Telefonica (NYSE:TEF) offers a high-dividend yield, but its dividend coverage could be better based on earnings, plus its weak growth prospects and relatively high valuation make it an income trap.

Company Overview

Telefonica is a telecommunications company based in Spain, offering fixed and mobile telephone, broadband, and subscription television services, plus other technology services, such as cybersecurity, big data, and cloud solutions.

Its current market value is about $25 billion and trades in the U.S. on the New York Stock Exchange through its ADR program. Its largest shareholder is the Spanish government with a stake of about 10%, followed by Saudi’s Public Investment Fund with 9.9%, and by CaixaBank (OTCPK:CAIXY) with about 5%.

Telefonica is the incumbent telecom operator in Spain, which remains its largest market, even though it has a diversified geographical presence in Europe and Latin America. Indeed, Spain generated some 31% of its total revenues in 2023, followed by Brazil (24%) and Germany (21%), while other markets have smaller weights.

As a relatively large company that operates in a mix of mature and emerging markets, namely in Latin America, Telefonica’s growth prospects are better than compared to some of its European peers, even though investors should be aware that the telecom industry is mature, and growth prospects aren’t particularly impressive over the long term.

Moreover, competition in the industry is quite strong, particularly in Europe, which puts pressure on revenue and earnings as most markets have three or four players, each one trying to win market share over competitors. This means its pricing power can be considered to be relatively weak, even in markets where it has a larger market share, such as Spain.

Indeed, competition from Zegona and MasOrange in Spain is quite intensive, and Telefonica as the leading player is the one to potentially lose the most market share. In Germany, its business prospects aren’t also much better, as Telefonica will lose its main customer (1×1) in the wholesale segment by mid-2025 as the German company is switching into Vodafone’s (VOD) infrastructure, impacting negatively Telefonica’s revenue in the country. On the other hand, it has better growth prospects in Latin America, namely in Brazil where it holds a mobile market share of about 39% through Vivo, being the market leader in the country.

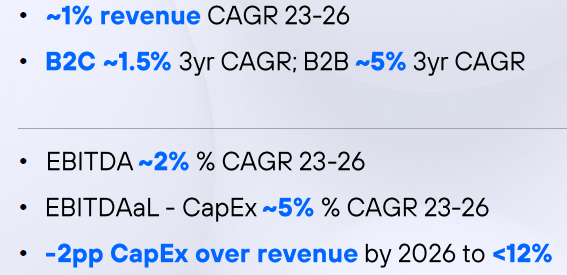

Despite that, Telefonica’s financial targets aren’t particularly impressive, reflecting its business headwinds in the coming years, expecting to achieve annual revenue growth of about 1% during 2023-26, and its EBITDA should increase annually by about 2% during the same period. This clearly reflects that Telefonica’s business growth prospects are quite low ahead, while on the other hand its free cash flow generation is expected to increase by more than 10% annually due to its efforts to reduce costs and share the burden of its investment with other partners through joint-ventures, leading to a higher cash flow generation over the medium term.

Financial targets (Telefonica)

Financial Overview

Regarding its financial performance, Telefonica has reported a relatively stable performance over the past few years, with revenues being around €40 billion per year and its EBITDA has been around €12 billion annually, representing an EBITDA margin of around 30% in recent years.

As I’ve covered in previous articles, this does not compare well with some of its peers, considering that regarding growth Deutsche Telekom (OTCQX:DTEGY) has much better prospects due to its exposure to the U.S. market, while regarding profitability its Dutch peer KPN (OTCPK:KKPNY) seems to be in a better position because it’s exposed to a concentrated telecom market in the Netherlands.

While Telefonica is more diversified geographically than most of its peers, this isn’t necessarily positive, as the company is exposed to several tough markets (Spain, Germany, the U.K.), in which the competitive dynamic is not expected to change much in the near future.

Another sign that being geographically diversified across several European markets does not necessarily create value is Vodafone, which has for many years struggled to report positive operating trends in Spain and Italy, and has decided in recent months to dispose its operations in both countries.

Therefore, I don’t see Telefonica’s geographical diversification to be a competitive advantage, as synergies between different markets are quite low, and macroeconomic conditions usually are similar across Western Europe, thus being geographically diversified doesn’t seem to create much value over the long term.

Taking into account this background, it’s not surprising that Telefonica has reported a relatively weak operating performance in 2023, with revenues increasing by only 1.6% YoY to €40.6 billion. Its operating income was €2.6 billion, a decline of 36% YoY, impacted by higher costs and losses in investments accounted for by the equity method. Its bottom-line was negative last year, reporting a loss of €574 million (vs. a profit of more than €2.3 billion in 2022).

However, these results were significantly impacted by a one-off effect, namely the goodwill impairment of close to €3.6 billion in its U.K. joint-venture (VMO2), in which Telefonica has a 50% stake, impacting negatively its accounts by some €1.8 billion. Adjusted for this effect, Telefonica’s net profit would have been around €1.2 billion, still representing a sharp drop compared to the previous year.

During the first half of 2024, its operating performance was not much different compared to its recent history. In Q2 2024, Telefonica’s revenues increased by 1.2% YoY to €10.2 billion, supported by growth across its several segments. Geographically, Brazil was its major growth driver (+3.3% YoY), while Germany and the U.K. were weaker, reporting stable revenues compared to the same quarter of last year.

Its EBITDA increased by 1.8% YoY to €3.2 billion in the quarter, representing an EBITDA margin of 31%, which is a positive outcome considering the inflationary environment and cost pressure, which Telefonica has been able to manage well and protect its profitability. However, due to lower income from its VMO2 joint-venture, its net profit declined by 3.3% YoY to €447 million in Q2 2024, which is not particularly impressive.

For the full year, the company has maintained its guidance unchanged, expecting to report revenue and EBITDA growth of 1-2%, which is quite low and reflects its several business challenges including fierce competition and lack of pricing power, factors that have structurally impacted its business historically and aren’t expected to change much in the near future.

Indeed, according to analysts’ estimates, Telefonica is expected to report very muted growth ahead, given that its revenues are expected to be about €41.9 billion by 2027 (vs. €41 billion in 2024) and its EBITDA is expected to decline to €12.8 billion (vs. €13.2 billion in 2024), showing that its financial performance is not expected to improve much over the next few years.

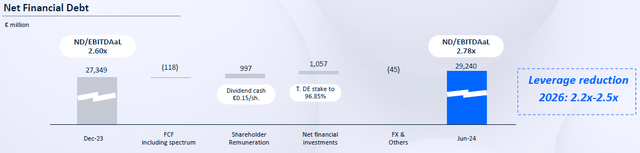

Regarding its balance sheet, Telefonica’s strategy has been to reduce its leverage in recent quarters, aiming to achieve a net debt-to-EBITDA ratio between 2.2-2.5x by 2026, which is an acceptable leverage position compared to its telecom peers. However, its current leverage ratio is close to 2.8x, which is somewhat high and shows that Telefonica needs to reduce debt going forward, considering that its EBITDA is not expected to grow much over the medium term.

Leverage (Telefonica)

This means a good part of its organic cash flow generation should be allocated to debt reduction, even though Telefonica also wants to maintain an attractive dividend in the future.

Its current annual dividend is €0.30 per share, with a semi-annual frequency, which at its current share price leads to a dividend yield of 7.4%. This is quite attractive for income investors, but its dividend sustainability is not great, considering that its payout ratio is close to 100% based on its forecasted EPS for 2024, which is clearly a very high payout ratio.

Based on cash flows, its coverage is better, given that Telefonica’s cash outflow related to its dividend payments is about €1.8 billion per year, while its free cash flow was €2.3 billion in 2023 and is expected to grow to about €3 billion by 2026. Therefore, while Telefonica’s dividend’s coverage could be better on earnings, I don’t expect a dividend cut in the near term, something that the street seems to agree with given that current consensus is for a flat dividend of €0.30 per share over the next few years.

Regarding its valuation, Telefonica is currently trading at 11.8x its forward earnings, which is at a premium to its historical valuation of 10.1x over the past five years. Compared to its peers that also have low growth prospects, such as Orange (ORAN), BT Group (OTCPK:BTGOF) or Vodafone (VOD), this also seems to be a high valuation given that its peers trade, on average, at less than 9x earnings.

Conclusion

Telefonica has very weak growth prospects and does not have any competitive advantage in the telecom industry, plus its valuation is not particularly cheap compared to its closest peers. While it offers a high-dividend yield, its coverage based on earnings could be better and has low dividend growth prospects, and thus Telefonica doesn’t seem to be a great income investment over the long term. I think KNP is a much better income play in the European telecom sector, as I’ve covered previously here.

Read the full article here