JBS S.A. (OTCQX:JBSAY) 2Q24 results were very good, with significant improvement in the core business Seara, record margins in poultry and pork, and organic expansion in Brazil. The super important North American sector remains muted, probably until 2026 at least. The company’s better cash flow generation led to a doubling of dividends, to $0.7 per share (close to 6.5% yield), without affecting net debt reduction.

Overall, my thesis on the company has not changed since my original article in January. I expected JBS’s segments to return to average profitability from a very challenging position. In 2Q24, we saw most of the segments operating normally, with pork and poultry probably above normal thanks to low grain prices. This is what we had also seen in March and May. With the stock price mostly unchanged since my last article, I continue to believe the stock is a Buy at these prices. The valuation is based on cycle-average profitability, and therefore leaves some upside in case of above-average profitability for a period.

Great 2Q24

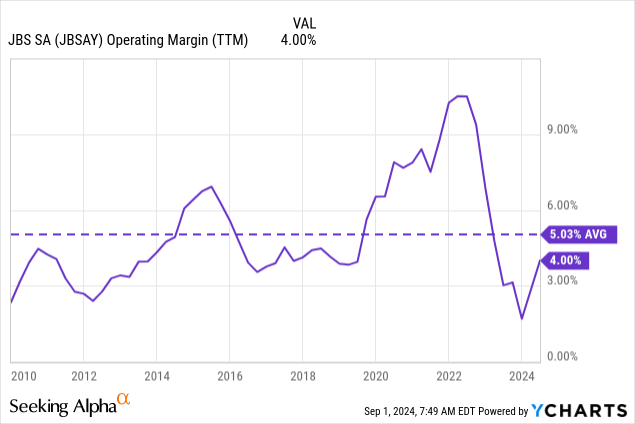

JBS posted revenues of $19.3 billion and a consolidated EBITDA margin of 9.8%, five percentage points above 2Q23 when it was in the midst of a multi-market crisis. The recovery is complete in most markets, with some already getting hot on their cycle. The only segment lagging continues to be North America, and management has commented that is not expecting a great 2025 in that market.

Seara, pork, and poultry firing all cylinders: Seara, the company’s processed poultry and pork brand in Brazil and some foreign markets (mainly the Gulf countries), had been challenged by operational problems attached to the addition of new plants. This quarter, the segment posted EBITDA margins of 17%, from only 4% last year. The improvement, which had been promised by management since at least 3Q23, was based half on operational improvements and half on better grain prices (according to the call).

The improvement in grain prices was also felt in record margins at Pilgrim’s Pride (poultry) and USA Pork. Pilgrim reached margins of 17% (the highest quarterly EBITDA in history), and USA Pork grew 22%. These two segments benefit from lower costs (grains) and higher prices (as cattle prices continue to increase, leading people to choose pork and poultry over beef).

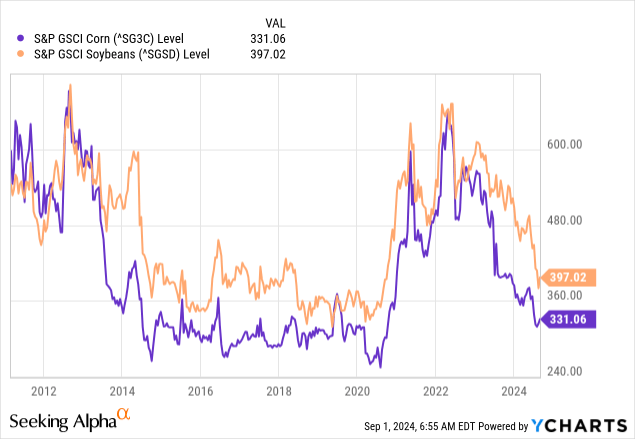

Grain prices continue falling: The cycles in poultry and pork are much faster than in cattle because these animals are raised more rapidly, so production can adjust easily. The main determinant of producer and processor profitability is grain prices, which have consistently collapsed. The rapid increase in 2021 led to the meager results of 2022/23 for these segments.

Although predicting the prices in these markets is impossible, we can clearly observe that there is not a lot more space for prices to continue decreasing, given the previous lows between 2015 and 2020.

JBS management has commented that all USA Pork, Pilgrim’s Pride, and Seara are moving into more value-added products, which lead to more stable and permanently higher businesses, but I would not project the current margins going forward for these businesses (happily, we don’t need to, as seen below).

Newcastle disease controlled: During July and August, a few cases of Newcastle disease emerged in Brazil. The disease kills poultry and presents no danger to humans, but it could have led to poultry sacrifices and the closing of processing facilities and export markets from Brazil. Fortunately, Brazil has already declared that it is free of the disease, and JBS has said that the effect on its operations has been negligible.

Beef improving in Brazil, challenged in North America up to 2026: The beef market is a different thing, much more cyclical, as building herds takes more time. In Brazil, the company has benefited from lower grain prices, which has led to lower cattle prices (down 15% YoY). It has given part of this improvement to consumers via lower prices, which has led, according to management, to a significant increase in consumption (12% higher domestic demand for JBS). (Source: JBS 2Q24 release, under JBS Brasil).

North America, on the other hand, continues to be very challenged. Wholesale beef prices are low while cattle prices are high, eating on the company’s margins. The segment leader (one of the company’s founders, Wesley Batista), commented that the situation is slowly improving (they are seeing cattle slaughter down 15% YoY) but that they are not seeing meaningful changes in the market until 2026.

Capital allocation: The company is directing investment to the salmon farms it has in Australia ($67 million), and to quadrupling its production capacity in the processed poultry segment in Saudi Arabia (the Jeddah facility, taking $50 million). The company has significantly released the pedal in expansion CAPEX, from $200 million in 2Q23 to $127 million in 2Q24.

Debt and dividends: JBS announced a $0.7/ADR dividend to be paid to holders as of late August. This dividend, costing $800 million, is a double from 2023 dividends and a return to the average dividend in 2021 and 2022.

In this way, the company is using more than the FCF it has generated in 1H24 ($450 million YTD). However, the company is confident that 2H24 will be a cash flow generating semester and therefore, net debt should go down for the year.

Ratings and listing: In addition, the company is confident that the rating agencies will improve its rating from negative to stable. JBS is already investment grade and has cheap long-term fixed 5.6% debt, but still, better ratings are always good.

On the listing front (the company wants to list directly in the US, now having only an illiquid ADR), there are no news so far.

Valuation and thesis unchanged

Since my first Buy article on JBS, my thesis has been based on the discount to cycle average profitability.

With revenues of $72 billion, a 5% historical margin leads to operating income of $3.6 billion. Applying a tax rate of 25% leads to cycle-average NOPAT of $2.7 billion. Finally, removing interest expenses of about $1.5 billion and an effective tax rate of 25% from the $3.6 billion in operating income leads to cycle-average net income of $1.57 billion.

I should comment that this cycle-average level does not include the fact that so far, JBS cycles have trended upward in terms of operating margin as it has moved downstream and has improved its operations and scale in most markets.

Still, based on the above and trading at a market cap of $13 billion and an EV of $29 billion, the stock presents multiples of 8.2x for P/E and 10.7x for EV/NOPAT (the better P/E from debt at lower yields than the company’s return on capital).

I still believe these figures represent an opportunity, given that they are based on cycle-average profitability, and that the company is not today posting record margins (especially because North America is still challenged).

For that reason, I maintain my Buy rating on the stock.

Risks

There are two risks for JBS that I think deserve attention.

First is the potential reversal of the cycle in poultry and pork without an improvement in the cycle for North American beef. This could happen because of lower wholesale prices or higher grain prices. As discussed, predicting grain prices is hard, whereas poultry and pork have more moderate wholesale price cycles than beef.

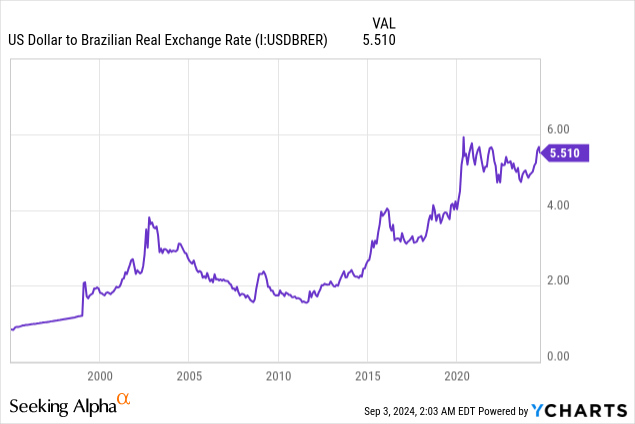

The second risk is the depreciation of the BRL against the USD. In this respect, potentially 25% of JBS’ EBITDA is currently generated inside of the Brazilian market (assuming Seara is 100% Brazilian market, which is not). Brazilian prices can become dislocated from the BRLUSD exchange rate, and therefore the same volume of sales at the same level of profitability in BRL can become less USD. The opposite can also happen, but in the past few months (and more generally in the past 15 years) it was the BRL that depreciated, not the other way around.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here