M&T Bank In New York City

Opportunities Following Silicon Valley Bank

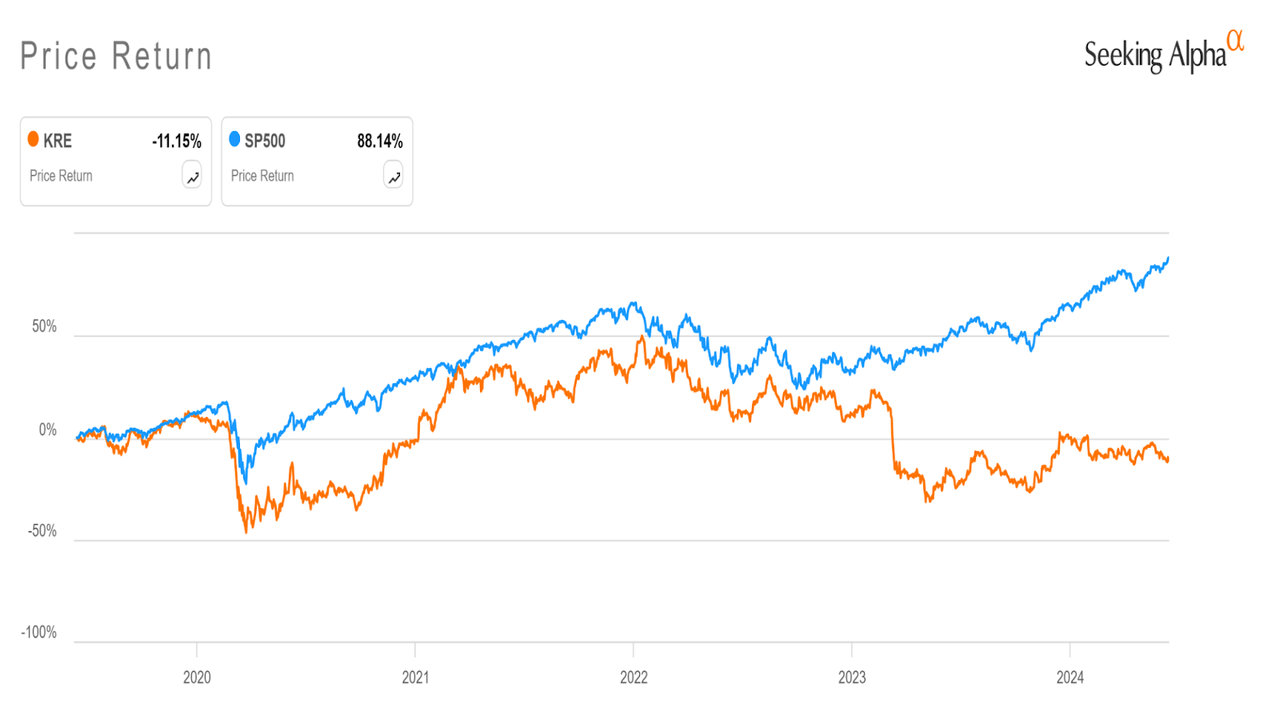

The recent turmoil surrounding the failure and seizure of banks such as Silicon Valley Bank and First Republic has raised concerns about the stability of the regional banking sector across the country. This has led to increased regulations and higher volatility. Many regional banks have been considered “guilty by association” and are undervalued due to credit fears and broader economic uncertainties. The US regional bank sector has yet to recover from this setback fully and could provide a valuable investing opportunity. To test our hypothesis, the Regional Banking ETF (KRE) was chosen as a benchmark for the performance of US regional banks.

KRE trades at 6.44x earnings and a P/B ratio of 0.8, significantly lower than its 10-year medians of 12.4 and 1.3, respectively.

When comparing the price return of the KRE index to the S&P 500, we can see that both were correlated through 2023, but the price return divergence occurred following the fallout of SVB in the first quarter of 2023. Regional banks have historically adapted to perform in rising and falling interest rate environments. Despite its recent volatility, the sector is undervalued, fueled by better-than-expected market conditions (or a “soft landing”) and low unemployment.

Performance of KRE and S&P500 from Seeking Alpha

Why M&T Bank?

To ensure a representative sample size, 149 unique regional banks were selected from the two most prominent US regional bank ETFs: iShares U.S. Regional Banks ETF (IAT) and SPDR S&P Regional Banking ETF. The sample size was narrowed to US regional banks with market capitalizations ranging from 10 to 100 billion dollars.

We identified the ten most pertinent metrics for assessing regional bank health and stability. These metrics include net interest margin, loan-to-deposit ratio, return on assets (ROA), return on equity (ROE), efficiency ratio, non-performing loans, Tier 1 capital ratio, price-to-book ratio, forward price/earnings to growth (PEG) ratio, and total deposits per share.

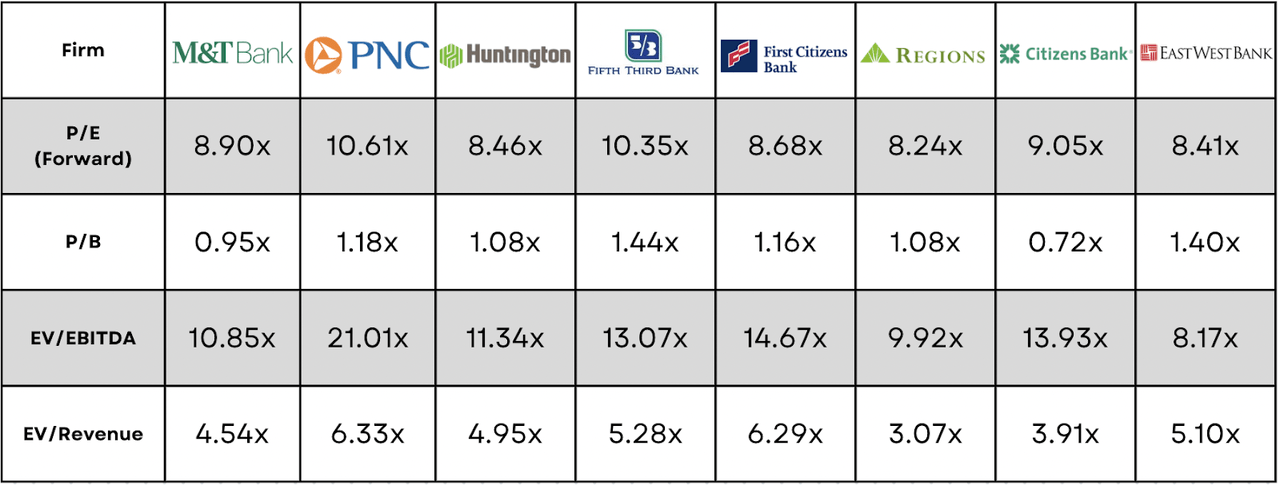

We assigned weights to these ratios based on their perceived importance, and ranked all U.S. regional banks. Based on this methodology, M&T Bank emerged as a top performer. Our methodology is further supported by the KRE ETF, where M&T Bank represents the highest percentage weight at 2.65%, taken as of Friday, June 21st.

While these ratios provide valuable insights, macroeconomic conditions, regulatory capital requirements, and management are additional factors that led us to pick M&T Bank.

Competitor Ratios from Yahoo Finance

About M&T Bank

For over a century and a half, M&T Bank (NYSE:MTB) has been a trusted financial institution in the Mid-Atlantic and Northeastern parts of America, solidifying its position as one of the largest regional banks in America. In 2022, M&T Bank operated around 700 branches, which increased to approximately 1,000, excluding ATMs, after the acquisition of People’s United Bank. Regarding operations, M&T Bank caters to various sectors, including automotive dealerships, healthcare, and agriculture. With its long-standing history, M&T has built a loyal customer base and a sharp understanding of local market needs.

M&T Bank maintains a high net interest margin relative to its competitors. However, this advantage is offset by increased provisions for credit losses and higher default rates from CRE loans. As the bank implements new lending strategies to mitigate these expenses, our intern team is adopting a wait-and-see stance despite the potential upside. This article delves into why additional time is necessary to assess M&T’s future performance as the regional banking sector slowly recovers.

M&T Deposits & Loan Portfolio

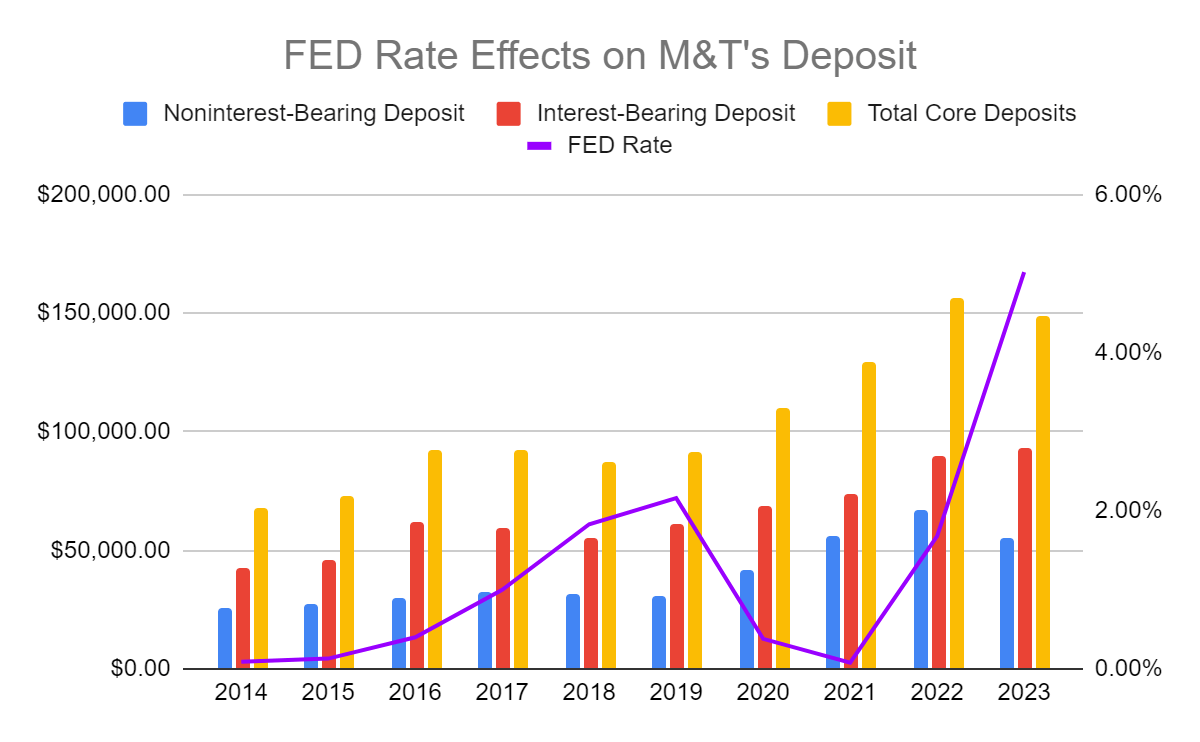

Banks primarily generate revenue from the difference between interest expenses paid on deposited accounts and income earned from lending activities, known as net interest income. In our competitor evaluation, M&T ranked second regarding net interest margins at 4.39%. To project M&T Bank’s future performance, we delved into its deposit and loan portfolio over the last ten years.

Despite fluctuating federal funds rates, M&T Bank has consistently seen growth in deposited accounts. Although higher rates have led some customers to transfer funds from non-interest-bearing accounts to treasury bonds, the overall increase in deposits has reduced M&T’s net interest income. This is due to the higher interest rates the bank must pay on these deposits. We will delve into the effects of this on their income statement in the next section.

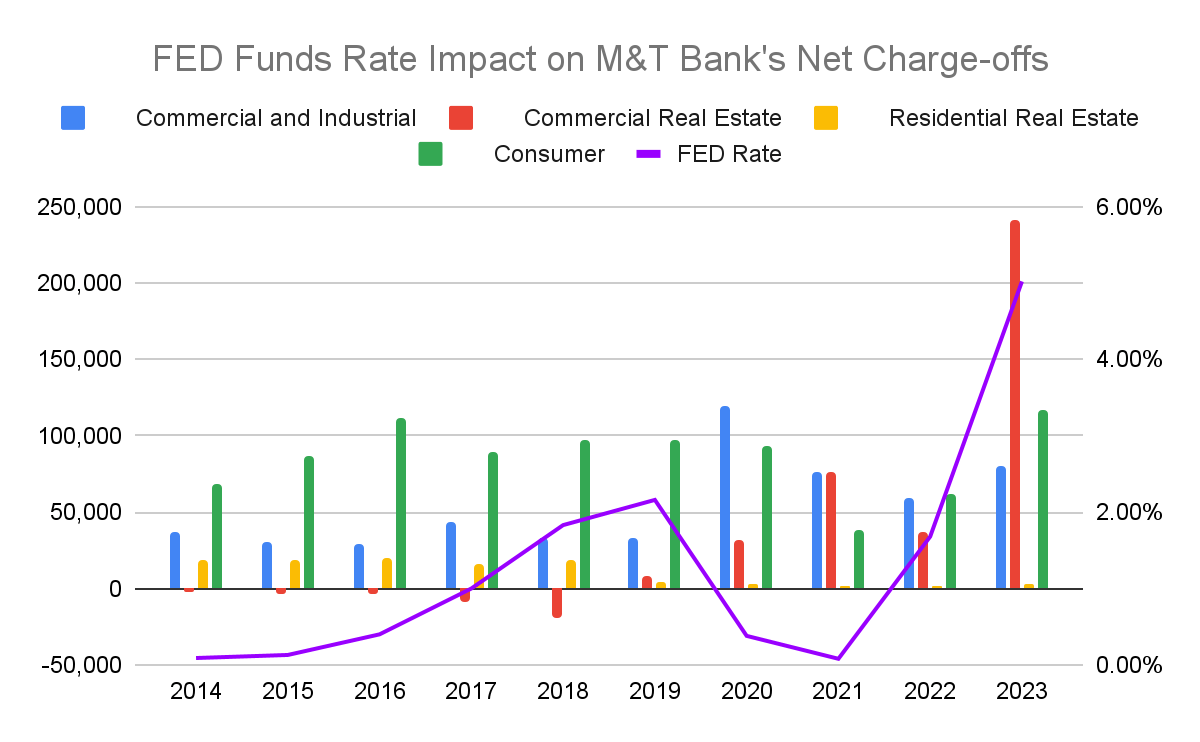

Euphoric Investment, M&T Bank 10K 2014-2023, FRED

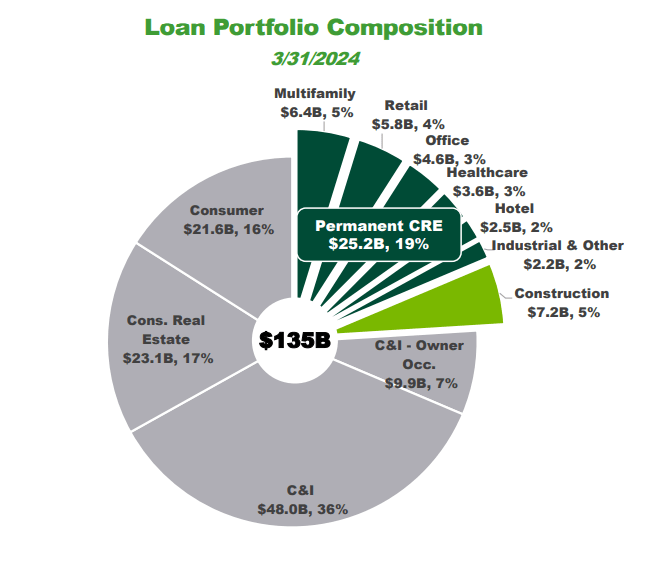

Within M&T Bank’s loan portfolio, commercial and industrial (C&I) loans account for 43%, while commercial real estate (CRE) loans make up 19%. These proportions increased following their 2022 acquisition, where People’s United had a loan portfolio consisting of 32% CRE and 23% C&I. Given M&T’s strategy to expand in the CRE and C&I space through their largest acquisition ever, we analyzed the resilience of these loan types in different federal funds rate to project their future returns.

Loan Portfolio Breakdown from Q2 2024 MTB Presentation to Investors

In environments with higher interest rates, defaulted loan rates tend to rise, leading to increased net charge-off ratios. Our research indicates a linear correlation between the federal funds rate and net charge-off ratios for C&I and CRE loans. However, there exists a lag as variable-rate loans gradually adjust to changes in the federal funds rate. Our intern team anticipates that interest rate cuts are unlikely due to low unemployment rates and strong consumer spending. With this in mind, we expect net charge-off ratios to remain elevated across all loan categories for M&T Bank, further reducing our net interest income as we account for expenses paid to provision for credit losses.

However, M&T’s focus on C&I loans has been a wise choice, as C&I loans maintained stable net charge-off ratios consistently. In contrast, there was a notable increase in net charge-offs for CRE lending in 2023. Further investigation revealed that this rise was driven by declining demand for office spaces and higher LIBOR rates, which increased borrowing costs and led to more defaults. Looking forward, our team anticipates that the continued unpredictability in the real estate sector will keep charge-off ratios high. This calls for patience as we await stabilization in the real estate sector and the return of net charge-offs to previous levels. Further details on the effects of higher rates of defaulted loans will follow in the next section.

Euphoric Investment, M&T Bank 10K 2014-2023, FRED

Effects on Income Statement

In comparing the Q1 2024 income statement to Q1 2023, increased net charge-offs in commercial real estate (CRE) and higher customer deposits have significantly impacted our net income. Interest expenses paid on savings and interest-checking deposits rose by $338 million, while provisions for credit losses increased by $80 million. After accounting for provisions, this resulted in a decrease of $218 million in net interest income. Diluted earnings per share declined from $4.03 in Q1 2023 to $3.04 in Q1 2024. Since net charge-offs have doubled since Q1 2023 and customer deposits continue to rise, these factors are expected to influence our net income.

Despite these impacts, M&T Bank still ranks second among competitors in net interest margin, indicating efficient revenue-to-net income operations. However, expenses related to credit losses have reduced this advantage. M&T has responded swiftly by reducing CRE lending by $2.5 billion and increasing C&I lending by $4 billion over the past year. However, the full impact of these changes on M&T’s income statement and the stabilization of the real estate market will require further observation over time.

Uncertain Future of the Regional Banking Sector

The regional banking sector is still recovering from Silicon Valley Bank’s collapse, which has led to increased market volatility, stricter regulations, and overall consumer distrust of regional banks. The sector’s vulnerability to macroeconomic influences and its track record of bank failures extend the timeline for restoring consumer confidence. As a result, it may take time to achieve stable returns, and the timing of this stability remains unclear.

Moreover, despite M&T Bank’s success under CEO Rene Jones, the absence of a COO since Q1 2023 is concerning, especially given their decision not to replace the role. While no immediate issues have surfaced, this approach could pose operational challenges in the future.

Post-Merger Difficulties

While acquiring People’s United Financial was successful, it presented challenges such as hundreds of layoffs and system conversion issues, which generated negative publicity and customer complaints. We believe these challenges will continue to affect M&T Bank’s ability to maintain customer satisfaction, retention, and a solid reputation.

Furthermore, People’s United Financial’s significant investment in commercial real estate (CRE) loans led to declining interest income and rising net charge-offs. Assuming People’s United’s debt made it harder for M&T to meet obligations while maintaining enough capital reserves. We see the volatility in the CRE market adding more uncertainty to when M&T will generate stable and growing returns needed to repay the debt.

Valuation

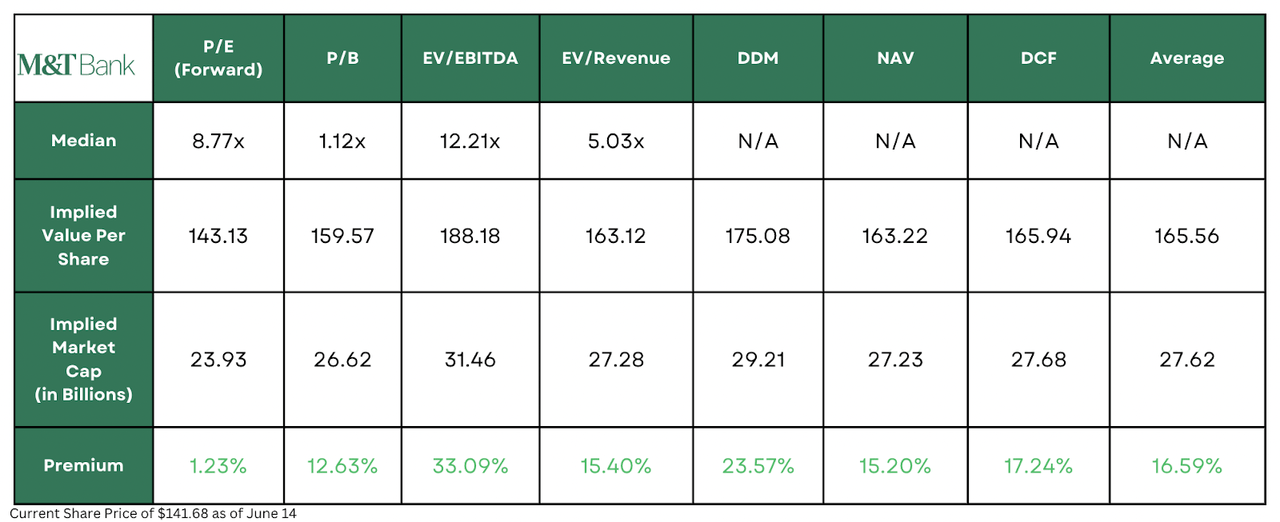

For our valuation of M&T Bank, we used four different valuation methods to obtain an intrinsic value of the company. This value was derived from four main valuation methods: comparative analysis, dividend discount model (DDM), discounted cash flow (DCF), and net asset value (NAV). Different valuation methods are used to capture the bank’s business model and the industry in which it operates. These valuations will most accurately represent the targeted share price within one year. An equal weighting was applied to all the valuation methods to capture the strengths of each model and avoid any potential bias of any single method.

Euphoric Investment Valuation for M&T Bank

In the upcoming twelve months, M&T Bank shows a potential upside of 16.59%, aiming for a price target of $165.56. However, the potential premium of 16.59% cannot justify a “buy” with the added risk of loan defaults from macroeconomic instability. Therefore, we recommend closely following the US regional banking sector with a “hold’ on M&T Bank.

Final Thoughts

Given the current economic conditions, M&T Bank Corporation presents a complex investment case. The bank has shown promising signs of resilience and strategic growth through its focus on C&I expansion and acquisitions like People’s United Financial. However, the lingering effects of the Silicon Valley Bank collapse still cast a shadow over the regional banking sector, impacting market volatility and consumer trust. M&T’s heavy exposure to volatile commercial real estate loans and the increasing net charge-offs also present another element of risk.

Despite M&T Bank’s efforts to reduce its commercial real estate (CRE) loans and expand commercial and industrial (C&I) lending, the impact on future net interest income remains uncertain. We believe further observation is needed. As we await the recovery of the regional banking sector, M&T is a company that investors should closely monitor.

Given these factors, we maintain a “hold” recommendation on M&T Bank. While there is potential for upside, with our valuation methods suggesting a 12-month price target of $165.56 (a 16.59% premium), the current risks surrounding the real estate market and macroeconomic uncertainties do not justify a “buy” rating. Investors should keep an eye out on sector performance, M&T’s credit losses, improvement in the real estate market, and potential federal funds rate changes before considering a more bullish stance.

Read the full article here