Investment Thesis

HP Inc (NYSE:HPQ) is one of the world’s largest PC manufacturers and printing service providers. Their large range of computers and printers sell in huge volumes despite targeting a lower-end market than some of their competitors.

A difficult 2023 outlook was ignored by Buffett when Berkshire acquired a sizable stake of HP shares earlier in the year. The fiscal year has proven difficult for the firm with declining margins and falling revenues defining the annum for the legacy PC giant.

Nonetheless, a great valuation places shares at a potential 50% undervaluation relative to their intrinsic value. I believe Buffett sees a slow-burn cigar-butt style opportunity whereby patience combined with the undervaluation could see outsized returns for the value conscious investor.

Company Background

HP.com | Homepage

Hewlett-Packard is the world’s second largest personal computer manufacturer by volume. The firm produces a wide range of personal electronic devices such a laptops, desktop PCs and tablets. HP also manufactures and sells a large number of printers and auxiliary electronic office equipment.

Since the firms founding in 1939 as an electronic test equipment innovator, the firm has become one of the most influential PC manufacturers with a 2015 spinoff splitting the firm’s personal computer and printing division (HP Inc covered by this article) from the firms Enterprise oriented business.

With Chip Bergh as chairman and Enrique Lores as president and CEO, the firm has adopted a newfound focus on margin expansion, market-share growth and portfolio revenue maximization. Post-spinoff many investors have been concerned that HP is a ship without a captain to steer towards a more profitable and sustainable future.

I believe Lores is fit for the role and has already begun to create tangible evidence that the strategic plan derived under his leadership is suitable and relevant to the incredibly competitive market environment HP currently faces.

Economic Moat – In Depth Analysis

Analyzing and attributing a moat to HP is quite a difficult task but I do believe that the firm holds a narrow economic moat. While HP has an undeniable presence in the PC market being the second largest producer by volume only to Lenovo, the firm has done little to truly differentiate their product offerings.

A similar situation is present in their printing business segment which while profitable, is not particularly unique compared to competitors such as Canon (OTCPK:CAJPY) or Xerox (XRX).

The issue with HP’s laptop and desktop PC “personal systems” segment is that their products are simply not differentiated enough to create any real moatiness for the firm.

HP.com | All Laptops

While many of their newest and historic product offerings have garnered significant praise from reviewers and critics for being great devices, the company has failed to create a real product ecosystem like Apple has with their Mac line of computers.

This failure to create a real image in the PC market as being anything more than one more competitor ultimately stems from the HP brand struggling to evoke emotion or a connection with consumers. HP is considered by many to be a “legacy” manufacturer whose reputation while reliable is in no way exciting or trendy.

While HP’s laptops may offer better performance and value to consumers than competing products such as those from Apple (AAPL), Dell (DELL) or Lenovo (OTCPK:LNVGY), the lack of brand image and modern reputation leaves HP battling these competitors on price alone.

Fundamentally it is this lack of pricing power HP holds even with their 24% share of the PC market that in my mind prohibits the assigning of moat to this business segment. Without pricing power, HP cannot earn outsized returns on this business and exposes their market share to erosion from competitors should the company try to increase prices.

HP.com | Printers

A similar situation exists with their printing business. HP is the largest printing supplier in the world with a long history of producing cheap and easy to use inkjet machines aimed at the private consumer market. I myself have had only HP printers thanks to their cost-effective and reliable nature.

However, for the company this segment while profitable once again fails to create any tangible economic moat that would protect their operations and market share from competitors. Quite simply the lack of any real product differentiation has led to HP once again competing on price and value.

This has led the company to adopt an interesting sales strategy for their printers whereby the company sells the actual devices at a loss. Instead, the firm aims to capture revenues from the recurring sale of ink cartridges, paper and subscription services for their printers.

I believe this subscription-oriented strategy is perhaps the only way for HP to create tangible profits from this otherwise matured and declining business segment. The firm has identified that money cannot be made on device sales, so selling at a loss to increase market share and the ensuing revenues from ink and paper sales is the best way to extract profitability from the business.

Oftentimes one can find HP DeskJet class inkjet printers on sale for around $50 at retailers such as Walmart or Target even without considering any sale reductions. HP’s most compatible 67-line of ink cartridges for the very same machine cost anywhere from $26-$30 depending on color, black and size variations.

While their approach to this segment is innovative, I still find it difficult to assign moatiness to HP’s printing business. The reality is that HP is competing purely on price and still lacks any ability to control prices in a positive direction. It would equally be just as easy for a customer to purchase a Canon or Xerox printer compared to sticking with HP as a brand.

Nonetheless, HP’s sheer scale of operations does garner the firm significant economies of scale and operational synergies that aid with improving the cost effectiveness of their manufacturing and marketing processes.

HP is notoriously tough with suppliers and has been known to negotiate hard to get the best possible supply deals. The firms scale helps with these negotiations as a supply deal with HP can be a critical lifeline for some smaller suppliers.

This helps HP minimize their COGS and extract some slim margins from their relatively undistinguished business segments. Without their scale and legacy earnings, HP would not exist today.

While the effects are quite small, I do believe HP’s scale and (while unexciting) reliable reputation earns the company a narrow economic moat. Their legacy status as an established and reputable PC and printer manufacturer makes their products a steady and familiar pick for many consumers while their value pricing acts to further capture the lower-end of the market.

Assigning any duration of lasting competitive advantage as arises from their narrow economic moat is essentially impossible as they lack tangible pricing power and brand image.

Regarding the title of this article and considering the relatively lack lustered moatiness present at HP, it is difficult to understand what Buffett’s Berkshire Hathaway sees in HP stock. Traditionally, Berkshire and Buffett have targeted companies with solid economic moats that allow the firm to control prices and produce oversized returns on their invested capital.

The Oracle from Omaha and his fund have a huge stake in one of HP’s fiercest upmarket competitors: Apple. The sizable 1.07% (over $3.7B) stake Berkshire has taken in HP suggests the company sees a bright future perhaps for the PC market in general with HP stock being another way to capture this believed growth.

Buffett has the benefit of being able to call essentially any CEO in the world and extract un-publicized truths and expectations. Nonetheless, it is difficult to see exactly what Buffett and Berkshire see in HP from an economic moat standpoint. The pick is definitely more unusual for Buffett from the perspective of a smaller professional investor.

Financial Situation

The last five years have been relatively decent for HP regarding their fiscal performance. The company has managed to expand their margins to achieve 5Y average gross, operating and net margins of 19.39%, 7.14% and 6.77% respectively.

While these margins are not unappealing, they begin to look particularly mediocre when compared to those of their much smaller competitor Apple who have managed gross, operating and net margins of 40.34%, 27.34%, and 23.44% respectively.

HP and Apple have relatively different business models and thus cannot be compared directly, but the huge difference in these margin metrics for two business operating in equally competitive markets illustrates the importance of having a robust economic moat that provides significant pricing power.

For the same 5Y period HP has managed ROA, ROE and ROIC of 11.72x, 8.04x and 3.93x. The relatively low ROIC in particular is concerning and once again illustrates the truly slim margins HP is able to extract from their value-oriented business.

Warren Buffett in particular is keen on business having strong ROIC and ROE figures which HP simply has not been able to produce. While the firms TTM ROIC is a much more respectable 9.01x, the relatively moatless nature of their key businesses places any long-term outsized returns into speculative territories.

HP operates on an average of around 120 days payables which supports the thesis that HP is tough on suppliers. While this is positive for the firm from a cash flow perspective, HP must ensure that they do not compromise any business relations in the name of reducing supply prices by a couple percentage points.

These very basic operating performance metrics illustrate that HP is fundamentally a profitable business. While their margins are slim, the company has consistently even through difficult macroeconomic conditions continued to produce positive returns from their businesses.

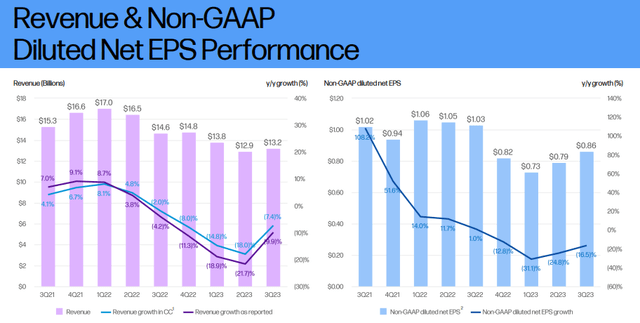

HP Q3 Result Press Release

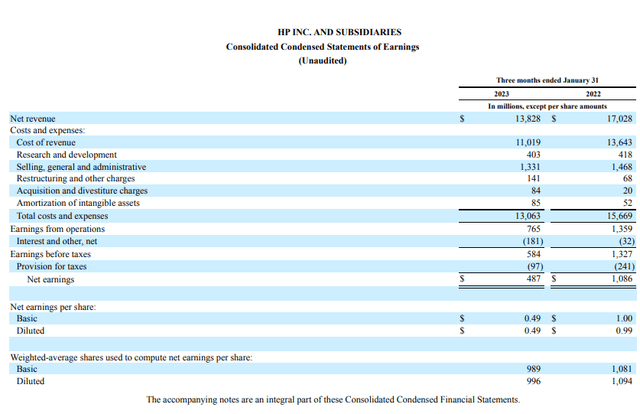

Considering HP’s FY23, the firm has had a turbulent annum. Q1 saw net revenues for both their Personal Systems (PS) and Printing segments down 24% and 5% YoY respectively. This was primarily due to softening demand for devices both by consumer and commercial users. The firm also saw -$0.2B in FCF for the first quarter.

Q1 saw the firm’s PS segment’s operating margin drop to just 5.4% which illustrate just how sensitive the business is to falling revenues and sales figures. The printing business operated on a much healthier 18.9% operating margin.

HP Q1 FY23 10-Q

The first quarter saw the firms COGS increase substantially from being 70% of revenues to accounting for almost 80% of all revenues earned. This illustrates and explains the significant margin contraction experienced in the quarter.

While regrettable, the highly inflationary macroeconomic environment has resulted in labor costs and raw material prices increasing substantially. HP struggled to control these costs at the start of the fiscal year.

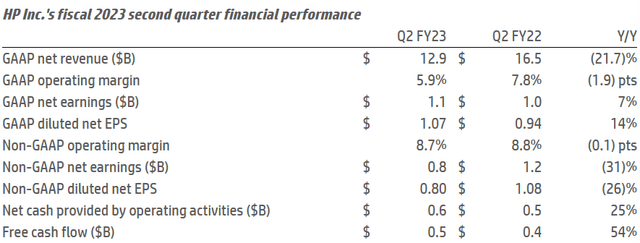

HP Q2 FY23 Press Release

Q2 saw a similar story with net revenues dropping 22% YoY and operating margins for the firm as a whole declining 1.9pts to just 5.9%. However, the firm was able to generate $0.5B in FCF and overall managed to deliver non-GAAP EPS of $0.80 which was at the high-end of their target.

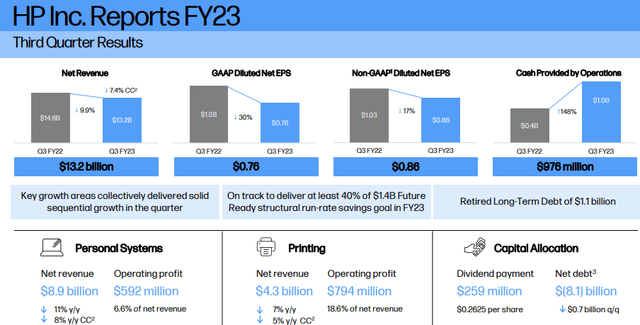

HP Q3 Report

This slow turnaround in business profitability has been continued by the firm in their latest Q3 report which saw YoY sales decrease by just 9.9% and operating margins decline by just 1.4pts YoY to 7.2% for the quarter. FCF for the quarter increased 214% YoY to $0.9B.

HP also reported that total PS unit sales were up 3% thanks to an 8% increase in the volume of consumer PS sales and flatline commercial PS unit sales. The firm’s printing business unfortunately saw total hardware sales decrease by 19%.

While CEO Lores was positive about the excellent growth in PC market share and achieving their non-GAAP EPS target of $0.81-$0.91 by posting diluted EPS of $0.86, the truth remains that HP has seen their margins contracting over the 2023 fiscal year.

The firm’s COGS have decreased by 6% as a portion of revenues which is welcomed to see and suggests their new cost-targeting strategic plan is working effectively. Such an improvement in COGS primarily thanks to a reduction in their supply chain inefficiencies during a particularly difficult macroeconomic environment does suggest that HP has been able to tangibly improve the efficiency of their business.

This is reflected in their TTM ROIC improving and suggests that HP may be becoming a leaner and more slick operation. Inventories for Q3 also continued to decrease down to just $7.1B compared to $7.6B in FY22 which supports HP’s claims of growing hardware sales volumes.

While these market share and volume improvements particularly in the PS segment is very good to see, it is a shame HP has been unable to capitalize on these improvements in the form of outsized returns and growing profits.

The lack of improvement in revenues from the segment suggests HP has been selling at least a portion of their PS devices at a loss to improve market share. While this is an understandable strategy in the Printing business, the lack of recurring sales associated within the PC market suggests HP’s ability and influence to sell may have decreased further.

In a market environment where Apple Macs continue to gain in popularity and where competitors such as Dell and Lenovo are keen to grow their own market share and reputation, any weakness by HP could result in long-lasting consequences.

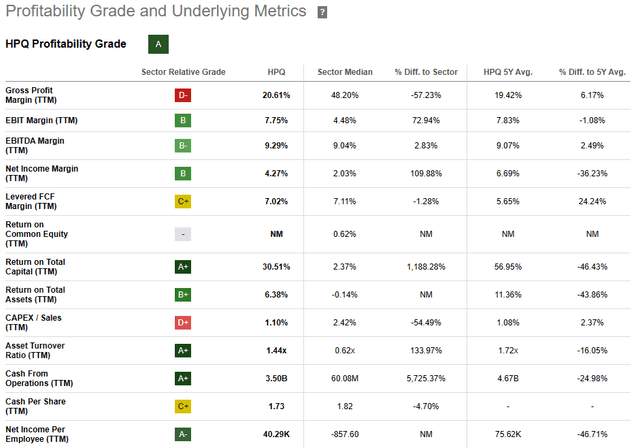

Seeking Alpha | HPQ | Profitability

Seeking Alpha’s Quant assigns HP with an “A” profitability rating. I believe this is a reasonable summary of HP’s current profit generation abilities.

Considering the firm’s balance sheet, HP looks relatively secure. The firm currently has $17.46B in total current assets with their total current liabilities amounting to $25.19B. This current illiquidity leaves the firm with a current ratio of just 0.71 and a quick ratio of 0.34.

Nonetheless, the firms return to relatively healthy FCF should help service any short-term obligations and as a result I do not see HP needing to acquire any new revolving credit facilities or lines of credit to finance these debts.

HP’s total debt/equity ratio is 1.06 which illustrates that HP has a significant portion of debt on their balance sheets.

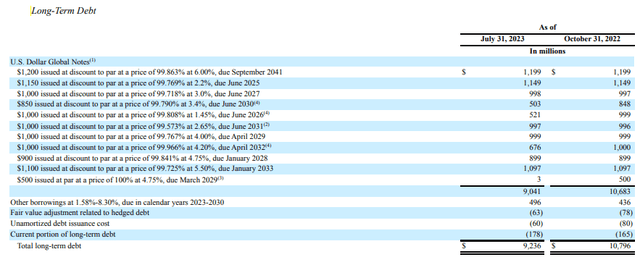

HP FY23 Q3 10-Q

The firm’s material cash requirements for the financing of long-term debt amounts to $9.24B.

The earliest maturities of these debentures is 2025 with a majority maturing well beyond 2030. This staggered and well-executed debt repayment profile reduces the risk HP faces of illiquidity. I believe HP is well-managed and has a relatively healthy capital allocation state.

HP has obtained a Baa2 credit rating from Moody’s for their senior unsecured domestic notes. The agency believes the outlook is stable for HP. Baa2 is classified as credit obligations which are “judged to be of medium grade” by Moody’s.

Overall, I believe HP is a recovering firm that is gaining in market share but experiencing contracting margins due to overall weakened pricing. While their cost reduction initiative is working and the company is becoming leaner, the continuously falling profits from their PS and Printing segments is concerning.

Valuation

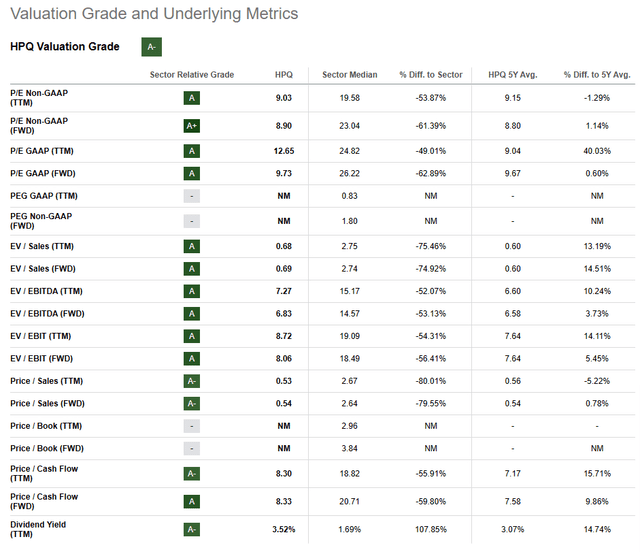

Seeking Alpha | HPQ | Valuation

Seeking Alpha’s Quant assigns HP with an “A-” Valuation rating. I believe this is an accurate depiction of the value proposition currently present in HP stock.

The firm currently trades at a P/E GAAP FWD ratio of 9.73x along with a P/CF TTM of just 8.30x. Their FWD EV/EBITDA of 6.83x is excellent especially when considering their EV/Sales TTM and FWD of just 0.69x and 0.68x respectively.

These basic valuation metrics suggest HP is trading at quite a significant discount compared to its relative valuation.

Seeking Alpha | HPQ | Summary Chart

From an absolute perspective, HP shares are trading at higher valuations thanks to the last 10 years having seen steady value generation by the firm leading to a 21% per annum average return to shareholders.

While the relative valuation provided by simple metrics and ratios along with the absolute comparison being to paint the value picture present at HP, a more qualitative assessment must be made.

The Value Corner

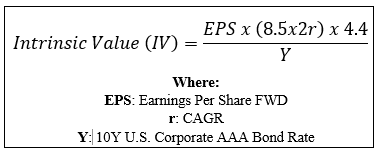

By utilizing The Value Corner’s Intrinsic Valuation Calculation, one can better understand what value exists in the company from a more objective perspective.

Using HP’s current share price of $29.30, an estimated 2023 EPS of $3.31, a conservative “r” value of 0.04 (4%) and the current Moody’s Seasoned AAA Corporate Bond Yield ratio of 4.95x, I derive a base-case IV of $48.90. This represents a substantial 40% undervaluation in the firm.

When using a marginally more optimistic CAGR value for r of 0.06 (6%), HP appears to be undervalued by around 52% with an intrinsic value of $51.80 per share.

Considering the valuation metrics, absolute valuation and intrinsic value calculation, I believe HP is soundly trading in deep-value territory and could potentially present a lucrative long-term buy and hold play.

In the short term (3-12 months), I find it difficult to say exactly what may happen to valuations. While the historic performance of HP stock has been consistent generating linear value growth for shareholders, the sustainability of this in the coming months is almost impossible to guarantee.

The firm’s short-term performance is also tied to the general sentiment surrounding U.S. and global economic performance as a whole with a recession potentially leading to dropping share prices. A softer than expected Christmas retail season could also see HP sales lag YoY figures which could send share lower in the short term.

In the long term (2-8 years), I see a slightly brighter outlook for HP. Their position as one of the largest and most reputable if not exciting PC and printer manufacturers helps produce consistent sales. Market share expansion will see the company generate larger volume sales figures, but HP must try to sell more “fat margin” devices to ensure revenues grow equally.

Even despite any great increase in sales and revenues, HP stock appears to be significantly undervalued from a quantitative perspective. I believe a share price increase to better represent the intrinsic value at HP is due and that this could happen in the 2-8-year timeframe.

Seeking Alpha | HPQ | Dividends

On top of this, HP has a history of share repurchases and a healthy dividend yield of around 3.57%. This should help produce good returns for shareholders even if the firm’s overall business doesn’t see much margin expansion or revenue growth.

Risks Facing HP

HP faces a few material risks which arise from the narrow moat nature of their businesses. The primary issues stem from their lack of pricing power in the PS segment exposing the company to declining margins as well as the overall decline in demand for their more profitable printing business products.

Without a sustainable and tangible economic moat HP has no ability to control prices and charge a premium for their devices. While this does mean that the company is able to sell a significant volume of devices with a great value proposition to customers, there is no real reason other than price for a consumer to choose a HP device.

This means that any pricing competition from competitors Dell or Lenovo will need to be matched by HP in order to retain sales and market share. Such a ‘race to the bottom’ scenario will lead to deteriorating margins in the firm’s PS segment and overall declining revenues.

HP’s more profitable printing business also faces the overall threat from a decline in demand for printing services. As more individuals, businesses and institutions move towards paperless processes for conducting their operations, the demand for printers, paper and ink will decline accordingly.

This means that HP’s second key pillar to profitability and returns is in direct risk of going the way of the dodo. Without a doubt the steady decline of this key segment will harm future returns and long-term profitability of the company.

While diversification into 3D printing technologies may help HP maintain a competitive position within the printing segment, the lack of current commercial applications of their equipment means the possibility of this innovation succeeding traditional printing is speculative.

From an ESG perspective HP faces very little risk. The firm is dedicated to ensuring it is a friendly and positive place to work while also guaranteeing that their entire supply chain will be carbon neutral by 2040.

For a more ESG conscious investor, HP may be one of the best tech companies at satisfying the increasingly stringent demands corporations are facing for environmental, social and governance responsibility. Of course, opinions may vary and I implore you to conduct your own ESG suitability research should this be of concern to you.

Summary

HP is a difficult company to unravel from a valuation, long-term outlook and profitability perspective. It is undeniable that the company has been able to generate steady value for shareholders by operating an excellent business despite having little to no pricing power.

Then again, the decline of the printing business both globally and at HP does mean that one of their key revenue streams will likely face a steady and continuous decline as years go by. Unless the firm can find a new business in which to extract healthy margins, the firm’s overall profitability will surely fall.

The Motley Fool

Considering this all I can ask myself is what does Buffett see in HP? I believe it’s a hybrid between a cigar-butt and a high-quality company. It is undeniable that the great leadership at HP in the form of Lores at the helm is helping the company to become slicker and more efficient which is evidenced by their years of continuous outsized investor returns.

However, the overall decline in the firm’s printing business combined with what seems like falling pricing power and an aging legacy image is less than positive. All of this is surrounded by an intrinsic undervaluation in shares and the potential for an almost 50% increase being required to represent the firm at a fairer valuation.

Considering these factors, I rate HP as a Buy thanks to the significant undervaluation in the firm. A cigar-butt scenario may be on the cards whereby the firm may not have much left to give, but an intrinsic and substantial deep-value opportunity exists which a value-oriented investor with lots of patience may be able to exploit successfully.

Read the full article here