Co-authored with Hidden Opportunities.

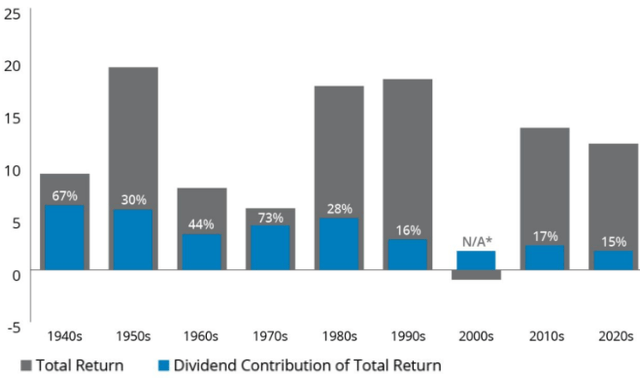

The laws of physics are difficult to escape in our everyday lives. According to Newton’s third law of motion, for every action, there is an equal and opposite reaction. As a baseball catcher positioned behind the batter, if you extend your hand to catch a ball traveling at +95 mph (ca. 153 km/h), the ball comes to an immediate stop, transferring its momentum and force into your hand. Without a mitt, you would definitely feel the impact and strain on your hand.

A similar principle is applicable in the world of investments as well. When investors make strategic decisions to buy income-generating assets like dividend stocks, preferred shares, or bonds, they are taking action to secure stable returns. This proactive action results in a predictable reaction in the form of a steady stream of income that counterbalances market volatility and uncertainty. We have seen this in action through the consistency and significance of the contribution of dividends towards total returns across economic variability.

Hartford Funds

Similar to the force you exert on a fast-moving baseball to counter its momentum, we can use the force of dividends to balance the uncertainties that shake the financial markets. Without further ado, let us look at two forces at our disposal to bring stability to our portfolios.

Pick #1: HR – Yield 7.1%

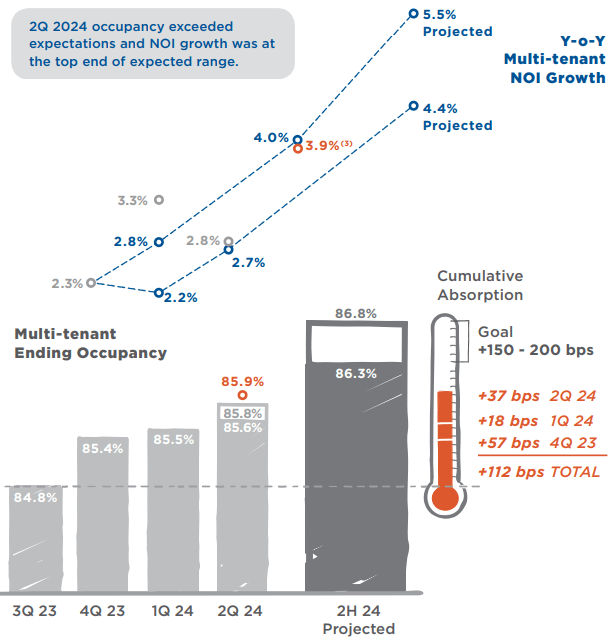

Healthcare Realty Trust Incorporated (HR) is a MOB (Medical Office Building) focused REIT that owns and operates a portfolio of 673 properties, primarily located around market-leading hospital campuses. HR reported its Q2 2024 earnings on August 2. It delivered FFO/share of $0.38, adequately covering its $0.31/share quarterly dividend, and NOI growth (Net Operating Income) exceeding expectations and arriving at the top end of the guidance range. The REIT projects YoY NOI growth to be between 4.5% — 5.5% in 2H 2024. Source.

Q2 Investor Presentation

Based on the strong execution in 1H 2024, the REIT has increased its full-year FFO guidance range midpoint by $0.005/share and mentioned that it would have been $0.01/share more if they didn’t have the Steward revenue reserve. Let us dive into the specifics of the earnings report.

1. Strong Leasing Activity

HR reported strong leasing trends during Q2, with over 400,000 sq ft (3.72 ha) of new leases signed for the fourth consecutive quarter. As per management comments, the tenant’s top-line and operating margins continue to improve, and providers are seeing strong outpatient volume. With limited new supply and rising demand, HR expects tailwinds to lease momentum. During Q2, HR’s new lease pipeline has reached a record 1.9 million sq ft, providing visibility into activity in upcoming quarters. The company expects leasing momentum to remain strong in 2H 2024 and into FY 2025.

2. High Occupancy Levels

HR reported strong retention rates in Q2 – that has the benefit of avoiding lost rent from downtime and also avoiding investments to re-lease a vacant space. During the quarter, the REIT reported its second consecutive quarter of occupancy above 85%, with the metric rising to 85.5% from 79.3% last year.

Management has projected 2H 2024 occupancy to be ~87% and expects this to be an early indication of their position to reach 90% occupancy in the upcoming years.

3. Strong NOI Growth

Due to the combination of strong occupancy gains and controlled expenses, HR reported higher NOI growth than expected. Without the Stewart Reserve, HR’s same-store NOI grew 3.5% YoY in Q2, and total multi-tenant NOI grew 3.9% YoY, both at the high end of the guidance range. This strong 1H 2024 momentum has increased management’s confidence in achieving YoY NOI growth to ~5% in the second half.

4. Fully Covered Dividend

When discussing HR in past quarters, we have mentioned how the REIT’s dividends aren’t covered yet, but they will be as the acquisition with HTA continues to become accretive. Management had initially guided FY 2025 to be the year with covered dividends, but we saw results of the accomplishment ahead of schedule. HR’s $0.38/share FFO for Q2 adequately covers the $0.31/share quarterly dividend. We note that the FFO calculation included the Steward reserve revenue.

For FY 2024, HR expects normalized FFO between $1.53 — $1.55/share, placing its annual dividend at a respectable 79% payout ratio.

5. Share Repurchases

HR’s JV with KKR & Co. has been highly beneficial for the REIT, injecting much-needed liquidity into its balance sheet. The JV contributions and asset sales generated $400 million of proceeds YTD. For the full year, HR expects over $1 billion in total JV and asset sale proceeds, to fund $200 million in planned capital commitments and $800 million of debt settlements and share buybacks. Notably, HR repurchased $295 million of its common stock during Q2 at a 7.5% cap rate, while the JV contributions and asset sales were at a 6.6% cap rate. This 90 bps positive spread makes it a highly accretive transaction. It is like selling a 6.6% yielding investment to buy a 7.5% yield, automatically resulting in greater earnings. Management expects to continue making accretive share repurchases below NAV.

6. Balance Sheet Health

HR ended Q2 with a leverage ratio of 6.4x, including planned debt repayments, which is expected to settle its $250 million term loan maturing in July 2025. Less than $300 million of debt maturing in 2025 is left outstanding. HR expects to end FY 2024 with lower leverage and an improved dividend payout ratio.

Overall, HR continues to post strong operating results, and its dividend coverage improves with each passing quarter. With a portfolio of recession-resistant MOBs occupied by credit-worthy physician tenants, HR is well-positioned to deliver growing income to shareholders in the years ahead.

Pick #2: BTI – Yield 8.2%

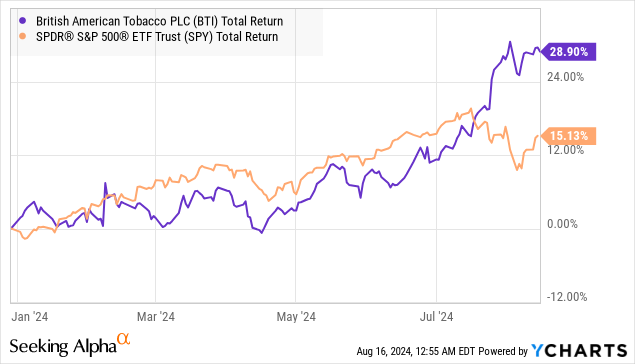

The rotation into value stocks is working well for British American Tobacco p.l.c (BTI) (which will be referred to as BAT in this article), the largest global tobacco company. BAT’s common stock is ~24% above its bottom, and this is only the beginning of what the undervalued tobacco leader can deliver to shareholders.

Note:

-

BAT is a U.K. corporation that pays qualified dividends to U.S. shareholders.

-

The dividends are declared and paid in GBP, and U.S. investors will receive an amount that varies based on USD-GBP conversion rates.

-

The U.K. does not withhold taxes on dividends paid to international investors.

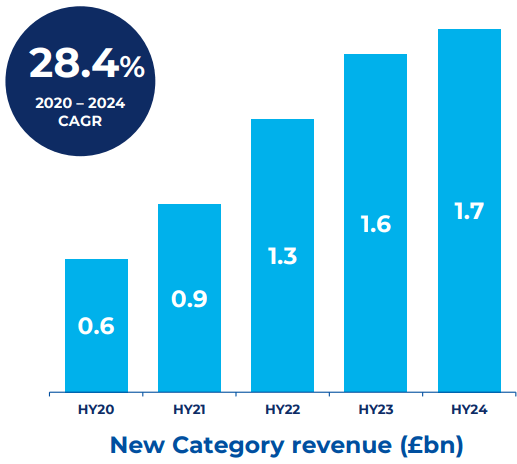

BAT is leading the Big Tobacco peer group in its transition to a smokeless future. During 1H 2024, the company reported an addition of 1.4 million smokeless product consumers to a total of 26.4 million. At £1.7 billion for 1H 2024, BAT’s new category segment represents 17.9% of the group revenue, reflecting a 28.4% CAGR since 2020. During the first half, new category growth was driven by the nicotine product Velo. Source.

1H 2024 Investor Presentation

E-cigarette brand Vuse continues to maintain market leadership with a 40.9% value share in leading markets during the first half of the fiscal year. Smokeless products constituted 20% of total U.S. revenues during 1H 2024.

While combustible revenues were lower in the U.S., its effect was cushioned by strong growth in the Americas & Europe and Asia Pacific Middle East & Africa markets. It is noteworthy that BAT’s popular brands like Newport, Lucky Strike, and Natural American Spirit continue to gain value share in the United States. The company’s strong position in developing nations bodes well for this “legacy” segment. Source.

British American Tobacco

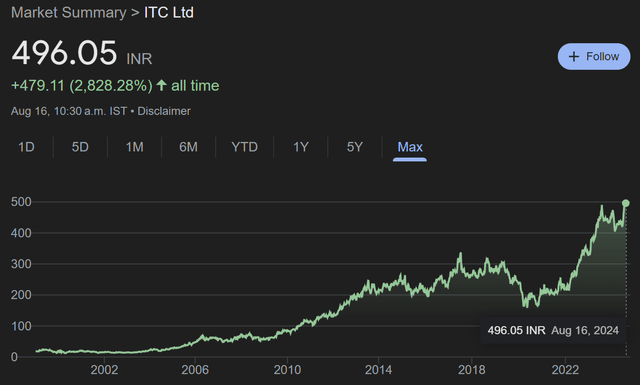

BAT ended 1H 2024 with a strong liquidity position, an average debt maturity of 9.2 years, and a fixed debt profile of 84%. BAT’s balance sheet maintains investment-grade ratings, rated BBB+ by Fitch. The company expects to be within 2.0–2.5x adj. Net Debt/adj. EBITDA by the end of the fiscal year. The Big Tobacco leader still owns 25.5% of ITC Inc., worth $18.6 billion (25% of BAT’s market cap).

Google Finance

Following a modest trim in its ITC stake back in March, the company initiated a significant share repurchase program, intending to buy back £700 million worth of its shares in 2024, and £900 million worth of shares in 2025. As of June 30, 2024, the company has repurchased 15.1 million shares for £366 million.

BAT expects gross capital expenditure in 2024 to increase to ~£600 million, mainly related to ongoing investments to expand its new category portfolio. Management commented that they are on track to meet FY 2024 guidance. Despite the strong YTD rise in market price, BAT is still an undervalued stock, trading at 7.5x forward PE. The company’s current price point presents an 8.2% yield.

Tobacco is an industry where higher prices are easily passed on to consumers and, despite the health effects of combustible products, the government cannot do much in terms of restriction for fear of political consequences. Moreover, efforts to ban have historically led to an increase in illegal shipments of potentially unsafe products manufactured in facilities with poor health standards, making the situation much worse to manage. Tobacco has been inherently ingrained in human society for centuries, and this will continue to be the case for the foreseeable future. It is just the form factor that will change based on preferences, and BAT is already a market leader in what is being defined as the smokeless future for this industry.

Conclusion

In today’s report, we discussed two picks. HR stands to benefit from the constrained supply of medical office buildings and the growing demand for healthcare arising from America’s rapidly aging population. On the other hand, BAT maintains a consumer product line that has proven immunity from recessions or inflationary pressures. Despite the social stigma surrounding the industry, this class of products has deep-rooted ties to the human race and continues to evolve to meet the preferences of new generations. Together, these are solid sources of dividends for our ever-growing income needs.

Our Investing Group closely adopts a strategy we fondly call the Income Method. It involves building a diversified portfolio of income-generating investments to keep the passive income flowing no matter how the market performs from time to time. This is the kind of income stability and reliability you need to enjoy a financial stress-free retirement.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here