Immunovant, Inc. (NASDAQ:IMVT) is a pre-revenue clinical-stage biopharmaceutical company developing autoimmune disease therapies. IMVT’s drugs target the neonatal Fc receptor [FcRn] to manage harmful antibodies [IgG] responsible for autoimmune responses. By inhibiting FcRn, IMVT’s therapies facilitate antibody degradation, alleviating disease symptoms. IMVT’s market is considerable, but highly competitive in IgG-mediated conditions. Still, the company’s leading drug candidate, Batoclimab, continues to make progress in its clinical trials for myasthenia gravis [MG], chronic inflammatory demyelinating polyneuropathy [CIDP], Graves’ disease [GD], and thyroid eye disease [TED]. Unfortunately, I suspect most of IMVT’s market cap seems related to its potential as a strategic M&A target. However, with no concrete developments, investors face significant value erosion, while waiting through cash burn. Therefore, I lean bearish on the shares at these levels.

Batoclimab: Business Overview

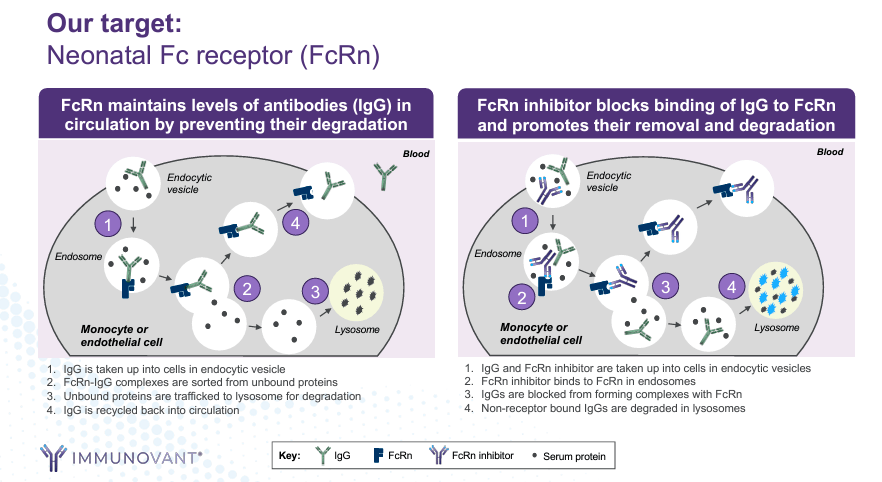

Immunovant was founded in 2018 and is currently based in New York. It’s a clinical-stage biopharmaceutical company focusing on therapies for autoimmune diseases. IMVT’s underlying science addresses autoimmune disease causes by reducing damaging antibodies. To do so, IMVT’s candidates target the neonatal FcRn and reduce pathogenic IgG antibodies that trigger immune responses against healthy tissue. FcRn inhibition prevents FcRn from recycling IgG, allowing antibody degradation in lysosomes. This FcRn inhibition decreases IgG levels, alleviating symptoms and progression of autoimmune conditions.

Source: Corporate Presentation. May 2024.

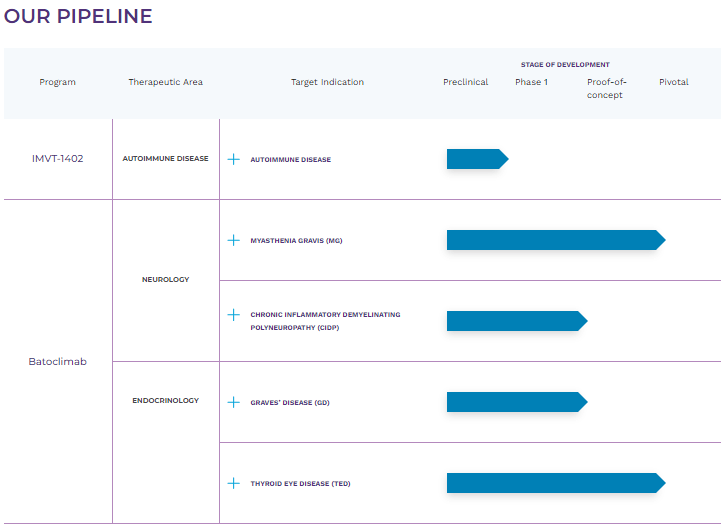

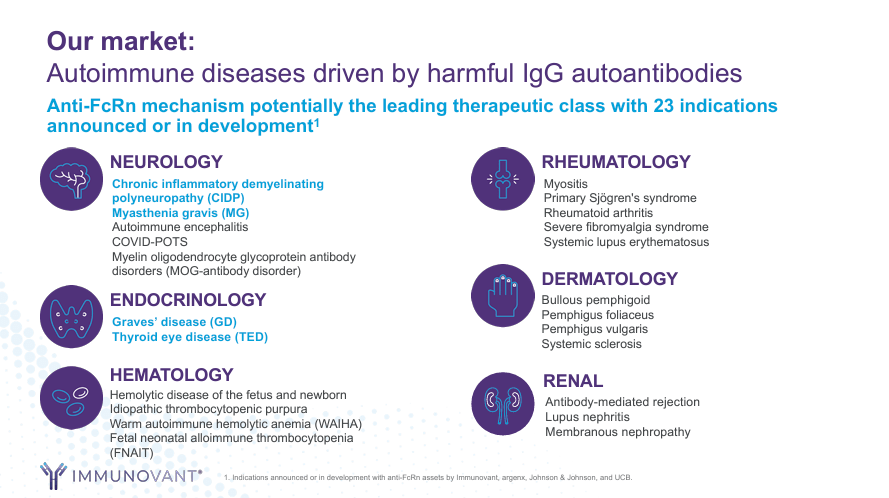

It’s worth noting that over 2 million people suffer from harmful IgG autoantibodies-related disorders. Hence, the anti-FcRn mechanism can benefit a wide range of autoimmune conditions. This is why IMVT has research programs on 23 indications in neurology, endocrinology, hematology, rheumatology, dermatology, and renal diseases. These indications comprise the company’s pipeline, mostly through its leading drug candidate, Batoclimab.

This drug candidate is indicated for neurological conditions like myasthenia gravis [MG] in phase 3 clinical trials and chronic inflammatory demyelinating polyneuropathy [CIDP] in phase 2b. Batoclimab is also indicated in endocrinology for Graves’ disease [GD] in phase 2 and thyroid eye disease [TED] in phase 3. Another IMVT drug that is in preclinical studies is IMVT-1402 for autoimmune disease.

Why IMVT’s Leading Drug Candidate Matters

First of all, MG is a chronic autoimmune disorder that weakens voluntary muscles. Its symptoms start in the eyes, with drooping eyelids and double and blurred vision, progressing to the face, throat, or limbs. Unfortunately, MG has potentially life-threatening respiratory implications when muscles are also affected. MG’s prevalence is 18 cases per 100,000 individuals in the US, so it’s also a sizeable patient population.

Source: Immunovant website.

As for CIDP, this is an autoimmune disease mediated by IgG-damaging antibodies in myelin sheaths. This condition reduces the protective covers around nerve fibers essential for transmitting nerve signals. Since the body’s immune system attacks peripheral nerve fiber nodes, the collateral damage leads to symptoms such as muscle weakness, sensory problems, numbness or tingling, and reflex failure. CIDP progresses over time if left untreated and has a prevalence of around 9 per 100,000 people in the US.

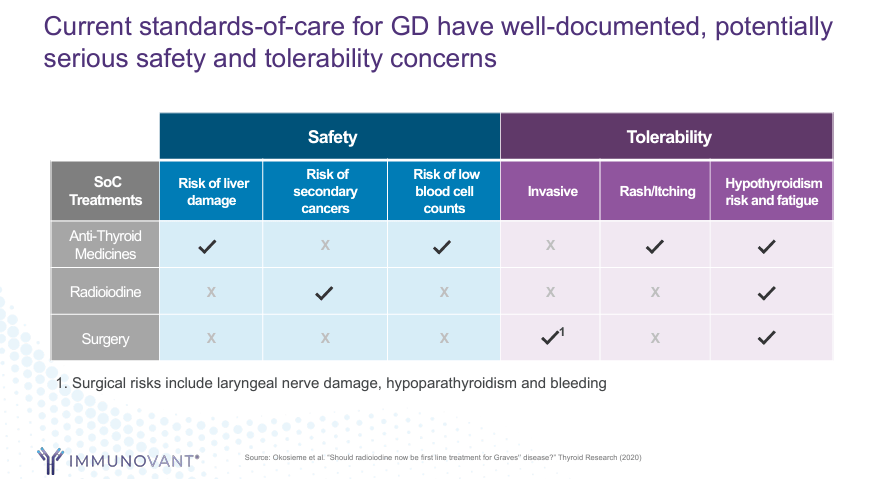

Furthermore, GD is linked to thyroid hormone overproduction mediated by thyroid-stimulating IgG antibodies, causing hyperthyroidism with symptoms such as heat intolerance, weight loss, anxiety, dermopathy, and also ophthalmological manifestations like eye redness or swelling. If left untreated, patients may develop arrhythmias, heart failure, or thyroid storm, which is a life-threatening condition needing immediate medical attention due to high fever, confusion, and coma. Lastly, TED is a variation of GD that affects tissues in the extraocular space, causing eye bulging, tearing, swelling, redness, pain behind the eyes, and double vision or loss of sight. It is produced by IgG autoantibodies that attack the thyroid-stimulating hormone receptor [TSHR]. The prevalence is 10 per 100,000 people in the US.

Source: Corporate Presentation. May 2024.

Consequently, Batoclimab, also known as IMVT-1401, binds and inhibits FcRn. The previously explained conditions benefit from this effect, because it prevents the recycling of IgG antibodies, leading to accelerated degradation and a significant reduction in serum levels. So, I believe IMVT’s leading drug candidate is flexible, as its pipeline suggests, and strategically positions the company in the sector. Since Batoclimab addresses diverse conditions, its TAM is also significant.

Potential and Acquisition Appeal

It’s also worth mentioning that on May 12, 2024, IMVT was identified as underappreciated among the 14 undervalued biotech stocks chosen for its first-in-class and best-in-class anti-FcRns. Then, on May 25, 2024, IMVT was once again considered a potential acquisition target because it is a relatively small biotech that seems strategically positioned for big pharmaceutical players looking to gain an edge in autoimmune diseases. Since biopharma M&A activity increased to 71% in Q1 2024 compared to 2023, it suggests IMVT might be a realistic M&A target.

Source: Corporate Presentation. May 2024.

Moreover, in December 2023, IMVT announced positive initial Batoclimab phase 2 results in GD. They administered 680 mg in the first cohort and obtained a mean IgG reduction of 81% after 12 weeks of therapy, and was seemingly well tolerated. Therefore, I suspect IMVT’s potential value is evident from an M&A perspective, especially for a big pharma player looking to bolster its IP in autoimmune diseases.

Not Worth the Premium: Valuation Analysis

From a valuation perspective, IMVT trades at a respectable $4.0 billion market cap. According to its Q1 2024 financials, most of its assets are in cash and equivalents, amounting to $635.4 million. It has no financial debt, only operating lease obligations, and $41.3 million in accrued expenses.

Still, I estimate its latest quarterly cash burn was about $59.9 million by adding its CFOs and net CAPEX, which implies a yearly cash burn of roughly $239.6 million. Therefore, its sizeable cash fortress only amounts to 2.7 years of cash runway. While this is healthy in most cases, it’s a concern investors must consider for a company trading at a $4.0 billion valuation. After all, IMVT is essentially eroding its main liquid asset at 37.7% per year, and it won’t generate any revenues in the foreseeable future.

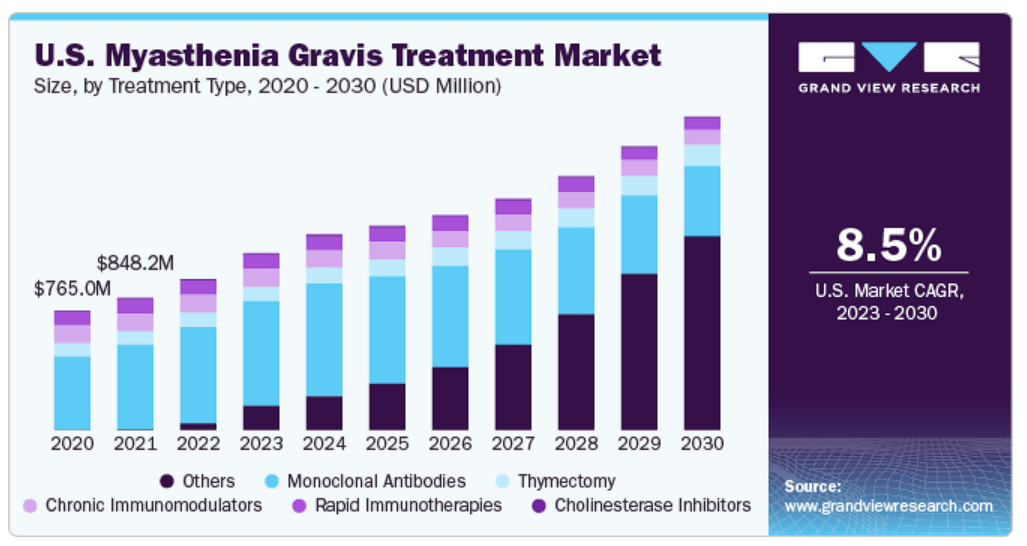

The MG market CAGR is forecasted at 8.5% until 2030. (Source: GrandViewResearch.)

In fact, IMVT’s book value is only $617.8 million, meaning it trades at a P/B of 6.5. This is self-evidently expensive, but compared to its sector’s median P/B multiple of 2.4, it appears overvalued compared to peers. Hence, much of IMVT’s current price seems to be driven by its strategic M&A value, which I believe is somewhat justified. However, it’s hard to envision a significantly higher acquisition price at its present valuation, even if a takeover ultimately occurs. Besides, the longer shareholders wait in anticipation of such an acquisition, the more cash the company will burn, increasing the risk over time.

Lastly, from a competitive standpoint, I must also mention that IMVT’s IgG degraders and FcRn inhibitors are not the only ones being developed. Other biotech companies such as Argenx SE (ARGX), UCB S.A. (OTCPK:UCBJF), and Janssen Pharmaceuticals (JNJ) already have (or are developing) indications for MG, CID, Warm Autoimmune Hemolytic Anemia (WAIHA), and potentially others using similar action mechanisms. I do concede that IMVT’s Batoclimab could ultimately show better efficacy and safety, but it’s key to highlight that this market is riddled with competitors. This, coupled with the relatively hefty cash burn and premium embedded in the shares, nudges me toward a slightly bearish take on IMVT. Hence, I rate the shares as “sell” at these levels.

Caveats: Risk Analysis

Naturally, if a takeover materializes because a pharma giant wants to secure a foothold in this market through IMVT, the shares would probably pop in response to the announcement. Moreover, while I see a considerably challenging competitive environment for IMVT, the aggregate TAM it targets is also quite large.

Further downside potential. (Source: TradingView.)

For context, the MG market was estimated at $2.3 billion in 2023. Similarly, TED is forecasted to reach $417.4 million by 2027, CIDP $3.1 billion by 2031, and WAIHA $1.6 billion by 2033. So IMVT’s aggregate TAM at this time is roughly $7.4 billion. However, when I compare that number to IMVT’s market cap of $4.0 billion, I believe the shares might be overvalued, especially considering it targets highly competitive markets.

Lean Bearish: Conclusion

Overall, IMVT’s degraders are promising, but unfortunately, I don’t think its valuation is justified in light of the competitive space it’s targeting. While I reckon it has a sizeable cash balance to see through its research to a potential FDA approval, the reality is that competition will be fierce even if approved. Moreover, to obtain such approvals, it’ll continue to burn 37.7% of its liquid resources per year, its main tangible asset. Most of IMVT’s value seems to reside on its perceived strategic M&A appeal for pharma giants, which could indeed materialize in an acquisition. However, there’s nothing concrete for now, and while investors await such news, the underlying value erosion is considerable. Hence, I suspect IMVT won’t be a good investment at these price levels.

Read the full article here