In my financial choices, I always suppose starting from 60-40, and I assume that the portfolio is totally invested in two great classics of the market:

60% of the equity is 100% invested in the iShares MSCI World ETF (NYSEARCA:URTH) On the other hand, 40% of the bond is entirely invested in the Vanguard Total World Bond ETF (NASDAQ:BNDW).

Starting from the composition of the URTH and the BNDW I think it is preferable to focus on specific geographical and thematic sectors. For the equity component, there is a particular focus on emerging markets, European REITs and US Small Caps, while for the bond component on European bonds.

It does make sense to maintain a 60-40 composition?

A first question to ask in this historical moment could be, does it make sense to maintain a 60-40 composition?

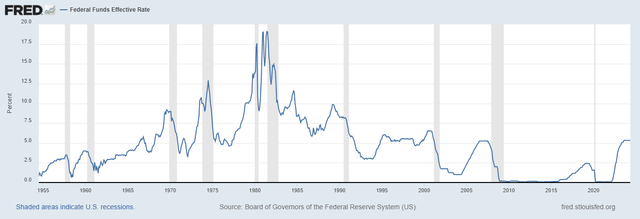

In my opinion, not in the past, but now absolutely. The 60-40 portfolio can be a good compromise even today. There are upcoming events to consider. The first is the opening of the second half of the year, while the second one is the shadow of lower interest rates.

Regarding the arrival of the second half of the year, a study by Sam Stovall, chief investment strategist at CFRA, reassures us about the performance of the stock market: since 1945, the S&P 500 index has recorded an average growth of 5% in the second half of the year when the return of the first half was positive while in years when the index gained more than 10% in the first six months, average gains in the second half were 8%. You can find an interesting opinion of his at the link in this video.

After that, the question must be asked: how should we deal with the possible lowering of interest rates? In my opinion, it is appropriate to maintain at least 40% exposure to the bond market.

As is well known, lower rates could help raise the price of bonds and provide a more attractive return than stocks in a period of increased volatility.

The truth is that the bond market has better return prospects than the same segment of the stock market has experienced over the past 20 years.

(FRED)

Which geographies should be positioned in the equity component?

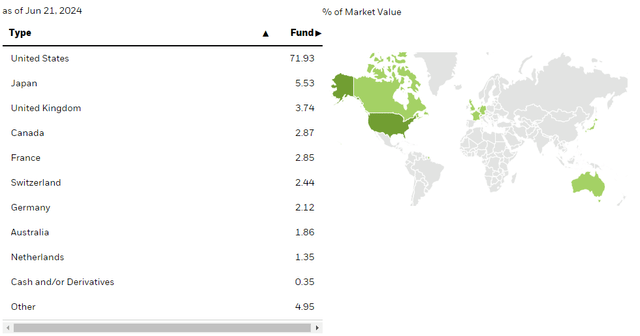

URTH ETF has a composition as follows:

- United States: about 60%

- Europe: about 20%

- Japan: about 10%

- Other developed markets: about 10%

(iShares)

There are undervalued geographic areas that could benefit from the current economic context. In fact, in my opinion, it is a smart choice to maintain more portfolio exposure to emerging economies, such as China. As explained in this article. A smart investment choice, especially considering the depreciation that some developed country currencies might experience during the process of lowering interest rates, might be to select which ETF invests in emerging markets. Such as the one well described in this article, the iShares MSCI Emerging Markets ETF (EEM). EEM, unlike the MSCI Index which is not representative in the emerging markets segment, offers a solution for investing in emerging markets, with a large exposure to China (around 31%).

Does it make sense to follow the sector composition of the URTH ETF?

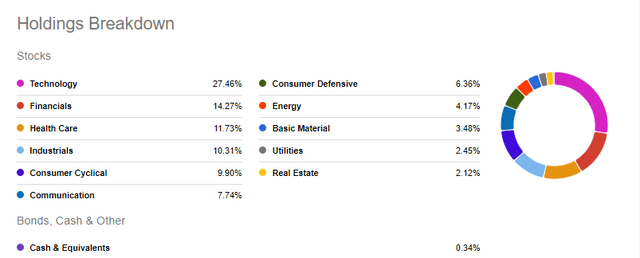

URTH consists of several areas, including:

- Technology: about 20%

- Financial: about 15%

- Health care: about 13%

- Discretionary consumption: about 12 percent

- Industrial: about 10%

- Other sectors: about 30 percent

Seeking Alpha

In view of the lowering of rates, it may be wise to consider changing the positive weight of cyclical sectors that could be weighed down by current financial conditions, such as real estate, and reducing the financials component. This component is already overrepresented in the index, and has also already benefited greatly from the rise in rates in recent years. In this sense, the stock market component of real estate REITs becomes very interesting. A very popular ETF for having a balanced exposure globally is the iShares Global REIT ETF (REET), a nice description of the instrument can be found here.

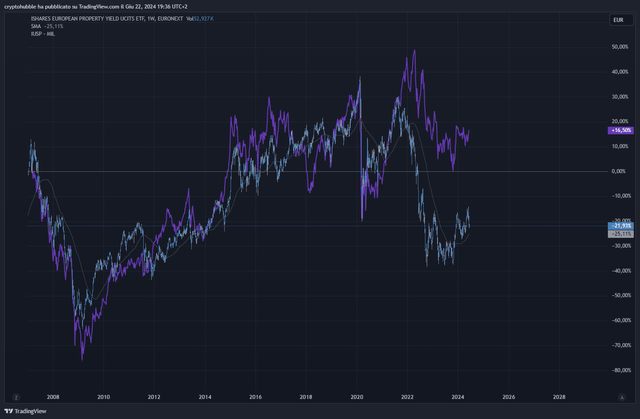

In this regard, I would like to offer my personal perspective. I am of the opinion that it would be intriguing to consider incorporating more European Real Estate Investment Trusts into the portfolio, given their historical trend of aligning with that of the United States. However, it is evident by comparing the US and EU property yields that the activity of real estate trusts in Europe has experienced a greater impact from the increase in rates. Furthermore, given that the ECB has been ahead of the Fed in the initial cuts, it could potentially result in a substantial premium in European REITs.

US Property Yields (TradingView)

On the other hand, despite the technology sector’s significant growth in terms of stock market performance, it continues to exhibit strong fundamentals and sustainable growth, justifying maintaining a good level of exposure.

What about URTH capitalization?

In terms of capitalization, the MSCI World is dominated by large caps, with a small percentage of mid and small caps.

Small caps, on the other hand, could represent an attractive opportunity to further diversify the portfolio. These companies, although riskier, have been plagued on the stock market due to particularly restrictive financial conditions. In a period of falling interest rates, small caps can benefit from better financing conditions and increase their growth. I honestly think there is little to discuss about small caps, I will always prefer the American growth component, and I explain the reasons here.

How do you manage fixed income in a 60-40 portfolio now?

Starting with the BNDW, there is a global exposure to the bond market with a strong US prevalence, around 40%, as it should be in a global fund. I think for the time being, high-yield bonds can be set aside, or at least put in as a minimal percentage. Over the past six months, high yield bond yields have offered attractive returns, but the spread over investment grade has narrowed significantly. As rates fall, the risk premium on high yield bonds may not be as attractive as it has been in the past. Therefore, it may make more sense to increase exposure to investment-grade bonds, which offer a better risk-reward ratio in a falling interest rate environment.

HY – IGY US Spread (FRED)

Regarding geographical allocation, there is an important consideration to be made regarding Europe.

In recent weeks, European government bond yields have risen sharply despite the ECB’s first-rate cut. This has happened because of the intensification of political reasons. However, as explained here, I sincerely think that these instabilities will impact bond prices ONLY in the short term. In the long term, considering a growth rate of the European economy, and the lowering of rates initiated by the ECB, an excellent investment opportunity has been created. For this reason, I think that a solution to include in the portfolio could be the Vanguard Total International Bond Index Fund ETF Shares (BNDX) which excludes the United States and gives a significant weight to Europe (almost 30%).

(TradingView)

Why might these considerations not be suitable for every reader?

As you well know, there are some variables that are decisive for the construction of an investment portfolio.

First, the age of the investor is a key factor: young people tend to be more aggressive, as they have more time to recoup any losses. A young investor may therefore have more exposure to stocks, which offer higher potential returns but also greater volatility.

In reverse, an older investor, close to retirement, may prefer a more conservative portfolio, with a higher allocation to bonds, to protect capital and generate income.

And this is where a second variable comes into play: risk appetite. This last element varies from person to person, can be independent of age, and depend on the needs of an individual at a specific time in life.

Conclusion

In conclusion, the 60-40 portfolio remains a very interesting composition in my opinion. Rather than following the composition of the URTH ETF and the BNDW ETF, it remains an interesting choice to evaluate greater exposure towards geographical areas and sectors that could benefit from this cyclical change in the markets.

Read the full article here