Intesa Sanpaolo (OTCPK:ISNPY) has obtained a fascinating stock performance over the last year. With favorable macroeconomic conditions, the bank has been well-positioned to capitalize on these scenarios. Intesa is a bank that over the last twelve months has achieved €23.748 billion in revenue, and €8.069 billion in net income, while simultaneously offering a dividend yield of 8.13% and a targeted payout ratio of 70% over the next two fiscal years. In this analysis, I will go through the Intesa business, financials, their new Neo Bank, valuation, and outlook to decide whether this stock continues to be a buy after its accelerated price appreciation over the last year.

Intesa Sanpaolo Business Overview

Intesa Sanpaolo was the result of a merger of two Italian banks; Banca Intesa and Sanpaolo IMI. From there, a diversified bank was created and as of Q1, they operate within seven business units.

1. Banca dei Territory (44% of revenue)

2. IMI Corporate & Investment Banking (15% of revenue)

3. Private Banking (13% of revenue)

4. International Subsidiary Banks (12% of revenue)

5. Insurance (7% of revenue)

6. Corporate Centre (7% of revenue)

7. Asset Management (4% of revenue)

Banca dei Territory represents the core retail banking to individuals and SMEs, while the rest of the segments have a self-explanatory business name. In the Q1 presentation, Intesa pointed out that they will consolidate their Private Banking, Asset Management, and Insurance divisions into a single oversight unit named the Wealth Management Division. Together, this new division will represent 24% of the most recent revenue quarterly revenue achieved.

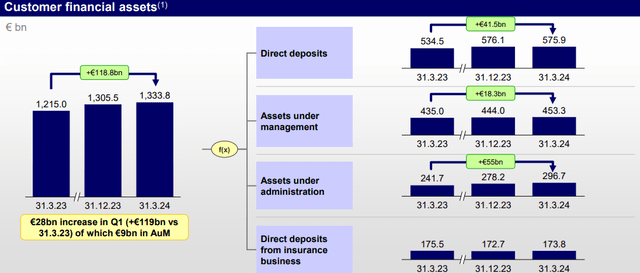

Intesa Q1 2024 Presentation

Due to its strong position in wealth management and retail banking, the bank has been able to accumulate €1.334 billion in customer assets. With this, Intesa can diversify well its asset base from direct deposits and assets under management/administration without exhibiting a significant difference between the two. The previous, also helps the bank to provide a higher balance between interest income and non-interest income.

At the same time, Intesa is not a solely focused Italian player. The company has 934 branches abroad, and in 2023, €5.85 billion or 23.3% of the revenue came from Europe and the Rest of the World.

Based on SP Global, Intesa is the #13 largest bank in Europe and #1 in Italy in terms of total assets, consequently, they stand #15 in terms of AUM in Europe and #2 in Italy after UniCredit (OTCPK:UNCFF).

ISNPY Financial Evolution

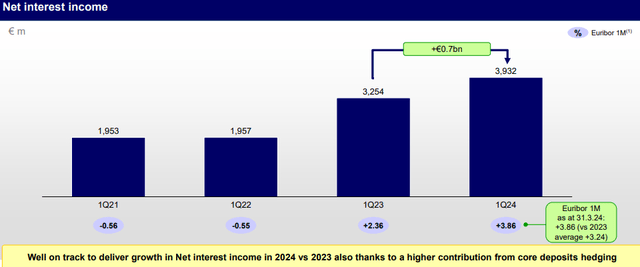

Intesa Q1 2024 Presentation

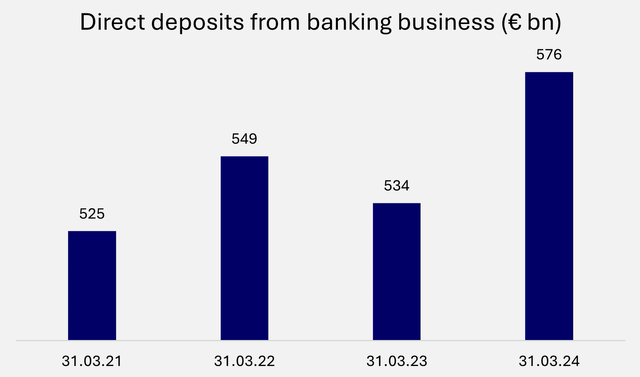

Intesa Sanpaolo has been a clear winner of rate hikes, showing a strong resiliency in its cheap core deposit base by even increasing them in periods when clients are induced to transfer funds to higher-yielding products. This in consequence has brought net interest income to soar. The last NII reading was €3,932 billion which represents a 41.7% CAGR from Q1 2022. At the same time, the direct deposits from the banking business saw a slight decrease of -2.7% from Q1 2022 to Q1 2023, but soared again 7.9% in Q1 of 2024.

Intesa Q1 2024

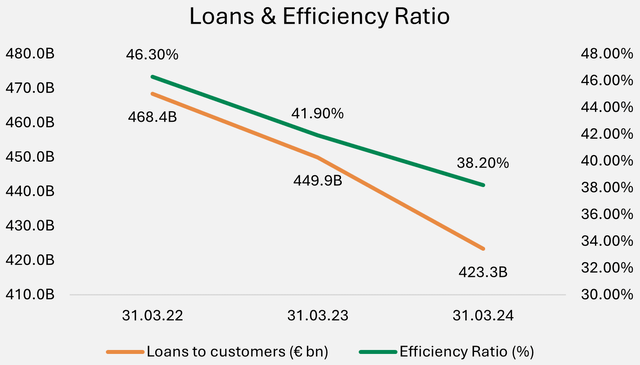

Of course, not everything is sunshine and rainbows for Intesa. The increase in rates caused the loan portfolio to decline due to the lower demand of customers to borrow at higher rates, as seen in the graph below. From Q1 2022 to Q1 of 2024 the loans to customers declined by €45 billion. Despite this drop in loans, net interest income did increase due to higher margins, and ultimately that’s the metric that matters the most. Also, the company has been successful in allowing income to grow higher than its costs as their efficiency ratio has dropped 8.1% points over the last two years.

Intesa Q1 24 23 22

Isybank – Intesa’s New Digital Bank

With rising adoption from depositors to fintech alternatives such as Revolut and N26 in Europe. Intesa didn’t remain with the hands crossed and launched Isybank last year. So far, the majority of their customers (~350,000) migrated from Intesa Sanpaolo to Isybank, while more than 90,000 are new customers of the bank. In total, they sum ~€2.1 billion in customer deposits and the company plans to add ~€200 million in gross income once the 1 million user mark is hit in 2025.

There isn’t much information about this in their presentation, but from what I can see, their customer acquisition cost from new clients is elevated. Currently, they are given referral offers of €50 for making an Amazon purchase with their debit card, and €50 extra if they receive their salary or pension on their Isybank account.

At the same time, the digital bank of UniCredit (OTCPK:UNCRY), Buddy, has significantly more time in the market, and a significantly broader digital presence in terms of YouTube reviews of their products, making the new digital bank of Intesa less innovative.

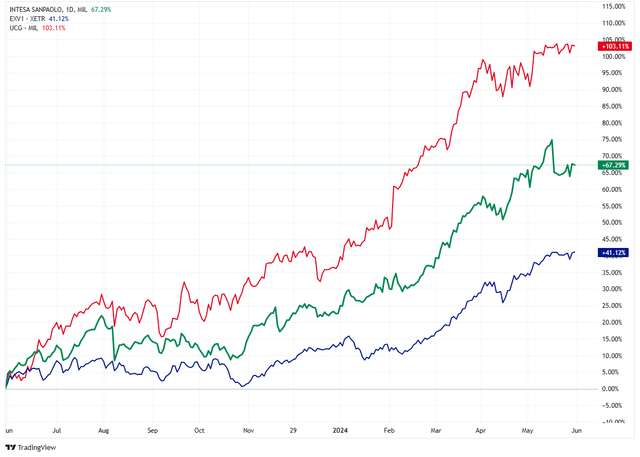

Intesa Stock Price

TradingView

Investing in European banks, particularly the ones in Italy, hasn’t been like a trendy spot to place your money over the past decade. Particularly, with growth outperforming value in most of the time frames. However, the performance of Italian banks over the past year has been extraordinary. In the case of Intesa, for example, the stock has gained 67.3%, which represents an outperformance of 26.17% to its natural benchmark, the STOXX Europe 600 Banks Index. Simultaneously, rival UniCredit has achieved a bagger with a performance of 103.51%, not even including dividend payments.

What drove Intesa’s stock up?

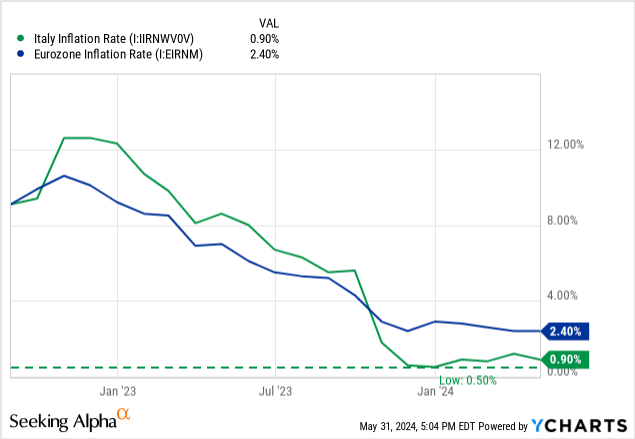

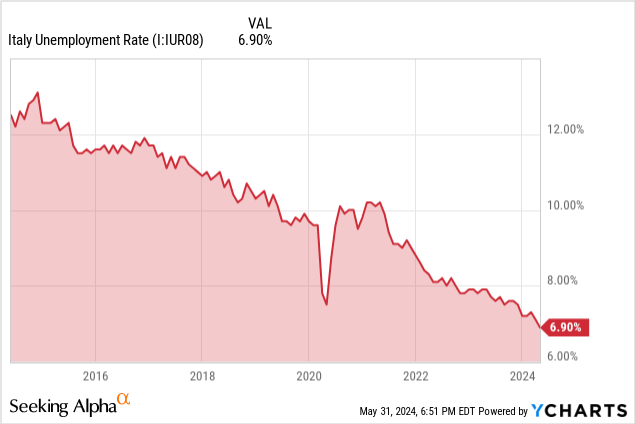

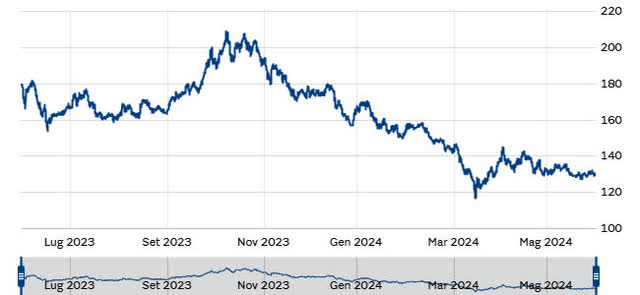

Besides the solid earnings growth of Intesa, the Italian economy has been exhibiting certain tailwinds that ultimately reduce the perceived risk of the expected debt repayments of the loans originated. From a non-exhaustive list these have been positive drivers that led to a general equity rally not only in Intesa but in the Italian index in general.

- Inflation Levels

- Unemployment Rate

- Spread Against German Bonds.

As seen in the image above, the inflation rate in Italy has strongly recovered from an elevated level higher than 12% in 2022, to now sit at 0.90% which falls below the Euro Zone inflation target of 2%. Also, the inflation rate has remained at low readings for a prolonged period now without exhibiting significant volatility.

Next, the unemployment rate in Italy has continued its downward trend and now stands at levels that seemed unachievable 10 years ago.

Finally, the spread between long-term Italian bonds and long-term Germany bonds has massively decreased through the last year making the cost of borrowing for the Italian government cheaper and also bringing lower country-specific risk.

Spread BTP Italia-BUND 10 Years (Il Sole 24)

Intesa Valuation

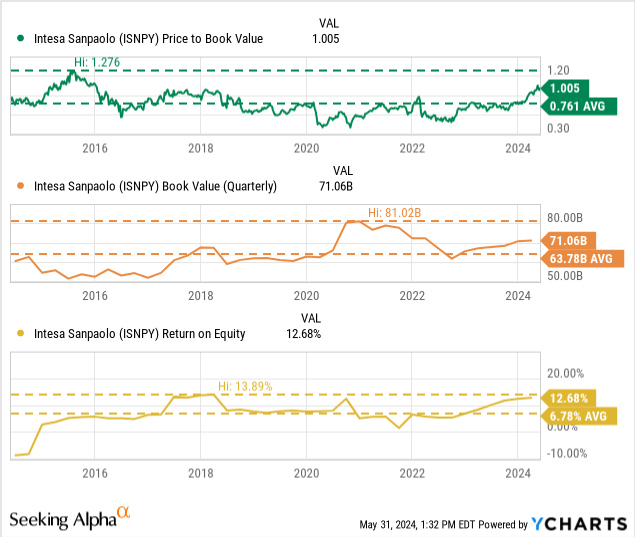

When looking at Intesa in terms of price to book, growth in book value, and return on equity, the following comments could be made.

- Based on their 10-year historical average, the boosted momentum in the stock price made ISNPY to trade above the one-time book value mark after many years. On average the PB multiple has sat at 0.761x, and now is at 1.005x, representing a 32% difference.

- Although the book value of Intesa declined -23.9% from Q4 2024 to Q3 2022, since that quarter, the book value has gained on every release and has recovered 15.3%. At the same time, on a 10-year trajectory, the equity portion of the bank has grown 17.7%.

- The return on equity, which helps justify the PB multiple, has been on the rise at 12.68% and stands close to its 10-year high of 13.89%. Also, the metric sits at twice the historical average, even though this average contains some outliers with quarters of negative net incomes.

Seeking Alpha

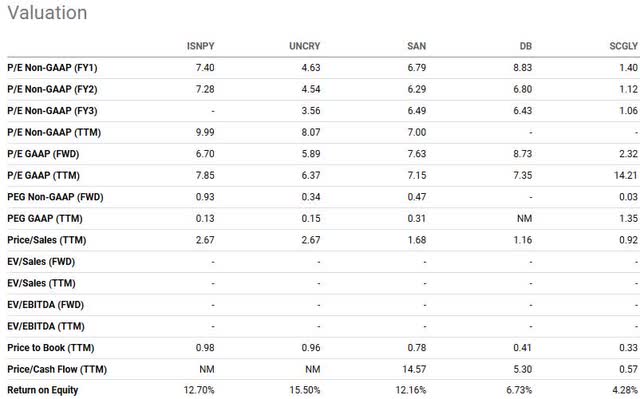

Now, with these rises, Italian banks significantly started to distinguish from other major European banks such as Santander (SAN), Deutsche Bank (DB), and Societe Generale (OTCPK:SCGLY) in terms of evaluating their companies at book value. Of course, this is justified by the higher return on equity that these Italian banks are achieving at 12.70% for Intesa and 15.50% for UniCredit.

Outlook

Based on the outlook and guidance given by the company, the path remains optimistic. Intesa continues to expect a net income higher than €8 billion for the fiscal years 2024 and 2025, which is consistent with the actual elevated levels that are currently being exhibited. At the same time, the company plans to conduct a €1.7 billion share buyback in June, which will still allow them to be well capitalized with a CET1 ratio higher than 14%.

Following, Italian and European banks in general have tightened their credit standards due to concerns about asset quality as rates remain elevated, which is a proactive approach to reduce the potential of loan losses.

General European Union elections are about to be held soon starting on the 6th of June, which are events that drive the volatility in the coming days up to the elections. Therefore, if someone is considering a position in any European stock in the following days, this should be taken into account.

Takeaways

In the end, here we are discussing a cyclical business, which is a bank. Things seem pretty bright for Intesa, and this might be a warning sign to remember that banks have their seasons of prosperity and hardship. The stock price appreciation talks for itself, and I am getting the feeling that I am too late to join the party. Therefore, I will skip this investment despite charming guidance from the company even when accounting for rate drops. Of course, these rate drops could potentially boost asset valuations and help increase the fees obtained from the wealth management division. So, this next policy step is not necessarily negative for all revenue sources.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here