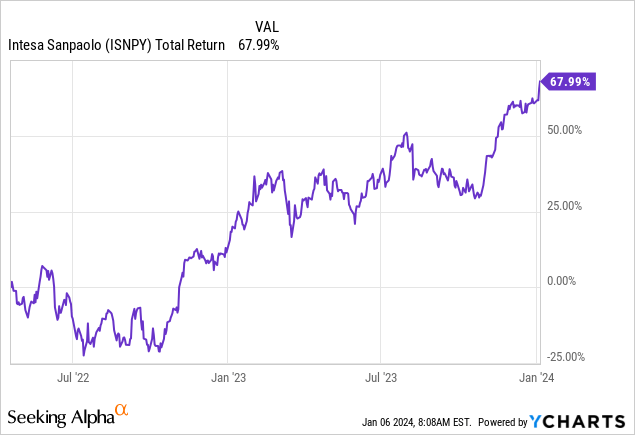

Italian bank Intesa Sanpaolo S.p.A. (OTCPK:ISNPY)(OTCPK:IITSF) has performed strongly since I first covered it in early 2022. The ADSs have returned almost 70% in that time, justifying the initial Buy rating thanks to a surge in profitability on the back of higher interest rates and strong credit quality.

Where we go from here is an interesting question. Intesa stock has since re-rated up to around the 1x tangible book value per share mark, delivering the valuation multiple expansion I was looking for last time. While the bank’s current profitability more than supports this, I am wary of the fact that not many European banks have gone beyond that valuation in recent times. Still, capital returns potential does remain attractive here – and with the dividend yield topping 10% and management pointing to buybacks on top I maintain my Buy rating on the stock.

A Bank Transformed

One of Intesa Sanpaolo’s key advantages is its deposit base, with the bank reporting around €400 billion in low-cost current account deposits as of Q3. As I mentioned last time, this ultra-cheap funding source was largely negated in the zero/negative interest rate environment that characterized the Eurozone until H2 2022.

Furthermore, the bank was also grappling with huge levels of bad debt for much of the 2010s. Gross non-performing loan (“NPL”) exposure was an incredible €60 billion ten years ago, equal to around 16% of total loans to customers. With net interest income (“NII”) squeezed by low rates and billions being set aside to cover bad debt, Intesa’s return on tangible equity (“ROTE”) was barely in the mid-single-digit area.

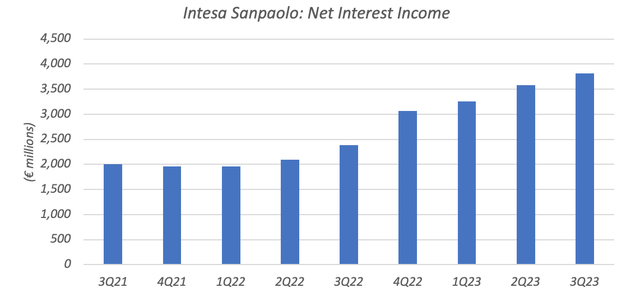

With both of these past issues now tailwinds, the bank has been transformed. Interest rates have risen sharply since my 2022 article, leading to a surge in NII as the bank is now able to realize the full benefits of its funding base. Intesa generated NII of €3.8 billion in Q3 2023, nearly double the levels it was earning when I first covered it:

Data Source: Intesa Sanpaolo Quarterly Results Releases

Perhaps more impressively, quarterly operating expenses have remained broadly flat in that time despite the inflationary backdrop. OpEx clocked in at around €2.65 billion in Q3 2023, only €10 million higher than the prior-year period. With fee and insurance income roughly flat year-on-year, pre-provision earnings have likewise surged, coming in at €3.7 billion in Q3 versus €2.4 billion in the prior-year period.

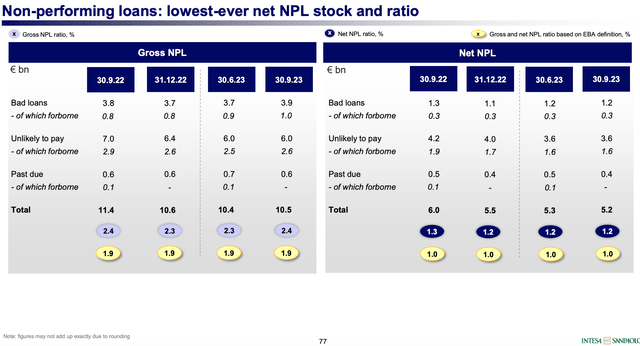

The bank has also made huge strides in reducing NPLs. Gross NPL exposure was around €10.5 billion in Q3, equal to 2.4% of total loans to customers. Like most banks, credit quality at Intesa has held up much better than most would have imagined: the NPL ratio remained flat year-on-year in Q3, with the overall gross stock of NPLs down around €0.9 billion in that time.

Source: Intesa Sanpaolo Q3 Results Presentation

This has driven very low provisioning expenses at the bank, with Intesa setting aside just over €900 million over the first three quarters of last year. That works out to an annualized cost of risk (“COR”) of just 28bps, comfortably below management’s 35-40bps target across the cycle.

All of this has contributed to a drastic improvement in Intesa’s profitability, with Q3 net income of €1.9 billion mapping to a ROTE of circa 15%, well above the single-digit levels it was earning in the mid/late 2010s.

Net Income Still Seen Growing

European bank earnings face a difficult task to grow from here. Rate hikes look done for one, with increased pass-through to depositors putting downward pressure on NII. Credit quality will probably become more of a headwind than a tailwind, too, for the simple reason it has been at very supportive levels recently.

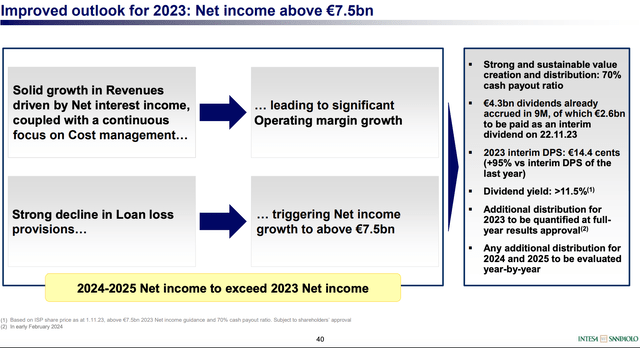

Interestingly, management actually expects net income to grow in 2024 and 2025 from the €7.5 billion-plus it expects the bank to earn in 2023. Modest revenue growth, absolute reduction in operating expenses and flattish cost of risk are seen driving this.

Source: Investor Sanpaolo Q3 2023 Results Presentation

This looks ambitious to me but there are a few supporting points to bear in mind. Firstly, guidance for NII growth will at least see support from the replicating portfolio. As I have commented in other recent European bank articles, readers can essentially view this as being like a bond portfolio that the bank earns spread income on. The value of Intesa’s replicating portfolio is currently around €160 billion with a duration of four years. Because most of this was invested when interest rates were very low, the bank was only earning a blended yield of 72bps at the end of Q3. Around €2.5 billion is rolling off each month, which the bank can reinvest at much higher yields today given prevailing interest rates. This will support NII going forward:

So the trend is absolutely in line with our expectation. And I mean, you can make your own calculation, but obviously, the it is €30 billion per year that is being rolled over and the difference in the yield from the existing portfolio to the new hedges that are in the four-year duration area, so it is about 3.2%, 3.3% of new investments will lead to an increased contribution to net interest margin, which is in the region of €1 billion per year.

Stefano Del Punta, CFO Intesa Sanpaolo, Q3 Earnings Call

Credit quality is probably the wild card. Although the bank has done great work in getting its NPL ratio (~2.4%) and Stage 2 ratio (~8%) down to very respectable levels, a sub-40bps through-the-cycle COR target is ambitious. One thing I would say in the bank’s favor is that residential mortgages are now a larger share of its loan book than in the past. Those loans accounted for around 27% of loans to customers in Q3, up around 8ppt compared to the mid-2010s. These loans are relatively lower risk and will help drive a structurally lower COR at the bank versus historical levels.

Capital Returns Potential Remains Attractive

While net income growth this year and next looks ambitious, capital returns potential remains compelling even on relatively flat earnings. The bank targets a 70% dividend payout ratio of net income, which on €7.5 billion maps to at least €5.25 billion in cash terms. Call it €0.29 per share (~$1.92 per ‘ISNPY’ ADS). With the ADSs trading for $18.34 as I type, investors are still looking at a 10%-plus gross dividend yield. Management plans additional returns on top by way of buybacks, with the level to be determined alongside full-year 2023 results:

In terms of the way in which we can distribute, so adding to 70% payout ratio, I told to my Board of Directors that my intention is to proceed with share buyback, so that is the proposal that it is likely that I will submit to the Board of Directors when we will approve the year-end figures.

Carlo Messina – CEO Intesa Sanpaolo, Q3 Earnings Call

Investors could be looking at a mid-teens annual shareholder yield over the next couple of years. Given that, I continue to view these shares as attractive. The current share price works out to a valuation of around 1x tangible book value per share. That seems to be about the limit that European banks have commanded in recent times. So despite guidance of a circa 15% ROTE through 2025, I would be wary about baking in further upside from multiple expansion. Even so, with buybacks and dividends running at a strong double-digit yield, these shares still hold enough appeal even on a flat valuation, and I maintain my Buy rating on the stock

Risks

I see the two main risks as coming to NII and credit quality. While Intesa does have nice non-interest sources of revenue, a return to the chronically low interest rate environment of recent years would seriously dent its profitability over time. Similarly, while management has likely pulled off a structural reduction in Intesa’s COR, it can’t control the macro environment, and that will need to remain somewhat benign for it to achieve its 2024-2025 net income growth targets.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here