Thesis

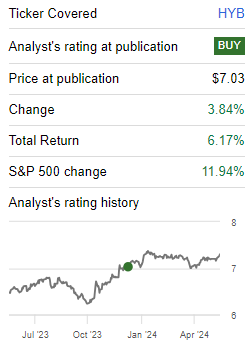

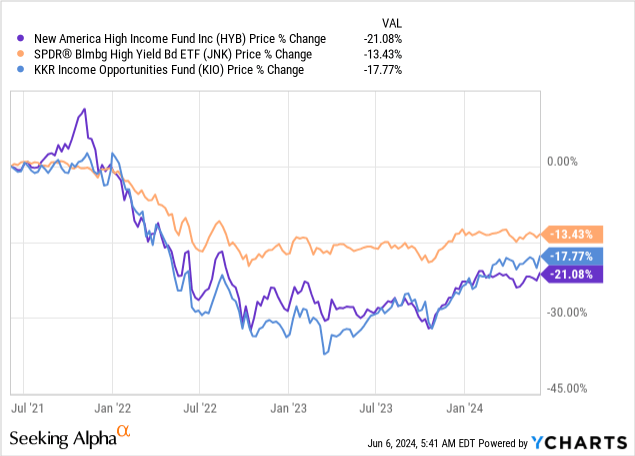

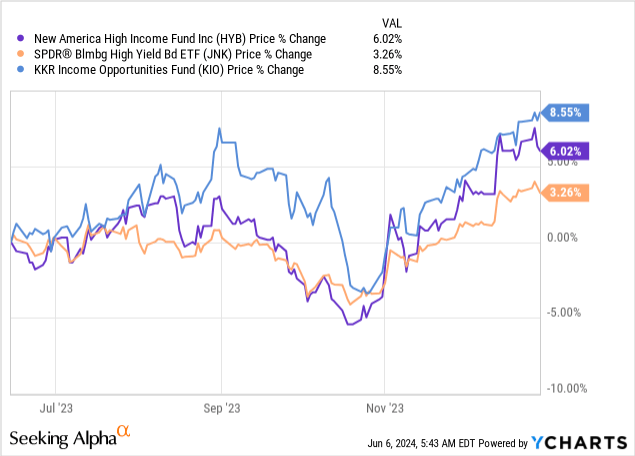

We last covered the New America High Income Fund (NYSE:HYB), a CEF we hold in our portfolio, roughly six months ago. In our last article, we wrote about the CEF’s very wide discount to net asset value and the appealing entry point presented. The CEF is up since our rating:

Prior Rating (Seeking Alpha)

Given the persistent high risk free rates and the compression of high yield spreads, we are going to revisit HYB and highlight why the CEF does not present an appealing entry point anymore. Furthermore, we are going to outline the reasoning behind considering this name a ‘Hold’ and DRIP-ing the dividends into the fund.

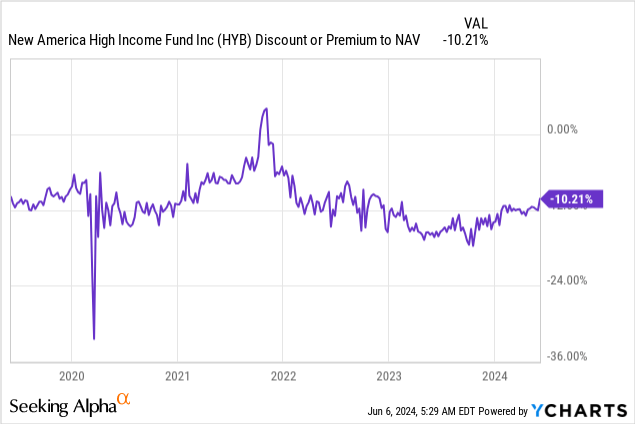

The discount has narrowed

One of the structural features that was mispriced the last time we covered this name is represented by the discount to NAV. Back in December 2023, we wrote:

We can see from the above graph courtesy of YCharts that the CEF usually sees its discount in the -10% to -12% range in a normalized rates environment, with fluctuations as rates move up or down. In the 2020/2021 zero rates environment the fund traded even at a premium to NAV (it was overpriced at that level). Currently, we find it to be underpriced from a discount to NAV perspective.

The discount has now narrowed to its historic range and is currently -10%:

We do not expect any further tightening here until the Fed actually starts lowering rates. The reason behind this statement is constituted by the fund’s leverage which is floating rate, and thus has hampered the CEF’s performance in a high rates environment.

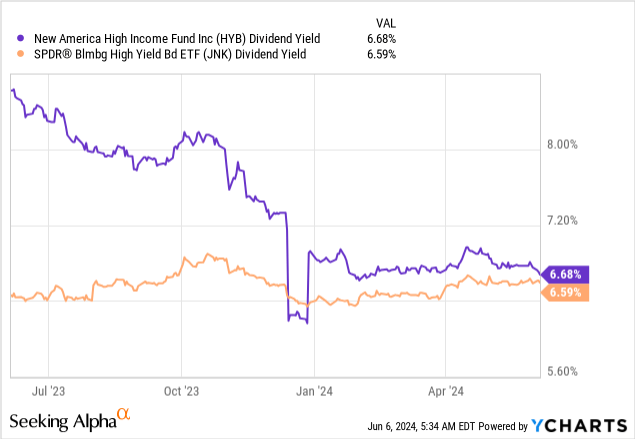

The high cost of leverage has reduced the dividend

When an investor buys a CEF, they buy a leveraged structure which is supposed to yield more than unleveraged funds. However, HYB has been severely hampered by its floating rate funding:

As the fund rolled new holdings and the cost of funds based on higher rates took full effect, we have seen a significant deterioration in its dividend yield. Currently, the CEF has the same one as the SPDR Bloomberg High Yield Bond ETF (JNK) at roughly 6.7%. This is too low for a leveraged structure in our opinion. While we are happy to hold here, we would not purchase more at today’s levels.

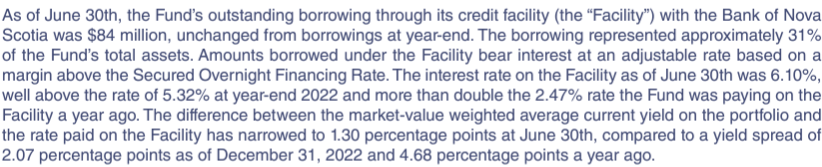

As a reminder, the fund has a bank facility which costs SOFR + 100 bps:

Bank Facility (Annual Report)

Until SOFR moves lower significantly, the fund will have a hard time making a substantial net interest margin given its conservative portfolio build.

What is the downside like for this CEF?

We initially took a liking to HYB because the fund has been in the market for a long time and has a conservative credit risk build. Let us look at how the name did from a drawdown perspective in 2022/2023:

During 2022 when both rates and credit spreads went up, the CEF had a -30% drawdown from a price perspective, versus only -13% for the unleveraged JNK. It is interesting to note however the CEF’s performance during the October/November 2023 market risk-off event:

Given rates were already high, the fund suffered only from the widening of credit spreads, but had a drawdown similar to the unleveraged JNK, all while KIO had a much larger one. We are penciling in a -10% drawdown for the CEF during the next severe risk-off event, based on its historic performance in a high rates environment. The fund’s risk metrics also support this view, with the 3-year standard deviation at 12.5%.

Portfolio is still conservative

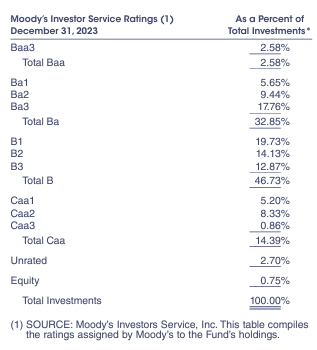

The fund has a high concentration of ‘BB/Ba’ names:

Ratings Profile (Annual Report)

‘BB’ names (or ‘Ba’ names in Moody’s nomenclature) are the better rated high yield credits, and present less of a probability of default. The fund contains a 32% bucket for BB names and even has some investment-grade bonds.

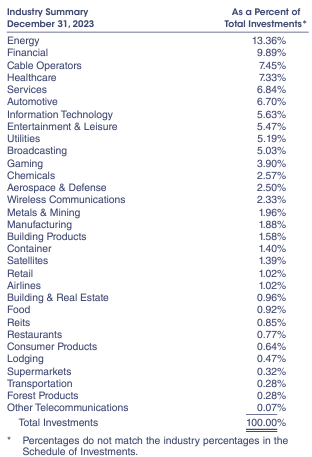

From a sectoral standpoint the CEF is focused on a sector which has greatly deleveraged in the past 3 years, and now sees Debt/EBITDA metrics of 1.5x on average:

Sectors (Annual Report)

We are talking about Energy here, which makes up 13.3% of this fund. We like ‘Energy’ as a sector for debt holders, with the majority of the companies in the space understanding the importance of a healthy balance sheet.

What you should expect from HYB going forward

The CEF will not be able to have an exciting dividend yield until risk free rates are lower, thus expect a rough 7% dividend yield here. Furthermore, the ‘easy’ narrowing of the discount to NAV has already occurred, with the CEF now squarely in the middle of its historic range. The discount will only narrow when rates are lower. We saw this clearly in 2020/2021 when the CEF was trading flat to NAV in a low-interest rate environment.

From a risk/drawdown perspective, the fund will only suffer from credit spread widening going forward (macro view on peak rates from our end). Given the conservative portfolio build, we expect a rough -10% drawdown here in a risk-off environment.

HYB is therefore an unexciting CEF going forward, and will only become appealing once the Fed starts lowering rates or the discount to NAV widens out again without merit.

Conclusion

HYB is a fixed income closed-end fund. The vehicle has been in the market for a long time and runs a conservative portfolio with a 30% leverage ratio on top. The CEF has been hampered by the high risk free rates, obtaining its leverage via a bank facility priced based on SOFR. In our last piece, we liked the entry point in the fund based on its very wide discount to NAV, a discount which has now narrowed to its historic range. With higher for longer rates, the CEF has experienced a narrowing in its net interest margin, with its dividend yield now at only 6.7%. We no longer find the current pricing appealing and think the fund will not make any significant headway until the Fed starts cutting rates. We own the name and are holding and DRIP-ing at the current price levels.

Read the full article here