The financial services industry hasn’t had a good 2023 at the stock markets, at least not so far. The S&P 500 Financials index is up by just 2.1% and the Bank index is actually down by 12.2%. This is in sharp contrast to the 19% increase in the S&P 500 (SP500) index.

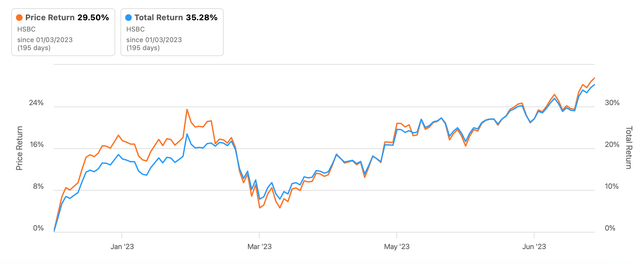

It might be tempting to write off the sector right now based on the recent performance and considering the slowdown can impact financials as cyclicals. But there are some financials that are still performing quite well even now. A case in point is HSBC Holdings (NYSE:HSBC), which is up by 29% year-to-date [YTD].

There’s also its dividend to consider, which isn’t bad at all. HSBC’s trailing twelve months [TTM[ dividend yield is at 5.1%, which is also superior to the financial sector’s median yield of 3.7%. As a result, the total YTD returns from the stock are at over 35% (see chart below).

Returns (Source: Seeking Alpha)

Strong and growing financials

The big question then is, what’s making HSBC tick right now? For one, its numbers are strong. They had strengthened already in 2022, as its diluted earnings per share [EPS] grew by over 19% year-on-year. On the face of it, this could well be attributed to better net interest margins [NIM], which rose to 1.48% from 1.2% in 2021 as interest rates inched up. This commensurately showed up in the income statement as a rise in the net interest income by 23%.

But the fact is, that its operating profit actually declined in 2022 on heads like lower fee income and an impairment loss on plans to sell off its French retail banking operations. A significantly reduced tax expense came to its rescue, resulting in a bump up in its net income.

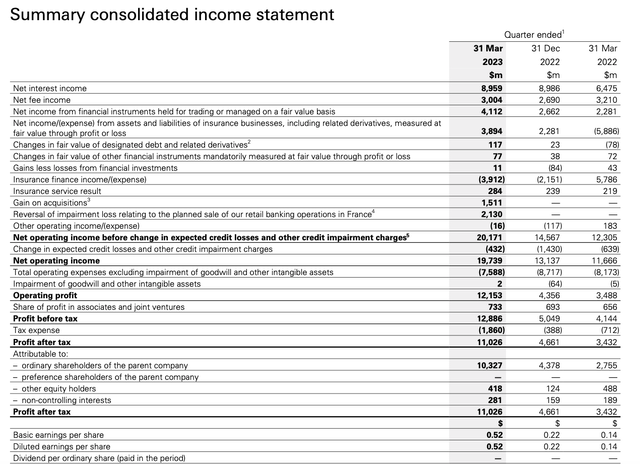

Positive as the outcome was, it’s hardly the ideal way for any company to grow profits. This brings me to the second reason as to why HSBC’s stock is doing well right now. In the first quarter of this year, it showed a genuine improvement in numbers. Its operating profit rose by 3.5x as its NII growth strengthened to 38.3%. Other income heads bettered (see table below), and significantly, the company reversed the impairment loss on its French retail business from 2022. Analysts expect continued strong financial performance in the upcoming quarter, results for which are due in August, and the year ahead is also something to note.

Income Statement (Source: HSBC)

The China opportunity and challenge

HSBC is not without its challenges though. Counterintuitive as it sounds, a big one is China. Don’t get me wrong, China, including Hong Kong, is a notable money spinner for the bank. In 2022, it accounted for a third of the bank’s pre-tax profits.

In fact, at the end of 2019, it set a still ongoing restructuring process in motion to focus more on its Asian market and reduce its exposure to markets like the US and Europe, which appears to be paying off. In the past three years, its diluted EPS has seen a compounded annual growth rate [CAGR] of a huge 84.3% compared to a tiny 1.6% for the past decade.

It might come at a cost, however. The company points to the risks stemming from the challenging relationship between China and other countries. Sanctions have been imposed on Chinese companies by the EU and the US and it in turn has imposed counter-sanctions. This can turn into a complicated situation for HSBC, which has interests around the world.

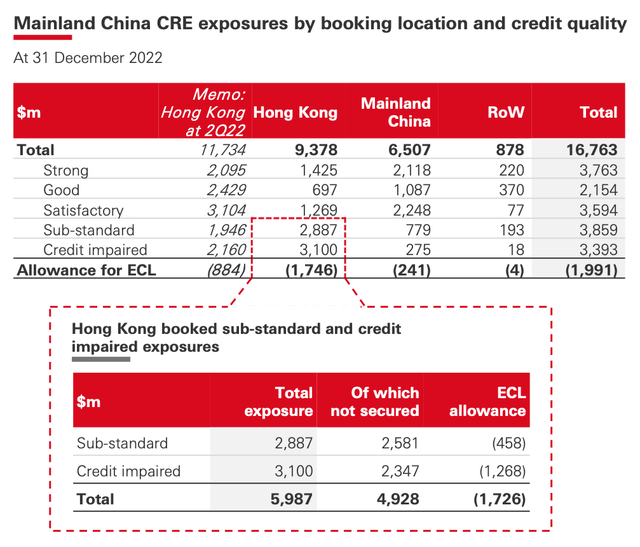

There is also the question of HSBC’s exposure to China’s commercial real estate sector [CRE], which has slumped and is only expected to see a slow recovery. To be fair, the bank’s exposure to the sector is limited to less than 2% of its total loans. At the same time, if it has to set aside bigger amounts for impairment losses, it could become a drag on its earnings. At the end of 2022, more than half the CRE exposure to Hong Kong, in particular, was seen as either sub-standard or credit impaired (see table below).

Source: HSBC

Attractive market valuations

Coming to HSBC’s market valuations shows that the bank looks attractive. With analysts bullish on HSBC’s earnings for 2023, its forward price-to-earnings ratio is competitive at 6.9x compared to the 9.85x for the financial sector. Its trailing twelve months [TTM] is also relatively low at 7.25x compared to the 9.8x for the sector. This is particularly interesting considering that financials haven’t done so well on average this year at the stock markets, while HSBC’s share price has been on the up and up.

It does need to be borne in mind, however, that HSBC’s long-term price performance is weak. Price returns are actually -28.1% over the past decade, which means just based on price returns investors actually lost money. The saving grace has been the dividends though, with total returns on the stock rising to 21.7%. With the restructuring underway, as discussed above, this can change. In fact, it’s already showing signs of improvement. But weak past performance is still worth keeping in mind, especially considering the China challenge.

What next?

All said and done, however, I like where HSBC’s at right now. The stock’s trading at a lower price than its peers, and despite the solid performance it has seen in the first quarter of 2023. With its important Asian market relatively insulated from the slowdown in Europe and the US, the bank has a good chance of outshining other financials right now. This already shows up in investor confidence in the stock YTD.

It’s not without its challenges of course. A key one is its vulnerability to China’s property market, which might see a multi-year slump. This can be a drag on HSBC at a time when the country’s economy had just come back to life after last year’s lockdowns. At the same time, it’s some consolation that the sector is only a small part of the bank’s overall loan portfolio. A weak long-term stock performance also doesn’t work in its favor.

It’s not all sunny days ahead for HSBC, to be sure, but for now, it does look like it’s on the right track. If nothing else, its dividends certainly look healthy. It’s a Buy for me for now. But I would watch developments with the bank keenly.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here