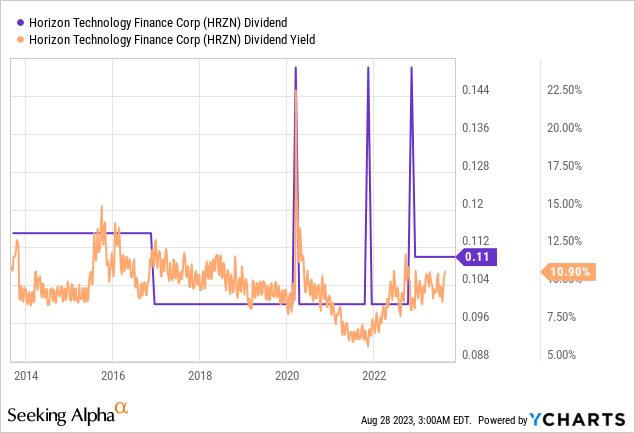

Venture debt is having its golden moment as private credit takes center stage on the back of the spring 2023 banking failures, subsequent incoming increases to US banking capital requirements, and a Fed funds rate that currently sits at a 22-year high at 5.25% to 5.50%. This subset of private credit describes loans offered to early-stage high-growth companies with venture capital backing. Non-bank lender Horizon Technology Finance (NASDAQ:HRZN) is up 9% on a total return basis year-to-date and is experiencing a surge in demand for new loans. This has come in tow with a floating rate portfolio positioning that is driving Horizon’s total and net investment income to new highs. The business development company last declared a monthly cash dividend of $0.11 per share, in line with its previous payout and for an 11.15% annualized forward yield.

Horizon Technology Finance Fiscal 2023 Second Quarter Presentation

Venture debt has become the preferred financing tool for startups seeking non-dilutive finance, a trend heightened by the March collapse of Silicon Valley Bank and what’s set to be tougher capital requirements from the upcoming Basel III endgame rules. Horizon’s portfolio at fair value as of the end of its recent fiscal 2023 second quarter stood at $715 million, up a huge 24% over its year-ago comp with the BDC also ending the quarter with $159 million in commitments. This came as the BDC’s dollar-weighted annualized yield on average debt investments grew to reach 16.3% during the second quarter, a 210 basis points expansion from its year-ago figure. Horizon’s lending is predominantly to life science companies which form 43% of its portfolio with the BDC most recently closing on a $15 million venture loan facility to Tallac Therapeutics, a Burlingame, California-based biopharmaceutical company developing a pipeline of immunotherapy candidates to fight cancer.

The Macroeconomic Backdrop And Loans On Non-Accrual Status

Financial Times

The yield on debt derived by the BDC is likely set for further gains on the back of the July rate hike. However, the market is currently pricing in a roughly 80% chance that the Fed will keep rates unchanged at its next FOMC meeting on the September 20. Critically, the Fed’s higher for longer mantra is set to entrench this golden era for BDCs for longer. However, there is a need for investors to be cautious here. UBS is predicting a spike in the default rate of private credit borrowers to as high as 9% to 10% next year on the back of the dramatic increase in the cost of credit.

Horizon had two investments on non-accrual status, with a fair value of $15.3 million, representing 2.14% of its total investment portfolio as of the end of the second quarter. This was up from the start of the fiscal year when investments on non-accrual status had a fair value of $8.3 million and was around 1.15% of Horizon’s $720 million total investment portfolio. The risk here is that higher for longer gets aggregated with a marked economic slowdown and that a hard landing of the US economy gets realized to spark intense credit risk. Horizon flagged that 100% of its outstanding principal on its debt investments bear interest at floating rates during its second-quarter earnings call, but we’re getting to an inflection point where any further hikes to the Fed funds rate could become detrimental to net asset value if it drives an increase in defaults.

Net Asset Value And The Dividends

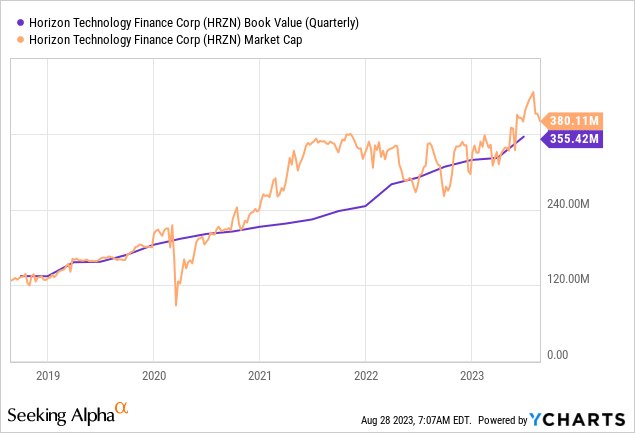

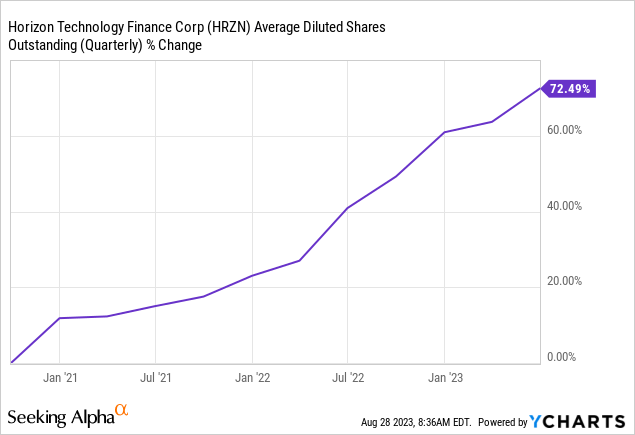

Horizon’s second quarter NAV came in at $355.4 million, around $11.07 per share. This was up from NAV of $290.6 million in the year-ago quarter but was down $0.62 on a per share basis on the back of a 22.4% expansion of its weighted average diluted shares outstanding to 29,747,290 as of the end of the second quarter. Shares outstanding are up 73% over the last three years with Horizon sometimes leaning on equity offerings to raise funds for investments. These have mainly been completed with the BDC trading at a premium to NAV so have been accretive to investment income.

Total investment income for the second quarter came in at $28.12 million, up 51.3% over its year-ago comp and a beat by $1.54 million on consensus estimates. Net investment income was $16.1 million, around $0.54 per share, and up from $8.6 million and $0.35 per share in the year-ago period. It was also a beat by $0.16 on consensus estimates. Hence, Horizon is currently paying out 61% of NII as a dividend with an undistributed spillover income of $1.02 per share as of the end of the second quarter.

Whilst, the expansion of NAV on a nominal basis is countered by the decline on a per share basis, the growth of investment income as expressed by dual beats during the second quarter has set a healthy backdrop for the path of dividends over the next few quarters and heightened the possibility of a large special year-end dividend. Do I think shares are a buy here? Yes.

Read the full article here