U.K. retailer J Sainsbury (OTCQX:JSAIY)(OTCQX:JSNSF) continues to run a solid supermarket business as well as growing its digital and non-supermarket footprint (a strategy I outlined in J Sainsbury: A Growing E-Commerce Story).

I last covered the name in my July 2022 “sell” piece Sainsbury: Not An Exciting Investment Case For Now, since when the shares have moved up by 7%.

My concern at that time was not the business, but its valuation, which I felt looked high. I continue to feel this and maintain my “sell” rating.

Business Strategy Feels Right but is Delivering Inconsistent Results

I like the company’s strategy of building on its supermarket base and expanding its digital shopping footprint not only in groceries but also general merchandise through its Argos arm, for example.

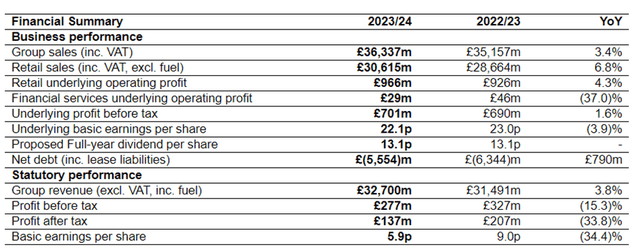

For now, though, the business results remain uncompelling. Last year, post-tax profit was £137m on sales of £36.4bn (including value added tax). That equates to a net margin of 0.4%.

company final results announcement

The company points to market share gains and says, “Customers continue to respond to the investments we have made in value, innovation, availability and service”. I’m not sure about the service based on my own store visits, but food quality and availability both do well. Comparing Sainsbury to Tesco, from a quality and ergo value for money perspective, I much prefer the former (but as my town has a Tesco not a Sainsbury I rarely shop in Sainsbury’s).

Why, then, the disappointing bottom line?

The company points to a planned restructuring of its financial services division. The company said that its overall underlying profit before tax was £701m and that non-underlying items predominantly relate to the planned downsizing of its inhouse financial services offering. I would therefore expect them to be non-recurring. Its accounts for last year included £368m of restructuring and impairment charges affecting profit before tax.

If all of that went into pre-tax profit next year we would be looking at pre-tax profit of around £645m. That far exceeds performance in most recent years, so while on paper it is possible in reality I doubt it to materialise at that level. I expect further non-underlying costs to eat into profits.

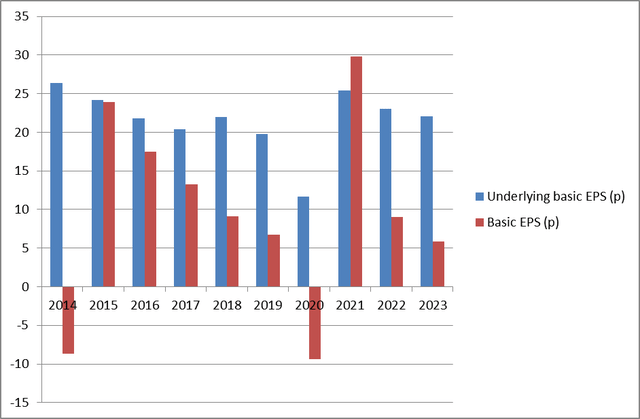

To illustrate this, let’s consider Sainsbury’s gap between what it calls “underlying basic EPS” and the statutory measure of basic EPS over the past decade.

Chart compiled by author using data from company annual results announcements

Slimming down financial services makes sense in some ways so the retailer can focus on its core competences (Tesco has been taking a similar approach in recent years). The Argos brand continues to perform well even after a lot of its standalone sites were closed (Argos units have been opening inside Sainsbury shops – the little anecdotal evidence I have heard about this has been negative, but the numbers suggest otherwise). That approach has reduced Argos’ operating costs by 3% of sales since 2019-20 and excluding its discontinued operation in the Irish republic, Argos like-for-like sales growth last year of 1.5% outstripped the 0.5% decline seen in the Sainsbury stores’ general merchandise sales.

I also think the company’s focus on quality food in recent years has helped it continue to perform well not only against Tesco but also German discounters Aldi and Lidl, whose food quality is often decent despite competitive prices.

Still, the strategy may look good, but recent bottomline performance has been inconsistent. Discounting remains a big risk – Aldi and Lidl continue to expand.

Valuation Continues to Look High

The share price has moved up since my last piece, but I continue to see it as too high. At 45, the current price-to-earnings ratio looks extreme to me. Rival Tesco sits on 12, by contrast.

Partly, Sainsbury’s high P/E ratio reflects a sharp fall in earnings last year. However, of the past five years, in four of them, the highest earnings have been £207m, which at today’s share price would equate to a P/E ratio of 30. Only 2022’s exceptionally high post-tax earnings of £677m would give anything like what I see as a reasonable valuation in P/E ratio terms (9) – but that was only one of the past five years and I see no indication to expect that the company’s profits are heading back anything like that high in the medium term.

In its final results, the company said it is “confident of delivering strong profit growth” this year. It said it expects retail underlying profit growth of 5-10% and a lower profit contribution from financial services. Given that, unless there are more favourable numbers than before somewhere between underlying profits and statutory profits, that “strong profit growth” sounds like it will be in the single digits as a percentage.

So we are still looking at a prospective P/E ratio in the thirties, which I regard as significantly too high for a U.K. retailer with a history of strong earnings fluctuation. Closer to Tesco’s P/E ratio of 12, perhaps with a premium (or not) for Sainsbury’s more diverse of businesses and digital footprint strikes me as a more appropriate valuation.

Accordingly, I continue to rate the name as a “sell” at its current price.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here