International Seaways, Inc. (NYSE:INSW) is one of the largest tanker companies, offering exposure to both crude oil and petroleum products. International Seaways owns and operates a fleet of 85 vessels, including 13 VLCCs, 13 Suezmaxes, five Aframaxes/LR2s, 7 LR1s, and 41 MR tankers. Additionally, it has 6 LR1 newbuilds scheduled for delivery in 2025 and 2026. International Seaways recently purchased 6 MRs, the best performing segment, which were delivered during Q2

I have previously covered International Seaways. Readers should view this as an update to my earlier articles on the company, where I conducted an extensive business overview, reviewed the capital allocation policy, examined management’s past actions, and detailed the investment thesis.

As expected, the stock has performed poorly since the last article, with a decline of around 10%. However, it has once again become the cheapest tanker company among those with reputable management. This is a position it doesn’t deserve and is the main reason I believe it is the tanker company to invest in right now. Moreover, we are in the middle of the low season, and rates have performed much better than I was expecting (except for VLCC rates). I’m not the only one with this opinion, Arctic Securities Research recently increased their rate assumptions.

Arctic Securities Research

Finally, another development that I believe the market hasn’t considered is the possibility that International Seaways could expand their lucrative niche LR1 pool to Ecuador. As mentioned in the first article, International Seaways consistently outperforms their peers in this segment by a huge margin due to their niche operations.

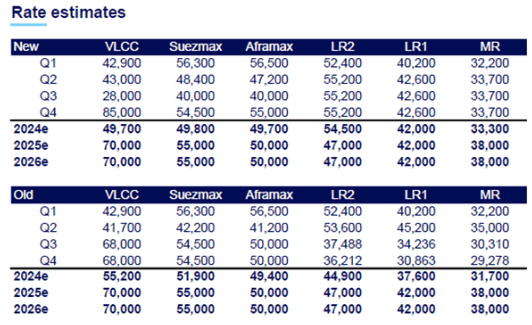

For instance, in Q3, it achieved an impressive $56,300 per day, outperforming competitors such as TORM PLC at $32,641 per day and Hafnia at $30,198 per day.

Tanker Overview

The outlook for both crude and product tankers remains positive and, in my opinion, is the best among the main shipping segments. However, orders have been steadily increasing by about 0.9% per month, and if this trend continues for many more months, it could endanger the bull market a few years down the road.

Another factor to consider is a possible tightening of dark fleet sanctions. Last week, a Hafnia LR1 and a shadow VLCC collided, resulting in a fire on both ships. This incident could increase the pressure to control the dark fleet from both Iran and Russia. If more vessels are sanctioned and there are stricter controls, this will be very positive for rates as supply will be reduced.

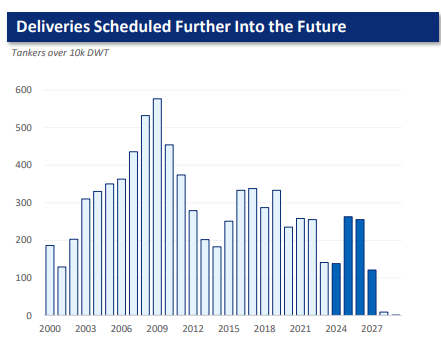

In the short term, supply is scarce, with 2024 expected to see the fewest deliveries since 2021.

Tanker deliveries (INSW Q1 Presentation)

Regarding demand, it remains resilient, and OPEC plans a gradual unwinding of production cuts. However, demand is lacking in certain segments, as evidenced by the low VLCC rates. Another factor affecting demand is the disruption in the Red Sea, especially for products. Last week, Israel attacked Yemen for the first time, and there is no clear resolution in sight.

Financial Position & Stock Valuation

INSW Q1 Presentation

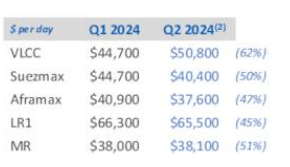

International Seaways’ financial position continues to be rock solid, with outstanding earnings generation and operational performance. Given the Q1 guidance, the rates’ evolution since then, and the recently acquired MR, I expect EPS to be between $2.25 and $2.50, with a dividend slightly below $1.50, representing an 11% yield. Earnings and yield should increase heading into Q4, when the strong season usually begins.

Rates (INSW Q1 Presentation)

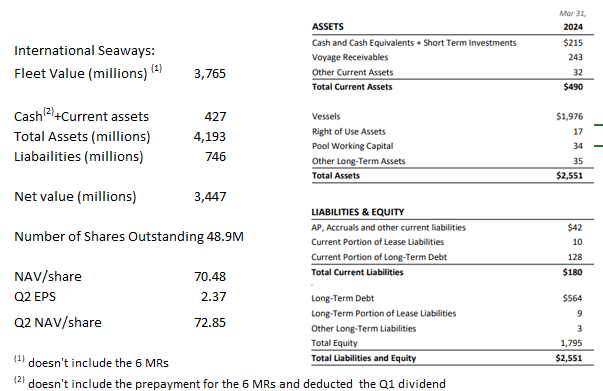

Based on Arctic Securities’ asset values, Q1 company information, and the mid-range of my earnings estimates, the NAV for Q2 is expected to be around $72.50. This suggests that International Seaways was recently trading at 0.75 times NAV, a significant discount compared to most reputable peers, which are trading at or above NAV.

NAV Calculation (Author & INSW Q1 Presentation)

Given International Seaways’ outstanding operational performance, interesting fleet composition, good capital allocation, and correct management, I don’t believe this discount is justified. The stock should trade closer to NAV, offering a potential upside of around 30%, making International Seaways the most interesting tanker company among those with reputable management.

Moreover, if management establishes a clear dividend policy, ideally paying out above 75% of EPS, and stops issuing shares below NAV to acquire ships, the company could trade at a premium valuation like some peers. I believe that with the recent improvement in relations with Fredriksen, both of these outcomes could become a reality by the end of the year or early 2025.

Risk

The company specific main risk is management’s possible desire to expand the fleet. So far, they have pursued very selective growth; however, they paid 15% of the cost of the recently acquired MRs in shares. They will issue fewer than one million shares, but issuing shares below NAV with such low leverage doesn’t make financial sense and has very poor optics. If they continue this practice, it will be a clear negative for the company.

Finally, a more general risk is demand destruction. Smaller ships have been outperforming larger ships for several months. If demand deteriorates further, all rates could be impacted.

Conclusion

International Seaways continues to stand out for its operational performance. However, management has the ability to boost the stock to a premium valuation. With straightforward actions and a clear dividend policy, the stock should re-rate higher.

Currently, it is trading as the cheapest tanker company, excluding Tsakos Energy (TEN), a position it does not deserve. This is the main reason I believe International Seaways is the tanker company to invest in, with around 30% upside potential.

The main risk is if management pursues aggressive fleet expansion at current elevated prices, especially if they continue to issue shares below NAV. Such actions could undermine the stock’s valuation and investor confidence. Additionally, broader market risks, including demand destruction and geopolitical uncertainties, could impact the tanker sector.

Read the full article here