International Business Machines Corporation (NYSE:IBM) experienced mixed financial results in the second quarter of 2023. The company saw slight changes in its revenue, with specific segments like software leading the growth, while the infrastructure sector faced some challenges. This dip in the infrastructure domain is attributed to the intricate lifecycle of mainframe operations. Profitability indicators, on the other hand, exhibited a promising direction. Looking forward, IBM remains optimistic about its yearly projections. This article continues the previous piece, diving deeper into IBM’s stock price through technical analysis. The previous article underscored the stock’s pronounced bullish trend, and since then, the price has continued its upward trajectory. In this follow-up, crucial price points and potential opportunities for long-term IBM investors will be explored.

IBM Journey From Software Surges to AI Dominance

In the second quarter of 2023, IBM reported a marginal decline in revenue at $15.5 billion, down by 0.4%, though when adjusted for constant currency, there was a slight increase of 0.4%. The software segment was a significant growth driver, with revenue up by 7% (8% at constant currency). Consulting also showed strength, rising 4% (6% at constant currency). However, there was a noticeable dip in the infrastructure sector, which saw a 15% decline (14% at constant currency). On the profitability front, IBM’s Gross Profit Margin under GAAP stood at 54.9%, reflecting a growth of 160 basis points, while its Operating (Non-GAAP) margin was at 55.9%, up by 140 basis points. The Pre-Tax Income Margin under GAAP increased by 180 basis points to 12.9%, although the Operating (Non-GAAP) margin decreased slightly by 70 basis points to 15.5%. Regarding cash flow, IBM generated net cash from operating activities amounting to $2.6 billion for the quarter, a $1.3 billion year-to-year increase. The company’s free cash flow remained stable at $2.1 billion. IBM closed the quarter with a solid $16.3 billion in cash and marketable securities, a jump of $7.5 billion since the end of 2022, while total debt, inclusive of IBM Financing debt, climbed to $57.5 billion. For 2023, IBM maintains its revenue growth expectation of 3% to 5% in constant currency. It foresees a free cash flow of approximately $10.5 billion, marking a yearly growth of over $1 billion.

From the financial data, IBM’s figures depict a firm steadily advancing. The dip in revenue is attributed entirely to the infrastructure segment and the product lifecycle nuances of its mainframe operations. Both the software and consulting sectors demonstrated robust growth, and IBM remains consistent with its full-year projections.

IBM’s robust performance in the software sector is attributed to its Artificial Intelligence (AI) advancements. In its transformative journey, IBM has anchored itself around two revolutionary technologies: hybrid cloud computing and AI. An integral feature of IBM’s operational approach lies in the interconnectedness of its various divisions. For instance, a client seeking to transition their IT setup to a cloud-based model might engage IBM’s consulting division for guidance and implementation. This interaction can stimulate the sales of IBM’s software, particularly the OpenShift container platform developed by Red Hat.

Following the acquisition of Red Hat, OpenShift has achieved an impressive annual recurring revenue of $1.1 billion. However, the benefits of the Red Hat partnership extend beyond this milestone. The collaboration has given rise to a consulting enterprise worth billions of dollars, focusing on Red Hat’s hybrid cloud system.

Concurrently, IBM is charting a parallel trajectory for AI. Through Watsonx, its innovative AI platform designed to aid enterprises in deploying and managing AI models, IBM aims to position itself as a central figure in the AI business landscape. To bolster AI consulting, IBM has inaugurated a “Center of Excellence for Generative AI” within its consulting division, staffed by a team of 1,000 AI experts. This endeavor goes beyond providing cutting-edge AI technology and guiding clients through the ever-evolving tech landscape. With these initiatives, IBM is primed to establish an extensive consulting empire centered around AI, paving the way for a surge in consulting revenues in the coming years.

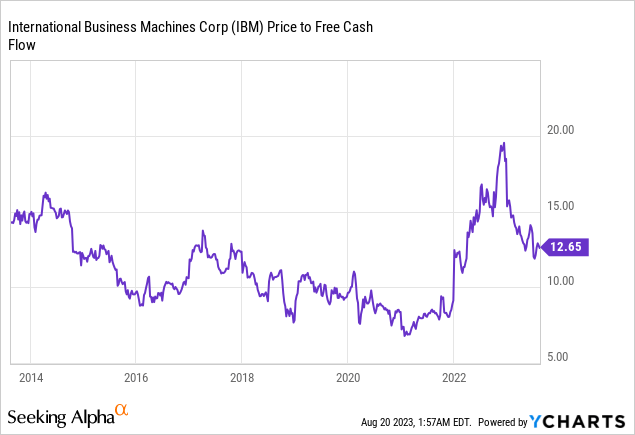

Additionally, after an earnings-driven surge, IBM’s valuation has impressively reached $125 billion. This translates to a price-to-free-cash-flow ratio of just 12. When coupled with a 4.7% dividend yield, it is evident that IBM presents an enticing opportunity for investors to prioritize value and dividends.

Bullish Price Momentum on the Horizon

The technical analysis provided in the previous article indicates a robust bullish outlook based on the yearly and quarterly charts. The yearly candle for 2023 is poised to be distinctly bullish due to the buy signal observed in 2020 and the strong formations in 2021 and 2022. Although there’s a corrective phase visible in the 2023 yearly candle, it is viewed as an additional opportunity for long-term investors to enter the market. The highlighted quarterly chart in the previous discussion showcases a rounding bottom pattern with bullish wicks, indicating robust price action. A breakout above the neckline of this rounding bottom pattern is anticipated to accelerate the ongoing bullish momentum.

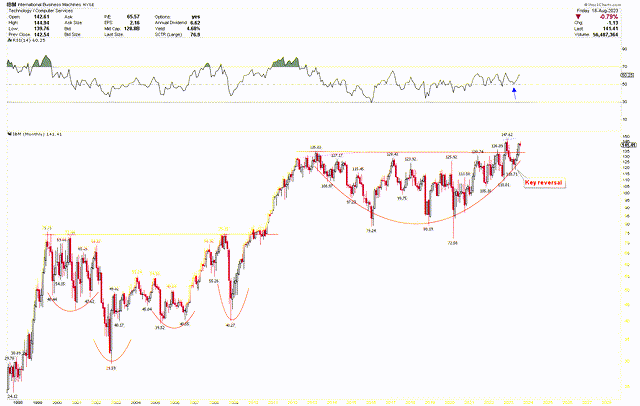

At the moment, the monthly chart below also displays a compelling formation and a strong movement from the breakout point. The significant reversal candle in May 2023 underscores the bullish price action, followed by the subsequent monthly candles in June and July. This impressive momentum highlights market strength and the potential for a breakout. The RSI bottoming around the mid-level of 50 supports the imminent bullish momentum. Market corrections swiftly transform into upward price movements, indicating market resilience. A notable resistance level is marked by the blue dotted line at $148, and a breakthrough at this point is likely to trigger a substantial rally in IBM’s stock price.

IBM Monthly Chart (stockcharts.com)

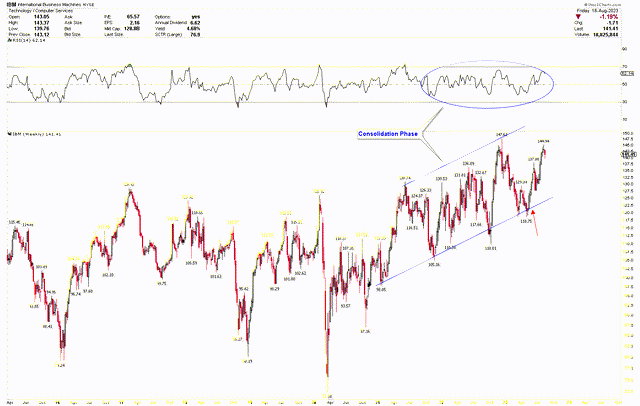

Turning to the weekly chart, the stock price has already met expectations by reaching the resistance point outlined in the previous discussion. Over the past two years, the price action has depicted a consolidation phase, evident in the behavior of the RSI. While short-term strength could materialize, consolidating further within a crucial range is possible before an eventual breakout. The buy signal, highlighted by the red arrow on the chart, emerged due to a double bottom formation, implying a solid foundation for the upcoming bullish move.

IBM Weekly Chart (stockcharts.com)

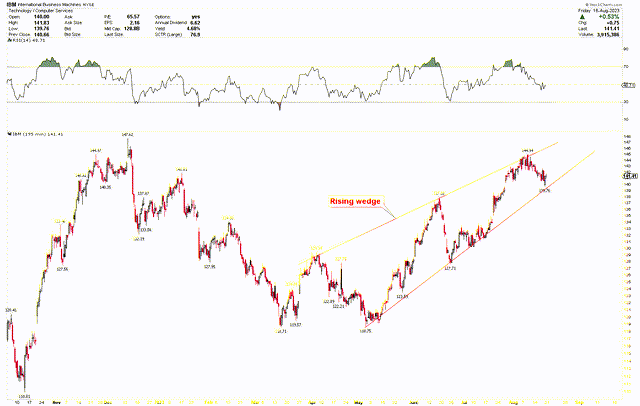

For a deeper understanding of IBM’s stock price resistance, the short-term chart reveals a rising wedge pattern. The price is at the apex of this rising wedge, indicating a pending directional move. As the price has already encountered resistance in the short term, a breakdown from this rising wedge might lead to a corrective phase. However, should prices continue to decline within this range, it would provide another favorable opportunity for long-term investors to enter the market.

IBM 195 min Chart (stockcharts.com)

Market risk

IBM’s dependence on specific sectors, like software and consulting, for its growth might make it vulnerable to fluctuations in market demand and competition. If these sectors experience a sudden drop in development, it could have a pronounced effect on IBM’s revenue and profit margins. The decline in revenue from the infrastructure domain due to the intricacies of mainframe product lifecycles underscores the danger of certain products becoming obsolete. Shifts in technology or evolving customer needs might reduce the demand for current products, affecting income.

The tech environment in which IBM functions is fiercely competitive. With the constant evolution of technology and the rise of new market players, IBM’s market position and ability to set prices might be at risk, compromising its profitability. Additionally, IBM’s financial performance is closely tied to the global economy. Events like economic slumps, recessions, or geopolitical tensions can lead to reduced IT expenditure by companies, which can hit IBM’s bottom line.

From a stock market viewpoint, IBM’s stock is subject to considerable fluctuations and moving sideways. If the stock price doesn’t surpass $148, there might be an increased risk of declining further.

Bottom Line

IBM’s recent performance highlights a company in transformation, leveraging key technological pillars such as hybrid cloud computing and AI. While segments like software and consulting are steering growth, challenges in the infrastructure sector emphasize the need for adaptive strategies. The integration of Red Hat’s capabilities has strengthened IBM’s market position, and the company’s proactive AI endeavors suggest a promising horizon for both innovation and revenue growth. The stock’s technical analysis reveals a potentially bullish trajectory, making IBM an attractive prospect for investors seeking value. However, a dependence on specific growth sectors, the rapid evolution of technology, and global economic fluctuations underscore the importance of vigilance and strategic diversification. Investors and stakeholders should remain cognizant of these dynamics as IBM continues to shape its future in the tech industry. Investors might contemplate acquiring IBM shares and increasing their holdings if corrections occur. A robust upward surge in IBM is anticipated once the market breaches the $148 threshold.

Read the full article here