I’ve always been a fan of REITs. Looking for a nice return on investment is simpler when one has a reasonable knowledge of what the dividends are going to look like. Obviously, residential REITs, and the high-yield mortgage residential REITs, are the most common of this form. But sometimes we want to diversify into other forms of REITs.

Office REITs are one such possibility. Today, we’ll be looking at Highwoods Properties (NYSE:HIW), an office REIT with properties around the southern US. The focus will be on understanding the business they’re in, what’s being offered in the realm of return, and the risks associated with this office REIT.

Understanding Highwoods Properties

Highwoods Properties owns and leases properties in the cities of Atlanta, Charlotte, Dallas, Nashville, Orlando, Raleigh, Richmond and Tampa. In 2023 the company moved out of the Greensboro and Memphis markets, and added the faster growing markets of Charlotte and Dallas.

The strategy is to own and operate high-quality workplaces in the most valuable business district parts of town. According to the 10-K they have acquired since 2019 what they described as 4.0 million square feet of ‘trophy’ office assets at an investment of $1.9 billion. That’s not a bad price for growth.

Looking at Highwoods Properties’ Balance Sheet

|

Cash and Equivalents |

$16.4 million |

|

Buildings |

$5.9 billion |

|

Total Assets |

$6.0 billion |

|

Mortgages and notes payable |

$3.3 billion |

|

Total Liabilities |

$3.5 billion |

|

Total Shareholder Equity |

$2.4 billion |

(source: most recent 10-Q from SEC)

The nice thing about Highwoods Properties is it’s easy to understand balance sheet. The total assets are made up almost entirely of buildings owned, and the total liabilities are overwhelmingly from mortgages. It’s a very simple lineup.

At current levels the price/book value comes in at a sensible 1.14. That’s not the sort of discount one would’ve been able to realize if they were buying in the fourth quarter of 2023, but it’s still not a gaudy premium to be afraid of, particularly for a company that offers value levels of earnings and pays a nice dividend return.

The Risks

Like most companies, Highwoods Properties is dependent on economic conditions in the markets in which they operate. A bad economy could lead to lower occupancy and rental rates, and that could reduce margins. That’s likely why they’re picking and choosing strong markets.

The downside to these strong markets is that there is considerable competition to contend with. That’s going to be a constant issue limiting their ability to increase prices.

The real question though is the trend toward work-from-home. With the rise of the pandemic in 2019-2020, companies tried to protect their workers through a system of no-contract. That’s less of an issue today, but some workers decided they preferred working from home, and some companies decided that was just fine.

Some leases allow the customer to terminate early. If the offices are too big, or in some cases no longer necessary, they can get out of these, and that could be a drag on revenues.

That’s not to say that people working from home mark a serious threat to the traditional office, but if companies have a meaningful percentage of their employees working from home, they’ll need less space overall, and that could lead to customers choosing to downsize what their leasing form the company.

Looking at the Earnings

|

2021 |

2022 |

2023 |

2024 Q1 |

|

|

Rental Revenue |

$768 million |

$829 million |

$834 million |

$211 million |

|

Op. Expenses |

$536 million |

$626 million |

$611 million |

$156 million |

|

Net Income |

$323 million |

$164 million |

$151 million |

$27 million |

|

Diluted EPS |

$2.98 |

$1.49 |

$1.39 |

25¢ |

(source: 10-K from SEC)

Rental revenue has been slowly but steadily increasing, and estimates for 2024 and 2025 show that this should continue, with the estimates $837 million and $841 million, respectively. Everything is definitely heading in the right direction.

More encouraging is that while net income went down the last couple of years (and by extension, diluted EPS), the estimates predict a strong recovery at hand, with $3.56 for 2024 and $3.54 for 2025, both very nice for a company trading at these levels.

The P/E ratio for the 2023 earnings would be 18.68 at present prices. That’s not exactly value range, but if we look for the forward P/E, we find it at 7.29, a very nice value proposition.

I can’t say enough what a good sign that is. The more common REITs we often see, the residential REITs, tend to have very shaky earnings, though it usually comes with higher dividend yields.

A Strong Dividend Yield

Since 2020, Highwoods Properties has been slowly increasing its already strong dividend. In 2020 the dividend increased to 48 cents per quarter. In the second half of 2021 the dividend increased to 50 cents per quarter, where it remains to this day.

That puts the dividend yield to 7.53%. That is a strong rate of return, though naturally if we went back to mortgage REITs it would be easy to find double digit returns as a matter of course.

If we continue to see earnings per share in the $3.56 range, which the estimates suggest we will, this will allow Highwoods Properties to strongly consider raising the dividend going forward. That would be extremely good news.

Conclusion

Highwoods Properties is a strong earner. Any company that offers a forward P/E ratio in the 7.29 and a dividend yield of 7.5% is the sort of company I would be looking for. I consider this a buy.

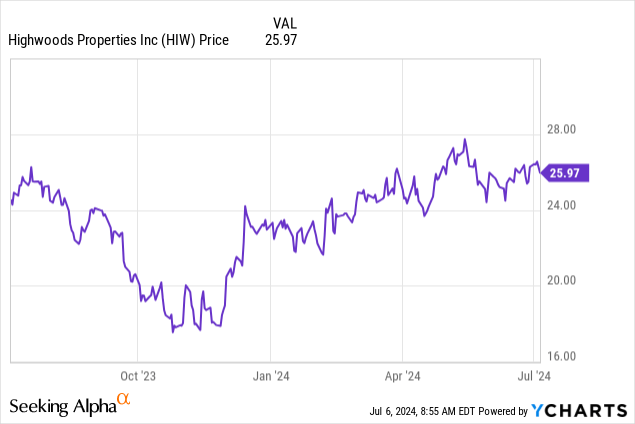

That said, the price is getting awfully close to the 52-week high, and there were better opportunities to buy the company back last year. If you’re buying, this would be a good candidate for buying for the long-term, and maybe even looking for a better entry point.

If you have an income portfolio, REITs are always something that should be on your watchlist. It shouldn’t be all residential REITs, however, even though those are mostly the highest yield. Getting into the office space, particularly in appealing markets like Highwoods Properties is, offers a nice balance of yield and diversity.

Read the full article here