Summary

I am recommending a buy rating for HP Inc. (NYSE:HPQ), as I believe the business is able to grow as guided, driven by the growth tailwinds it is enjoying. Importantly, management has reiterated their intention to return 100% of FCF to shareholders, making the upside much more attractive.

Business

HPQ offers a variety of offerings, ranging from personal systems (PCs) to printing solutions (including 3D printing). Their offerings work for both business and consumer (home) usage and are available worldwide. The business reports are divided into two key segments: personal systems, which comprise commercial and consumer systems, and printers, which comprise supplies, commercial printing, consumer printing, and others (3D printing is included here).

Financials/Valuation

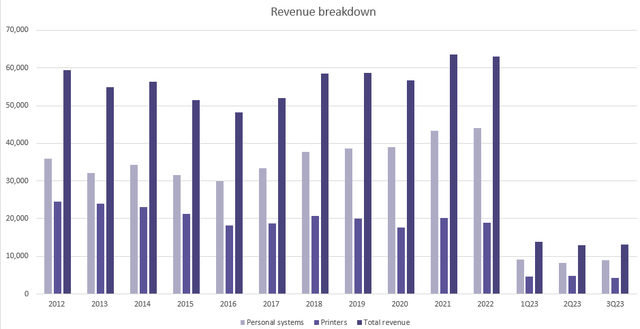

Based on author’s own math

In the initial period of the past 10 years, HPQ saw revenue decline between FY12 and FY16 before it started to increase until today. A breakdown view suggests that the Personal Systems segment is the one driving the returns in growth, while the Printer segment has continued to be a headwind since FY12. Nonetheless, HPQ is a very cash-profitable business that has continuously generated positive FCF over the past years, maintaining a mid- to high-single-digit FCF margin performance. This strong FCF profile enabled HPQ to sustain its high net debt position of ~$9.2 billion as of LTM (~1.8x FY23 EBITDA).

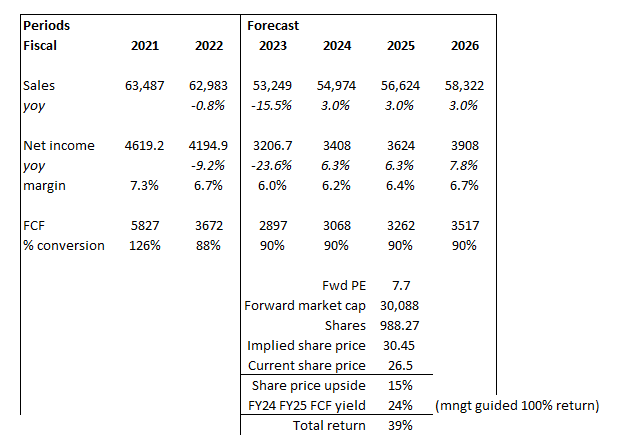

Based on author’s own math

Based on my view of the business, HPQ should be able to grow at 3% (the midpoint of its guidance) over the next few years. Note that I annualized 9M23 revenue and earnings to derive FY23 estimates. A key part of my model assumption is that margin will gradually increase back to FY22 levels, driven by the margin tailwinds discussed below. This is also in line with management guidance for EPS to grow at a high single-digit CAGR (HPQ has bought back around 2+% shares per year in the last 2 years). If we include this in my net income growth, that brings it to a high single-digit CAGR. As for FCF, I assumed it will continue to convert net income to FCF at similar rates to FY22, and 100% of FCF generated between FY24 and FY25 will be returned to shareholders. That said, I expect HPQ to trade at a discount relative to peers’ valuations as its growth profile is much slower (~low single digits vs. peers mid-to-high single digits).

Peers overview:

- ACER: 19x fwd PE / 7% 1Y forward rev growth

- Asustek: 13x fwd PE / 6% 1Y forward rev growth

Based on my model, I have a total return expectation of 39%.

Comments

After reviewing HPQ’s analyst day last week, I believe the stock has an appealing upside, especially after management reiterated its long-term financial targets. To give a refresher, HPQ reiterated 2 to 4% revenue growth, low-to-mid single-digit percentage growth in operating profit dollars, and high-single-digit percentage non-GAAP EPS growth. Of the guidance, the most important one is that management reiterated their intention to return 100% of FCF to shareholders and dividend growth at least in line with net income.

As I laid out above, the revenue mix of HPQ has shifted gradually over the past few years to a focus in personal systems, which I believe has a new secular tailwind that will help drive growth. Management has highlighted AI-enabled PCs as a growth catalyst in the analyst day, noting that they will cause the industry to expand from $470 billion in CY23 to $537 billion in CY26, a CAGR of 4.4%. In my opinion, the introduction of computers with built-in AI is the spark the personal computer market has been waiting for. AI-enabled computers outperform traditional computers in terms of productivity, allowing business users to dramatically increase their output. Even though AI-enabled computers aren’t widely used yet, I predict that as we progress toward a world where AI is integrated into every aspect of work, they will quickly become a necessity. Importantly, these AI-enabled PCs are naturally more expensive with more functionality and improved productivity, giving HPQ the opportunity to raise its effective pricing. HP’s partnerships with major AI-silicon providers, such as Nvidia, position it to capitalize on this trend, in my opinion. In addition to the AI-enabled PC, the gaming PC market is expanding at a much faster rate than the overall PC market. Given that HPQ’s product portfolio has the right offerings to meet this growing demand, this is encouraging for HPQ’s future expansion prospects.

HP’s portfolio, which includes brands like Omen and HyperX, enables us to offer both integrated solutions across gaming PCs and peripherals, and also go after the broader market opportunity by designing HyperX peripherals to work across the gaming PC and larger console ecosystem. Analyst day

I was worried that HPQ’s Print division would be a money loser for the company. Nonetheless, I was relieved to learn that management has raised the 16-18% operating profit margin it had previously projected for the Print segment to the 16-19% range. Given the success of HPQ’s Print profit growth strategy, I think they’ll be able to hit their goal. As a result of the company’s focus on maximizing customer lifetime value, HP has seen a 25% increase in Instant Ink subscribers since 2021 and has revealed that 60% of revenue is now accounted for by profit upfront sales. The fact that Print is experiencing a 20% decline in average customer value is a major headwind, I concede. However, given the growing proportion of Instant Ink in the mix, as well as the expansion of Services-both of which are repeat businesses that should increase lifetime value-the actual effect may be less dramatic than the headline suggests.

In addition, HPQ is exploiting synergies between its Personal systems and Printing solutions to seize opportunities in the Workforce Solutions market. Managers anticipate a 4.6% CAGR for the Workforce Solution TAM, bringing it to $182 billion by CY26. This is comprised of moderate growth for both Lifecycle Services and Managed Solutions, and a much more rapid 10% CAGR for Digital Services, as reported during analyst day. Management pointed to the rollout of Workforce Central as an example of how it is simplifying the portfolio and thereby driving greater market penetration in areas like IT fleet management for enterprises. The most important takeaway is how the increased attach rate of software and solutions benefits HPQ’s bottom line.

Overall, I believe HPQ should have no issues meeting its growth guidance given all the tailwinds that it is going to enjoy. Notably, the improved profitability is supportive of HPQ’s ability to generate cash, which is a key part of the bull case as HPQ intends to return 100% of FCF to shareholders if it can hold its gross leverage below 2x EBITDA.

Risk & conclusion

If hybrid work increases or consumer demand grows more slowly than expected, commercial PC demand revenue could fall short of projections. The industry’s high channel inventory, falling component costs, and increased discounting could all lead to lower margins. There may be less need for new commercial PCs if layoffs increase in the workplace.

In conclusion, I recommend a buy rating for HPQ due to the promising growth prospects and commitment to returning 100% of free cash flow to shareholders. HPQ’s diversified offerings encompass personal systems and printing solutions, with a strong focus on personal systems driving growth. The company’s emphasis on AI-enabled PCs and its expansion in the gaming PC market are encouraging signs for future growth. In the Print division, improved profitability and growing Instant Ink subscribers support its long-term prospects. HPQ’s ability to leverage synergies between personal systems and printing solutions, along with a focus on Workforce Solutions, further bolsters its profits outlook. However, potential risks include the impact of hybrid work trends and slower consumer demand on commercial PC revenue, as well as margin pressure from industry dynamics and reduced demand in the event of corporate layoffs.

Read the full article here