Key takeaways

- The fund outperformed its benchmark.

- The fund held up better than its benchmark as both declined during the quarter. Stock selection in the technology, consumer staples, financials and energy sectors contributed to the fund’s outperformance of its index. Stock selection in materials and industrials detracted.

- Small-cap stocks lagged large- cap stocks.

- The US small-cap universe declined in the second quarter, trailing US large-caps as investors appeared to consider the potential negative effects if interest rates stay higher for longer.

- We remain cautious with a balance of defensive stable growth and offensive cyclical growth.

- While the market seems in our view ready for a shift to lower interest rates, we remain cautious and continue to monitor the weight of the evidence for possible changes in interest rates and the economy.

Manager perspective and outlook

Large-cap US equities advanced during the second quarter as investors appeared to continue to process the possibility of a US Federal Reserve (Fed) pivot to easier monetary policy in 2024 and a select group of mega-cap technology stocks rallied on headlines about artificial intelligence.

The US small-cap universe declined during the second quarter, trailing US large-caps, as investors appeared to consider the potential negative effects if the Fed keeps interest rates higher for a longer period.

Since 2022, interest rate increases have slowed the US economy and dampened inflation, although the US labor market has remained healthy. While markets seem in our view ready for a shift to lower interest rates, we remain cautious and continue to monitor data in order to weigh the evidence for or against changes in interest rates and the economy. We scaled back some defensive positioning and introduced more cyclicality to the fund. However, we are aware of potential risks, so we seek to maintain balanced positioning. We see artificial intelligence as a significant technology trend with wide-ranging implications for technology investment, employment and productivity enhancements moving forward.

Portfolio positioning

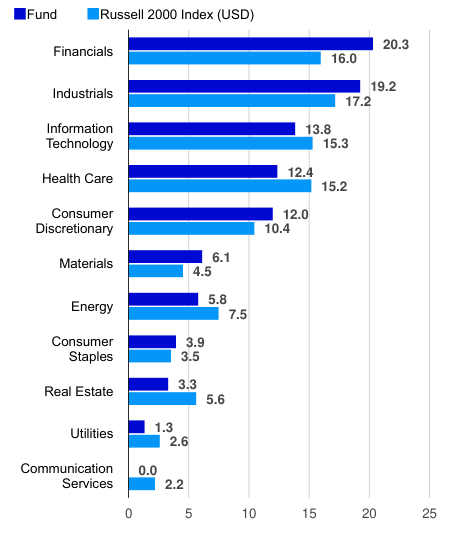

At quarter end, relative to the Russell 2000 Index (RTY), the fund was overweight in financials, industrials, materials and consumer discretionary and underweight in health care, real estate, communication services, energy, technology and utilities. During the quarter, we added to consumer discretionary, consumer staples and materials and reduced industrials, technology and communication services.

In industrials, we added Janus International (JBI) and ICF International (ICFI), and sold Masonite International (DOOR), WillScot Mobile Mini (WSC), Nextracker (NXT) and Alight (ALIT). In financials, we added Bancorp (TBBK), BGC (BGC) and Skyward Specialty Insurance (SKWD) and sold Radian (RDN), Essent (ESNT) and Reinsurance Group of America (RGA). In technology, we added Allegro Microsystems (ALGM), FormFactor (FORM) and Coherent (COHR) and sold Endava (DAVA), Lattice Semiconductor (LSCC), PROS, Blackbaud (BLKB) and PowerSchool (PWSC). In health care, we added ADMA Biologics (ADMA) and sold Cytokinetics (CYTK). In consumer discretionary, we added Modine Manufacturing (MOD) and Arhaus (ARHS) and sold Papa Johns International (PZZA). In energy, we added Antero Resources (AR) and sold Southwestern Energy (SWN). In materials, we added ATI (ATI). In consumer staples, we added Chef’s Warehouse (CHEF).

Second quarter additions:

Janus International supplies products and services to the self-storage industry.

ICF International provides consulting services to federal, state and local governments, electric utilities and commercial markets.

Bancorp is a Delaware-based regional bank and debit payment processor.

BGC is an interdealer broker and electronic trading platform serving the investment banking community.

Skyward Specialty Insurance provides property & casualty, excess & surplus and professional liability insurance.

Allegro Microsystems makes motion and power sensor semiconductors.

FormFactor makes semiconductor testing and measurement technologies.

Coherent provides networking equipment, optics and lasers for industrial, communications, electronics and instrumentation markets.

ADMA Biologics makes immuno-technology plasma-derived therapeutics to treat infectious diseases and manage immunocompromised patients.

Modine Manufacturing makes heating and cooling systems. Arhaus is an omni-channel retailer of premium home furnishings. Antero Resources is an independent oil and natural gas company.

ATI makes high-performance metals, alloys and components for aerospace, defense, energy, auto, electronics, medical and mining.

Chef’s Warehouse is a specialty food distributor serving high-end independent restaurants and specialty retailers in the US and Canada.

Top issuers (% of total net assets)

|

Fund |

Index |

|

|

Tenet Healthcare Corp (THC) |

2.37 |

0.00 |

|

Taylor Morrison Home Corp (TMHC) |

2.04 |

0.22 |

|

Sprouts Farmers Market Inc (SFM) |

2.03 |

0.33 |

|

Summit Materials Inc (SUM) |

1.75 |

0.17 |

|

Piper Sandler Cos (PIPR) |

1.71 |

0.16 |

|

ITT Inc (ITT) |

1.68 |

0.00 |

|

Applied Industrial Technologies Inc (AIT) |

1.66 |

0.29 |

|

Ollie’s Bargain Outlet Holdings Inc (OLLI) |

1.54 |

0.00 |

|

TMX Group Ltd (OTCPK:TMXXF) |

1.52 |

0.00 |

|

Weatherford International PLC (WFRD) |

1.49 |

0.34 |

|

As of 06/30/24. Holdings are subject to change and are not buy/sell recommendations. |

||

Sector breakdown (% of total net assets)

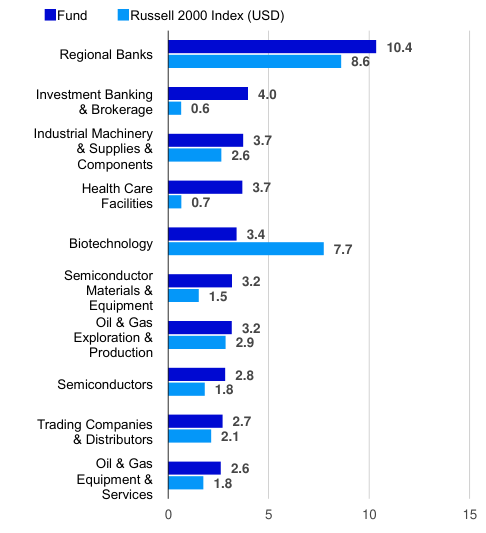

Top industries (% of total net assets)

Performance highlights

The fund outperformed the Russell 2000 Index in the second quarter. Both the fund and benchmark index had negative returns, but the fund declined less. Stock selection in technology, consumer staples, financials and energy contributed to the fund’s outperformance of the index. Selection in materials and industrials detracted.

Contributors to performance

Tenet Healthcare operates hospitals, imaging centers, ambulatory surgery centers and other health facilities. The company has benefited from improving hospital utilization trends, a favorable shift in its procedure mix and use of proceeds from hospital sales to reduce debt.

Sprouts Farmers Market is a health centric specialty grocery store chain that continued to deliver a long runway for growth, strong free cash flow and what we consider an attractive valuation.

Ollie’s Bargain Outlet is a discount retailer of closeout merchandise and excess inventory. The company had strong quarterly results driven by a favorable close-out environment and customers appearing to seek extreme value.

Celestica (CLS) provides outsource design, manufacturing and supply chain solutions to original equipment manufacturers across the communications, enterprise, aerospace, defense, smart energy, health care, industrial and capital equipment markets. The company reported better-than-expected results and raised guidance due to demand from cloud computing.

Piper Sandler is an independent investment bank offering advisory services, equity and debt financing, municipal financing and institutional brokerage services. The company delivered better-than-expected results, driven by strength in its investment banking segment.

Detractors from performance

CryoPort (cryx) provides temperature-controlled supply chain solutions for the life sciences industry. The company delivered weaker- than-expected results due to slower biotech funding, constrained government and academic budgets, post-COVID destocking and lower China demand.

Quanterix (QTRX) is a life science tools and services company. Constraints on capital budgets in the life science industry have reduced demand for the company’s capital-intensive instruments.

Summit Materials provides construction materials. The company reported organic volume declines in aggregates, cement and ready-mix concrete due to bad weather and lower residential demand.

Bloomin’ Brands (BLMN) operates and franchises casual dining restaurant chains under the Outback Steakhouse, Carrabba’s Italian Grill, Bonefish Grill and Fleming’s Prime Steakhouse & Wine Bar brands. The company has seen weaker sales in its core Outback chain, similar to other casual dining chains.

Nextracker provides solar trackers and software solutions used in utility-scale solar power generation projects. The stock declined in June after management announced the acquisition of a solar tracker foundation business.

Top contributors (%)

|

Issuer |

Return |

Contrib. to return |

|

Tenet Healthcare Corporation |

26.56 |

0.51 |

|

Sprouts Farmers Market, Inc. |

29.75 |

0.48 |

|

Ollie’s Bargain Outlet Holdings, Inc. |

23.38 |

0.31 |

|

Celestica Inc. |

27.57 |

0.29 |

|

Piper Sandler Companies. |

16.29 |

0.25 |

Top detractors (%)

|

Issuer |

Return |

Contrib. to return |

|

CryoPort, Inc. |

-60.96 |

-0.46 |

|

Quanterix Corporation |

-43.93 |

-0.41 |

|

Summit Materials, Inc. |

-17.86 |

-0.38 |

|

Bloomin’ Brands, Inc. |

-32.26 |

-0.37 |

|

Nextracker Inc. |

-22.23 |

-0.29 |

Standardized performance (%) as of June 30, 2024

|

Quarter |

YTD |

1 Year |

3 Years |

5 Years |

10 Years |

Since inception |

||

|

Class A shares (MUTF:SMEAX) inception: 08/31/00 |

NAV |

-2.56 |

5.54 |

11.57 |

-0.30 |

9.47 |

6.89 |

7.40 |

|

Max. Load 5.5% |

-7.91 |

-0.28 |

5.42 |

-2.17 |

8.23 |

6.28 |

7.15 |

|

|

Class R6 shares (MUTF:SMEFX) inception: 09/24/12 |

NAV |

-2.49 |

5.71 |

12.05 |

0.13 |

9.97 |

7.40 |

9.31 |

|

Class Y shares (MUTF:SMEYX) inception: 10/03/08 |

NAV |

-2.44 |

5.71 |

11.87 |

-0.06 |

9.75 |

7.15 |

9.28 |

|

Russell 2000 Index (‘USD’) |

-3.28 |

1.73 |

10.06 |

-2.58 |

6.94 |

7.00 |

– |

|

|

Total return ranking vs. Morningstar Small Blend category (Class A shares at NAV) |

– |

– |

34% (192 of 601) |

64% (346 of 575) |

28% (146 of 546) |

64% (240 of 390) |

– |

|

Expense ratios per the current prospectus: Class A: Net: 1.26%, Total: 1.26%; Class R6: Net: 0.82%, Total: 0.82%; Class Y: Net: 1.01%, Total: 1.01%. Performance quoted is past performance and cannot guarantee comparable future results; current performance may be lower or higher. Visit Country Splash for the most recent month-end performance. Performance figures reflect reinvested distributions and changes in net asset value (NAV). Investment return and principal value will vary so that you may have a gain or a loss when you sell shares. Returns less than one year are cumulative; all others are annualized. Index source: RIMES Technologies Corp. Please keep in mind that high, double-digit returns are highly unusual and cannot be sustained. Had fees not been waived and/or expenses reimbursed in the past, returns would have been lower. Performance shown at NAV does not include the applicable front-end sales charge, which would have reduced the performance. Class Y and R6 shares have no sales charge; therefore performance is at NAV. Class Y shares are available only to certain investors. Class R6 shares are closed to most investors. Please see the prospectus for more details. For more information, including prospectus and factsheet, please visit Invesco.com/SMEAX Not a Deposit Not FDIC Insured Not Guaranteed by the Bank May Lose Value Not Insured by any Federal Government Agency |

Read the full article here