annually. The average EV/EBITDA multiple since the listing of Helios Towers has been 9.5x.

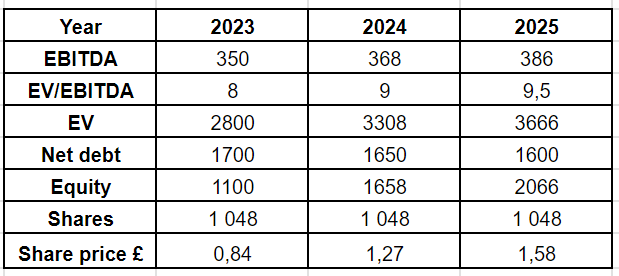

If we rather conservatively assume that the EBITDA grows by 5% per year, the company reduces its debt (excluding capital leases) by only $50 million per year and the EV/EBITDA multiple returns to its historical average, the shares could have a price tag of almost £1.58 in three years. Nearly a double. If the multiple would remain at current levels, the share price would stand at £1.14, still significantly above current price of £0.87 at the time of writing. Eight analysts have given Helios an average target price of £2.35.

Valuation scenario. All the figures in USD, except the share price. (Author)

Conclusion

Helios Towers is another tower company to tap into the growth of the digital infrastructure in emerging markets with built-in mitigations against currency depreciation and inflation. The company has a good track record of growth, further potential, and it has given hints about moving to a next phase of shareholder value creation. The shares appear attractively valued historically, relatively, and based on the current outlook for the company.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here