Looking for high-yield tech and/or life science investments? While these two sectors aren’t known for attractive dividend yields, there are still ways you can earn high-yield income from them.

One way is to invest in certain business development companies to gain high-yielding exposure to privately held tech and life science companies. Horizon Technology Finance (NASDAQ:HRZN) is a BDC with a focus on these two sectors.

Company Profile:

Horizon Technology Finance Corp. is managed by its advisor Horizon Technology Finance Management LLC. Horizon is a leading venture lending platform that provides structured debt products to life science and technology companies. Since 2004, Horizon has directly originated and invested more than $3 billion in venture loans to more than 315 growing companies. It is based in Farmington, Connecticut. (HRZN site)

Holdings:

HRZN’s biggest investment exposure, 63%, is with companies in the expansion stage, followed by early-stage companies, at 32%, and later-stage firms, at 5%. Its portfolio had warrant and equity positions in 97 companies as of June 30, 2023, with a value of ~$715M, as of 6/30/23.

Its two main sectors are Life Sciences, at 43%, and Tech, at 40%. And 12% of its portfolio is invested in Sustainability companies, with 5% invested in Healthcare Information Services.

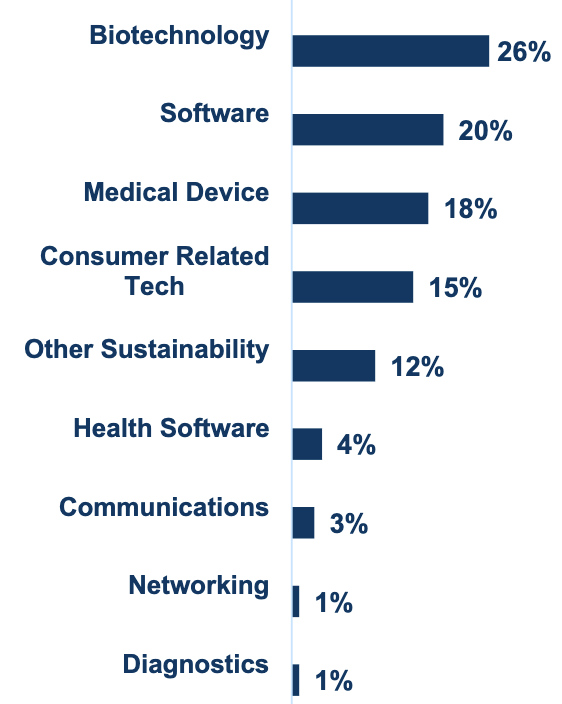

Sub-sector exposures run from Biotech, at 26%, down to Networking and Diagnostics, both at 1%:

HRZN site

Portfolio Company Ratings:

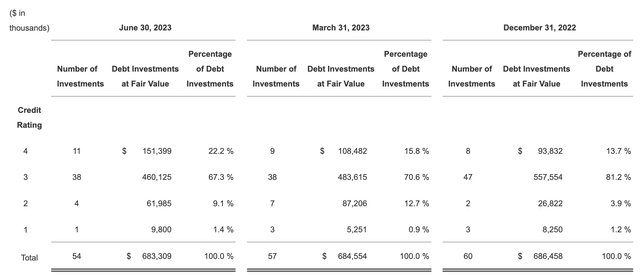

As with other BDCs, HRZN’s management rates its debt portfolio companies quarterly. Four is the highest tier – one is the lowest. As of 6/30/23, its debt portfolio consisted of 54 secured loans with an aggregate fair value of $683.3M. Top tiers 1 and 2 had 49 of the 54 companies, for 89.5% of fair value of the portfolio, vs. 55 companies at the end of 2022, at ~95% of fair value.

As of June 30, 2023, there was one debt investment with an internal credit rating of 1, with an aggregate cost of $17.4M and an aggregate fair value of $9.8M, vs. three debt investments with a cost of $20.9M and a fair value of $8.3M, as of Dec. 31, 2022.

HRZN site

Earnings:

Like other BDCs, HRZN has been reaping the benefits of rising rates and the pullback of banks from commercial loans.

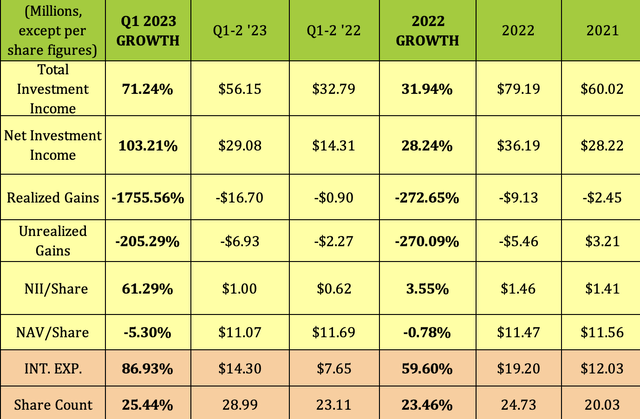

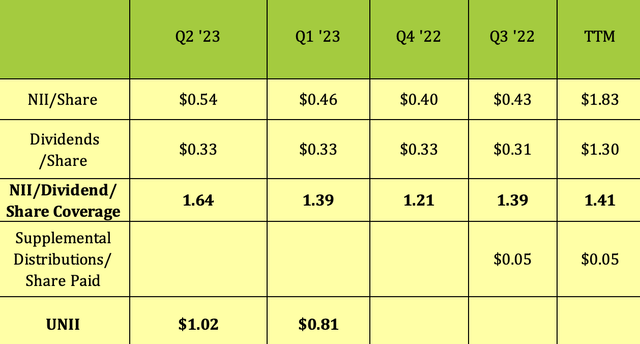

Q2 ’23: NII/share rose 54%, to $0.54, vs. $0.35/share in Q2 ’22. Total investment income for the quarter grew 51.3% to $28.1M, vs. $18.6M in Q2 ’22.

The annualized portfolio yield on debt investments was 16.3%, vs. 14.2% a year ago. HRZN funded 11 loans totaling $49.6M in Q2 ’23.

Sequentially, NAV declined from $11.34 as of 3/31/23, to $11.07 at 6/30/23. Management wrote off three debt investments as well as marked down the fair value of other debt investments contributing to the $0.27/share reduction in NAV for the quarter.

Q1-2 ’23: Total Investment Income jumped 71% due to a larger portfolio, and higher interest income. NII rose 10%, while NII/Share rose 61%, due to a higher share count.

The share count rose 25% – HRZN raised $38.9M of net proceeds in a common stock offering, and ~$5.1M with its “at-the-market” (“ATM”) offering program in Q2.

Interest expense rose $6.7M, up 87%, but was outpaced by the $15M jump in NII.

Hidden Dividend Stocks Plus

New Business:

HRZN funded 11 debt investments totaling $50M in Q2 ’23, including a $10M debt investment to a new tech portfolio company focused on security imaging, and a $10M debt investment to a new healthcare information portfolio company, providing AI-enabled technology for dementia care.

HRZN received two loan prepayments, one refinanced loan and one partial paydown during the quarter totaling $30M. HRZN ended the quarter with a committed and approved backlog of $159M, vs. $187M at the end of the first quarter.

Dividends:

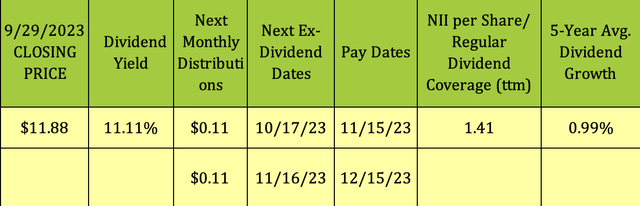

At its 9/29/03 $11.88 closing price, HRZN yielded 11.11%. Management already declared dividends for October and November, maintaining the $.11/share payout that it has paid since December 2022. HRZN has had modest dividend growth of 0.99% over the last five years, maintaining its monthly payout at $.10 from 2017 to late 2022.

Hidden Dividend Stocks Plus

In Q2 ’23, HRZN’s dividend coverage was even stronger than in recent quarters, rising from 1.39X to 1.64X, with a trailing average of 1.41X, one of the higher coverage rates we’ve seen in the BDC industry. It ended Q2 ’23 with $1.02/share in UNII, up from $.82 in Q1 ’23.

Hidden Dividend Stocks Plus

Profitability and Leverage:

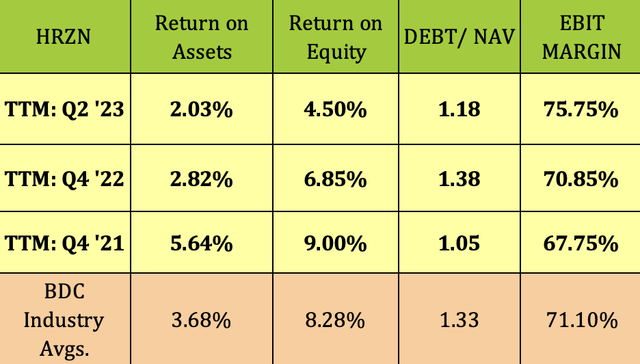

The realized and unrealized losses in Q1-2 ’23 decreased ROA and ROE, which are below BDC industry averages, whereas the EBIT Margin rose to ~76%, above average. Debt/NAV leverage decreased to 1.18X, more conservative than the 1.33X industry average.

Hidden Dividend Stocks Plus

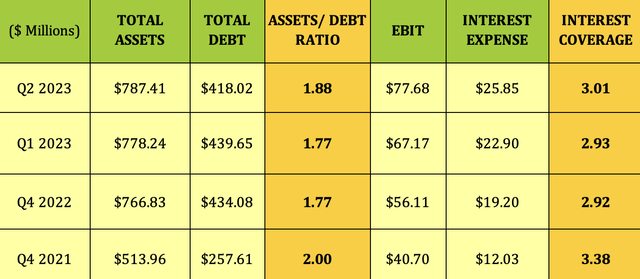

HRZN’s Assets/Debt and EBIT/Interest coverage ratios both improved in Q2 ’23:

Hidden Dividend Stocks Plus

Debt and Liquidity:

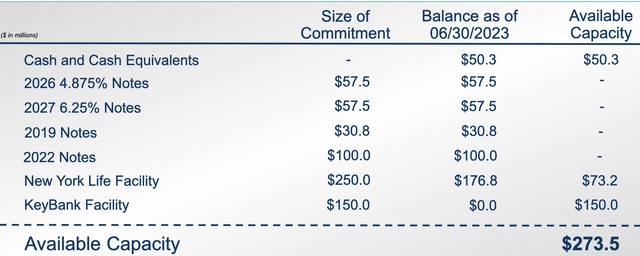

As of June 30, 2023, there was no outstanding principal balance under its revolving credit facility with KeyBank. On June 29, 2023, the Company amended the Key Facility, among other things, to increase the commitment amount to $150M, and to increase the amount of the accordion feature, which now allows for the potential increase in the total commitment amount to $300M.

On May 24, 2023, the company amended the NY Life facility, to increase the commitment by $50M.

As of June 30, 2023, the company had $273.5M in available liquidity, consisting of $50.3 million in cash and money market funds, and $223.2M in funds available under existing credit facility commitments.

HRZN site

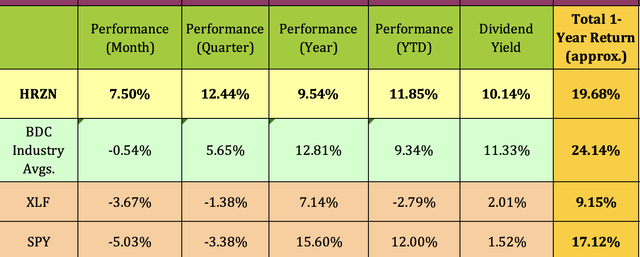

Performance:

HRZN has outperformed the BDC industry and the S&P 500 over the past month, and quarter, and has outperformed its industry so far in 2023 on a price basis. It has outperformed the financial sector over all of the periods below while achieving a higher total return than the S&P over the past year.

Hidden Dividend Stocks Plus

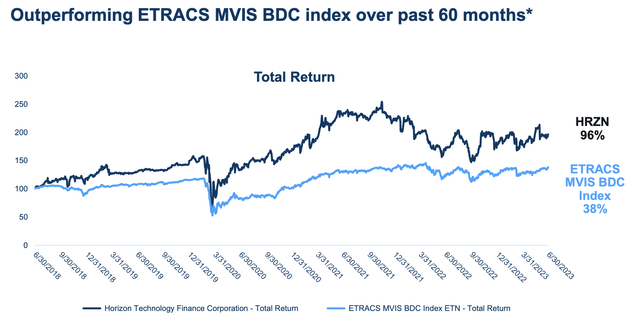

HRZN has delivered a 96% return over the past five years vs. 38% for its benchmark index.

HRZN site

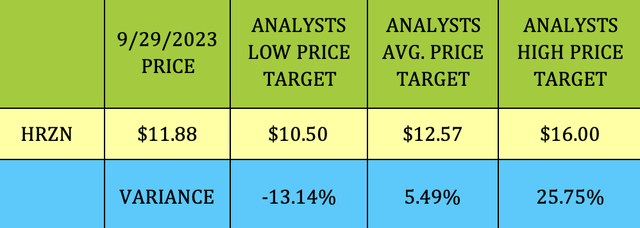

Analysts’ Price Targets:

At $11.88, HRZN is 13% above analysts’ lowest price target of $10.50, and 5.5% above the average $12.57 price target.

HRZN received a downgrade from Compass Point on 9/27/23, moving to Sell from Neutral – they lowered their price target from $11.00 to $10.50.

Hidden Dividend Stocks Plus

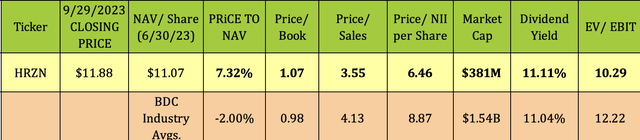

Valuations:

At its $11.88 9/29/23 closing price, HRZN was trading at a 7.3% premium to NAV, vs. an overall BDC industry Price/NAV discount of 2%. However, HRZN’s earnings multiple, a Price/NII of 6.46X, is much lower than the BDC average of 8.87X. Its P/Sales and EV/EBIT valuations are also lower than average.

Hidden Dividend Stocks Plus

Parting Thoughts:

HRZN’s advisor was acquired by Monroe Capital, as of 6/30/23, which management feels will be a boon to HRZN, enabling it to compete and win larger investment opportunities and help it create a more diverse portfolio. And 100% of the outstanding principal balance of its debt investments bear interest at floating rates, with rate floors.

We rate HRZN a speculative Buy, based on its floating rate exposure, its very well-covered yield, its low P/NII, and its long-dated debt maturities.

All tables are furnished by Hidden Dividend Stocks Plus, unless otherwise noted.

Read the full article here