There is somewhat of a case to be made for Invesco (NYSE:IVZ) purely on the basis that its relative valuation compared to the market is at an outlying discount right now and hasn’t been tracking the general market closely since the beginning of 2023. On the other hand, drivers in the market have been pretty narrow, and Invesco fundamentals benefit more from broad-based improvements primarily in the equity environment. We don’t think things are going to work out that well for Invesco over the next 6-12 months due to continued concerns around broad macroeconomic factors, and also due to the fact that with where long-term rates are being priced by the bond market, the secular picture for equities doesn’t look that good. While there might be inflows into fixed income funds to mitigate that, the banking sector and savings deposits are going to win share, with the overall passive shift also being an income and mix problem for Invesco. Not terribly compelling given the ambiguous picture.

Q2 Breakdown and Comments

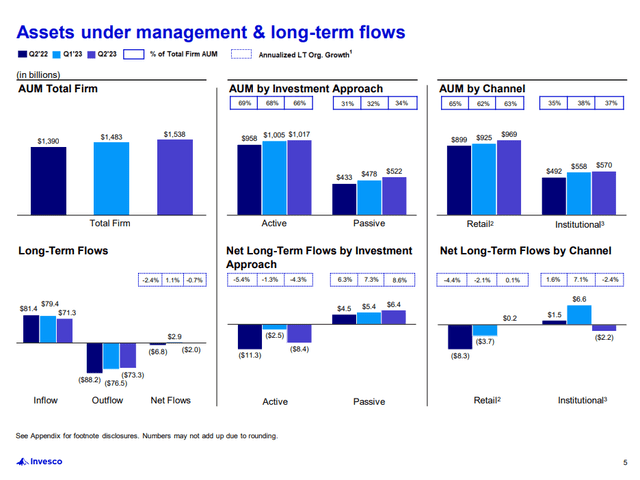

The Q2 breakdown shows slight revenue pressure due to mix effects despite growing AUMs. Reduced performance fees due to poor general asset class performance has not helped either. But primarily, the issues are that there is a shift to passive where Invesco will suffer meaningful mix effects.

By Segment (Q2 2023 Pres)

On top of that, inevitable inflation in the fixed cost structure continues to put pressure on the bottom line.

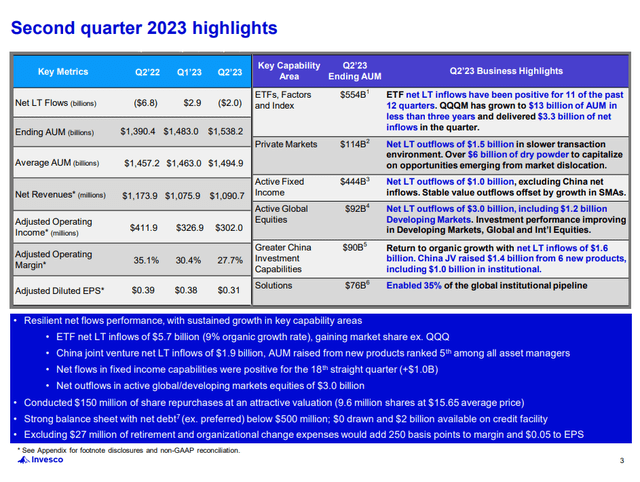

Performance Highlights (Q2 2023 Pres)

It is very likely that since the last quarter performance fees may be on track to improve, as the soft landing narrative has become more prevalent as the consensus view, but we are not sure if this will last for much longer, with the next several Fed meetings offering in our view a high probability of shifting expectations. The reason is that the last leg of inflation could be stubborn. Yes, the China troubles help general commodity deflation ease headline figures, and possibly rent inflation is slowing which is a major component of consumer prices. Still, retaliatory pricing and tit-for-tat dynamics between vendors and customers, as well as between unions, employees and corporations create a stubborn core component that will have to be defeated enough for inflation to fall below the 2%, non-negotiable mark.

Invesco is an indexer and a quasi-indexer in terms of the majority of its asset management strategies, and that means broad based factors like the rate situation matter. We are not certain yet of a soft landing or the arrival of peak rates in time to allow margin to stop a recession.

There are more concerns around the yield curve. Long-term rates are coming up in terms of expectations. This makes sense due to major secular trends like deglobalisation contributing to higher long-term inflation pressure. This could change the dynamics of savers and investors. While passive strategies grow in the mix, AUM could slow in growth if people decide that fixed income allocations are indeed more sensible. The TINA environment is over, and while Invesco has exposure to fixed income and money market funds, they will donate business to banks and their deposit accounts, so a shift away from equities is not a good thing, especially if poor performance accelerates the passive shift, as it always does.

There is also some meaningful ugly exposures in terms of the business mix at Invesco, which will likely see further fund outflows. Both the direct real estate, indirect real estate and China businesses are going to continue to decline, shifting more business to passive funds or to savings options outside of Invesco. For real estate it’s both because of recession risk, long-term rate risk, maturity walls and of course office exposure and the continuing, definite danger of WFH being here to stay. Together these are possibly more than 10% of AUM.

Bottom Line

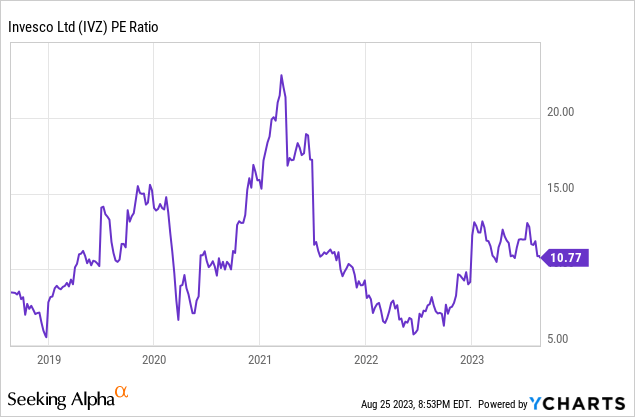

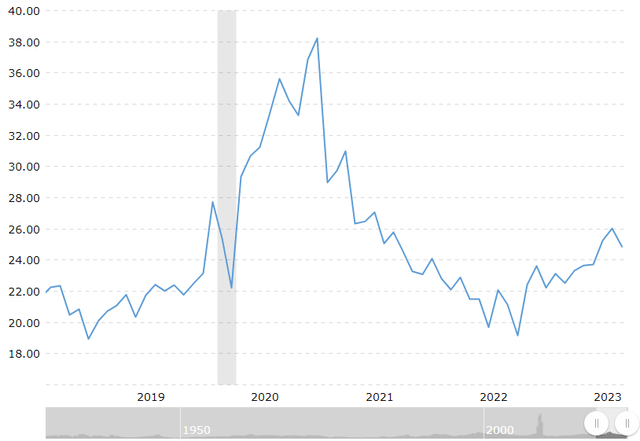

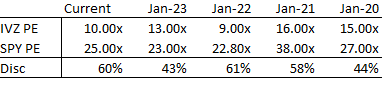

The upside in Invesco is the cheap valuation. 11x is not a lot, even though there are TTM figures and there are continuing margin pressures. Moreover, relative valuation compared to the broader market is also at a historic discount, referring to the charts and the table below.

PE of the SPY (macrotrends.net) Invesco discount in PE to the SPY (VTS)

The problem is that Invesco’s performance doesn’t track proportionately the market as a business, with mix effects being the major reason for differentials to grow permanently. Also, even if there is a relative case for Invesco’s undervaluation, it doesn’t change the headwind-rich business environment and the fact that the broader market may also be overvalued right now.

Plans to improve margins with cost savings initiatives are limited, even in the earnings call the forecasts for their $50 million savings initiative are not going to do much especially as inflation in the fixed costs continue to truck on. The organic problems are meaningful especially if you think that equity markets have jumped the gun by assuming soft landing.

I think investors can be more creative and more safe in the lower-multiple world with picks that are not Invesco.

Read the full article here