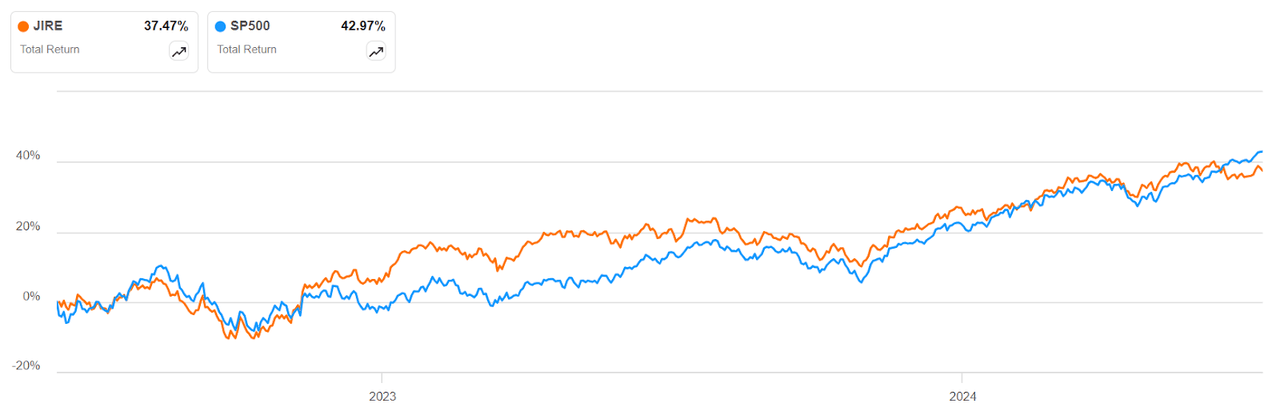

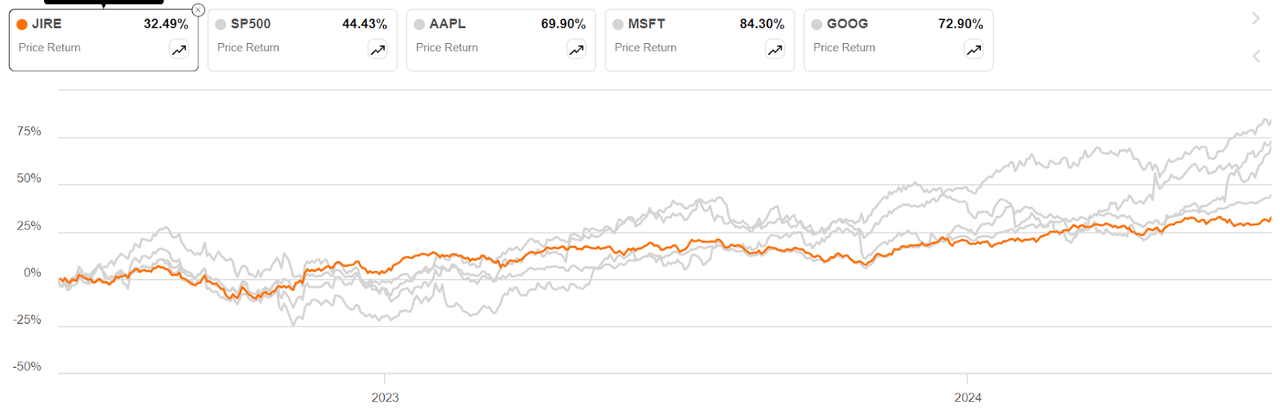

The JPMorgan International Research Enhanced Equity ETF (NYSEARCA:JIRE) is a mutual-fund-turned-ETF that was launched as a different asset class about two years ago in June 2022. Prior to the ETF, it operated as a mutual fund that largely depended on regional research inputs from around the globe for its investment strategy. The fund invests in developed markets and is well-diversified into financials, industrials, healthcare and consumer discretionary, with those sectors comprising a little under two-thirds of the $6.65 billion in assets under management. The expense ratio is a reasonable 0.24% net, and one element that stood out for me is that this fund has held its own against (SP500) for the better part of its existence as an ETF. Interestingly, it took a downturn last month around June 10, which is its two-year ETF anniversary.

SA

What’s important to note is that the 2023 period, which was a strong one for SP500, is also when the ETF strongly outperformed the domestic market in the U.S. In its essence, that’s my thesis for this stock. The world today is on the verge of extreme volatility. U.S. capital markets seem resiliently steady, but any sign of weakness could put considerable downward pressure on them. At a time like that, what you ideally want is the kind of broad International exposure that a fund like JIRE offers.

Country Allocation is Important

As important as sector allocation might be, in a scenario where many of the world’s largest economies are still struggling with high inflation and, subsequently, high interest rates attempting to control that inflation, it’s important to be aware of where your fund is investing its monies.

Fund Fact Sheet

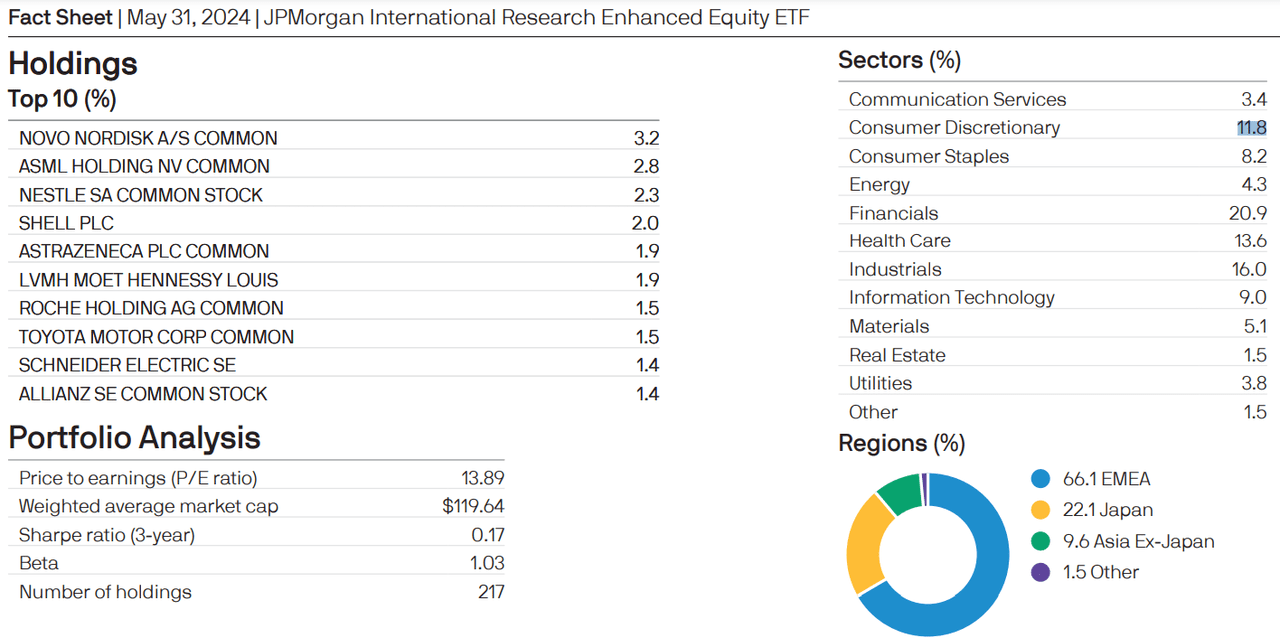

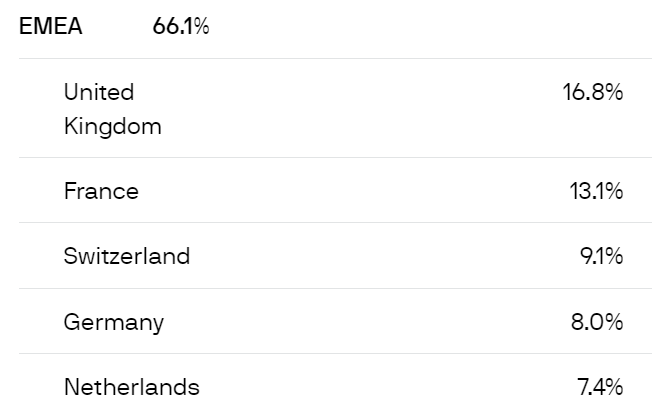

A quick look at the allocation makes it clear that the fund is more diversified in terms of sector allocation than it is in country allocation. The latter is skewed toward the EMEA region, with Japan, making it add up to nearly 90% of the fund. So, this is where your gains, if any, are going to come from. As such, it’s important to see what the economy looks like in these countries – specifically, the top economies in Europe.

Fund website

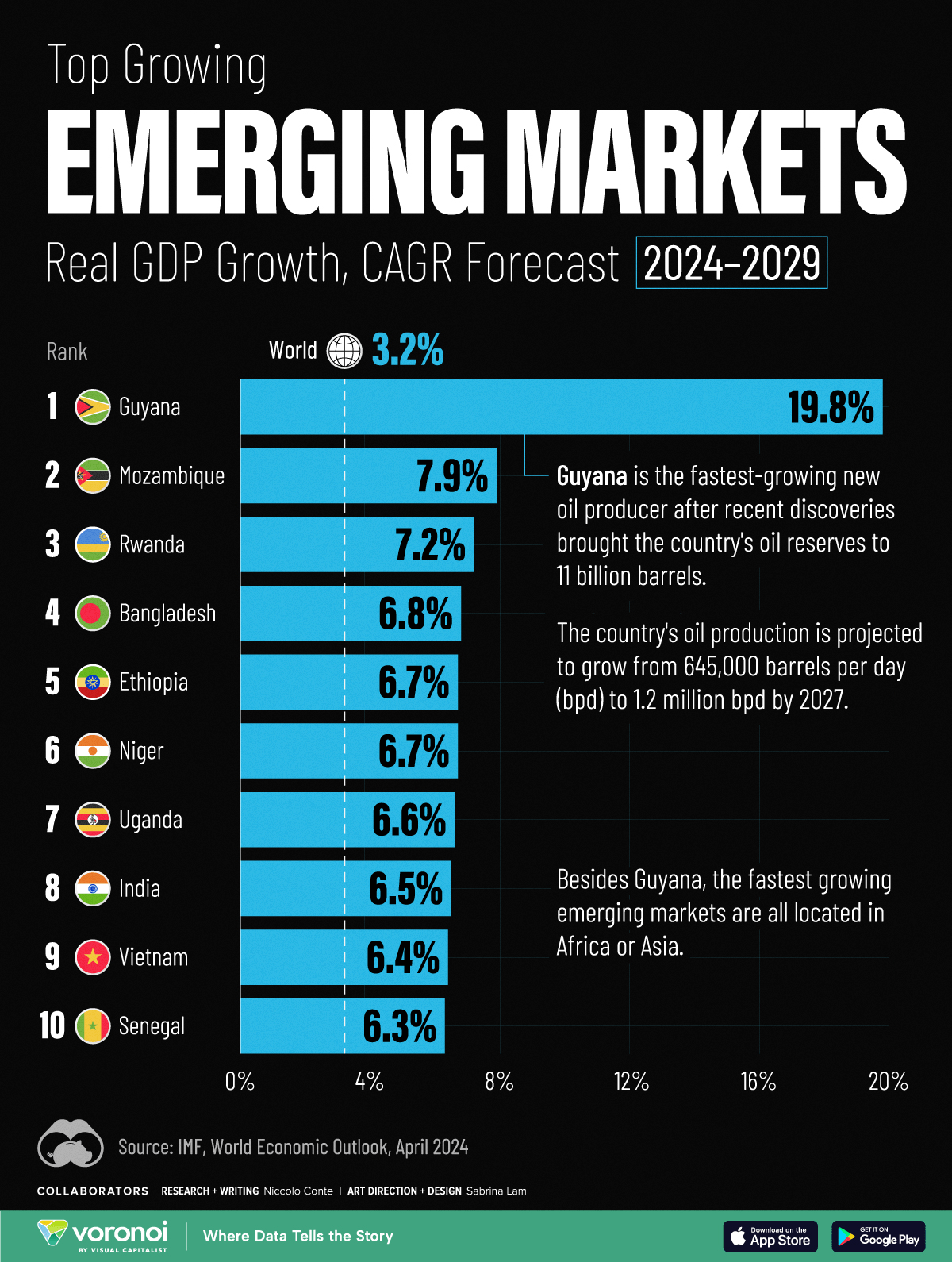

It’s interesting to note that EMEA in this context is restricted to the first E, Europe, with no allocation to either the ME, the Middle-East or A, Africa. That does fit into the developed international markets strategy, but I would have liked to see a few developing and emerging nations feature in this list, particularly because many African nations are expected to grow well above the global benchmark of 3.2% over the next five years.

Visual Capitalist

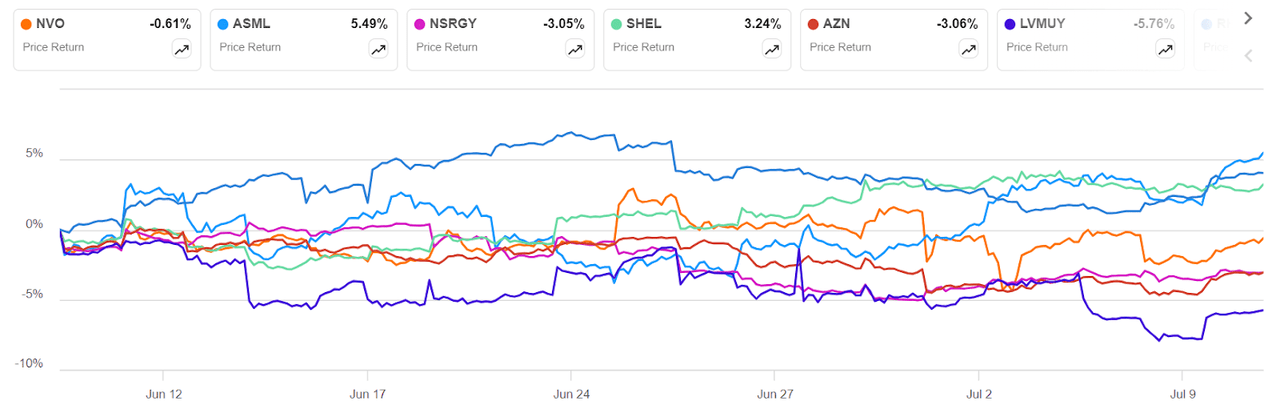

Nevertheless, JIRE seems to have found alpha in developed markets over the past two years. As I mentioned, it’s only a month ago that the fund’s performance started dipping against that of SP500, and looking at the last month’s price chart for some of its top holdings, there’s a clear drag being created by the bigger ones like Novo Nordisk A/S (NVO), Nestlé S.A. (OTCPK:NSRGY), and LVMH Moët Hennessy – Louis Vuitton, Société Européenne (OTCPK:LVMUY)(OTCPK:LVMHF)

SA

I don’t believe this trend will continue for too long, but a lot of that depends on how resilient the U.S. market can be over the next couple of quarters. Let’s not forget that the biggest variables right now are the Fed’s position on interest rate cuts and the U.S. Presidential Election. Either of these could go awry. On the economy side, if the Fed cuts rates too aggressively, it could rapidly devalue the dollar, benefitting European and Asian economies; ironically, if it doesn’t start cutting rates soon, it could cause havoc with America’s economy. On the political side, a second Trump presidency could very well upset the delicate global geopolitical balance (if you can call it that) that the Biden administration is presiding over as the largest economy in the world.

In light of these uncertainties, it’s prudent to buttress your core U.S. holdings with something like JIRE, even considering it a hedge against the numerous things that could go wrong with the U.S. economy over the next several months. The real bull case, however, is based on the fund managing to hold its own against SP500, and even a few of the Mag 7, for the greater part of its existence. I’m confident that JPMorgan Asset Management has the best talent possible managing the fund, with the portfolio managers bringing 51 years of collective experience to the table.

SA

Case in point would be the fund’s performance through all of 2023, when the AI hype sent Mag 7 market caps skyrocketing to unprecedented levels. If we have another tech rally like last year, I can easily see the fund managers rebalancing their portfolio to match what they did last year. I think the last month has been a learning curve for them, as it continues to be for the best investors and analysts, facing new paradigms in the current investment landscape. More importantly, I think they’re fast learners who will figure out how to match U.S. equities’ performance with International assets.

What are the Major Risks Involved?

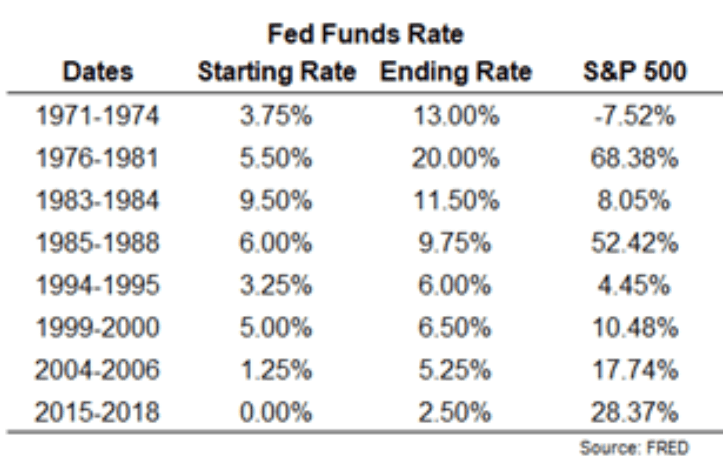

The biggest risk I see here is the U.S. continuing to defy nearly every law of economics. This is a very unique situation that we’ve never been in before. Yes, it’s similar to the late 70s and 80s in many ways, but it’s different in as many. For example, here’s what SP500 returns looked like over several key periods that had a range of different Fed Funds rates.

FRED via Bluerock Wealth Management

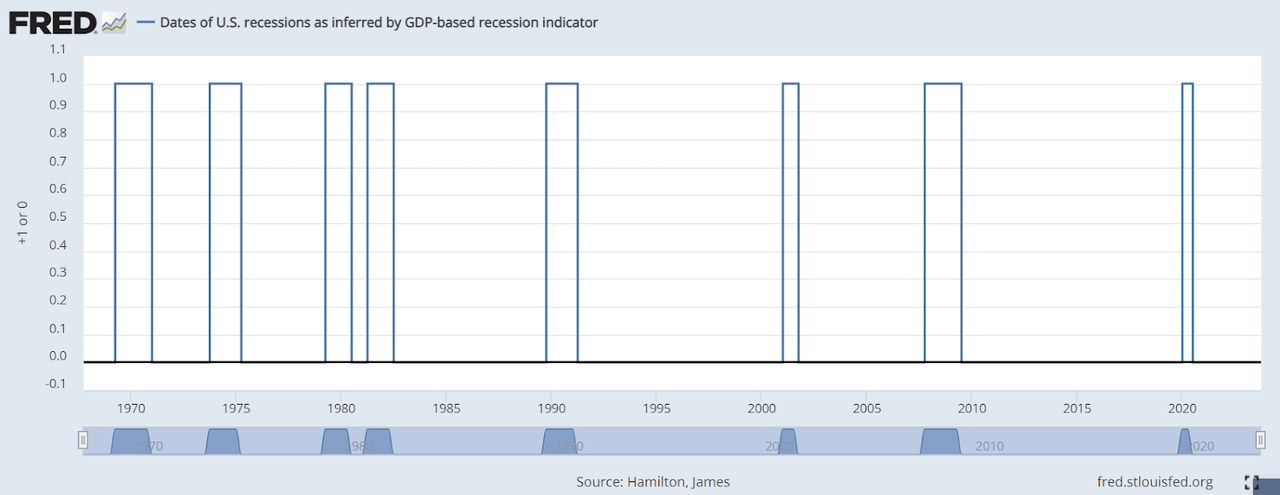

The first thing likely to catch your eye is the stellar performance of the market when interest rates were at or above current levels. You’ll see that it was greatly pronounced in the 1976 to 1981 and 1985 to 1988 periods. Let’s match that against recessionary periods to underscore the point that the U.S. represents a highly resilient economy.

FRED

Despite two recessionary periods between 1979 and 1981, and a time when interest rates rapidly escalated to 20%, that’s one of the highest gain periods for SP500. My point is that it’s hard to bet against the U.S. market. However, it’s not infallible. The negative factors right now are arguably much more intense than they were during that period under discussion. There are kinks in the U.S. economy’s armor, and my opinion is that there’s a tipping point just over the horizon that none of us can see yet.

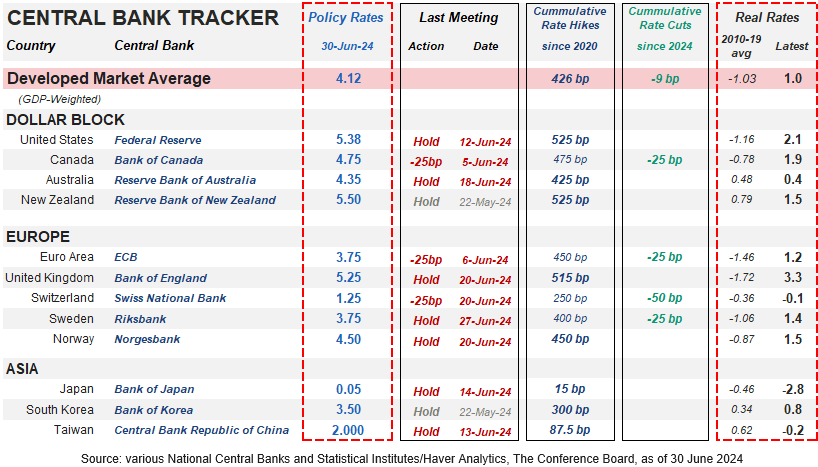

That’s also where a hedge-like investment like JIRE can swoop in to save the day. Of course, we’ll have to concede that European economies – and, indeed, global developed and emerging ones – are likely to echo any trouble in the U.S., but some of them, particularly Asian economies, are feeling the pressure to increase their rates as the U.S. prolongs its higher-for-longer mantra. Some European markets where JIRE invests are still seeing their central banks hesitate to continue any rate cuts, and at the end of June many key markets related to JIRE still have their policy rates in the 4% to 5% range.

FT Adviser

That means the U.S. Fed needs to tread carefully, and it’s not an improbable scenario where interest rates are kept elevated. There were even reports as recently as April that the Fed might consider further rate increases:

Fed Governor Michelle Bowman, arguably the central bank’s most hawkish voice, recently said that she would favor a rate hike “should progress on inflation stall or even reverse.”

Minneapolis Fed President Neel Kashkari last week floated the possibility of not cutting rates at all this year. He also said rate hikes are “certainly not off the table.” But he said they aren’t likely. Kashkari is not voting on monetary policy decisions this year.

Like Bowman and Kashkari, New York Fed President John Williams said rate hikes aren’t part of his baseline outlook. But he said he’s not even remotely considering a rate increase at the moment.

“I don’t see any signs that we’re not having the desired restricted effect on demand that’s helping us achieve our goals,” Williams said in response to a question posed by CNN at a Thursday discussion with reporters. There are “definitely circumstances” that would merit raising interest rates, he added, such as inflation moving materially higher, but the current trajectory doesn’t fit that, he said.

Williams, a top adviser to Fed Chair Jerome Powell, still believes it will be appropriate to cut rates later this year, but declined to specify the quantity and timing.

Boston Fed President Susan Collins said Thursday: “Overall, the recent data have not materially changed my outlook, but they do highlight uncertainties related to timing, and the need for patience — recognizing that disinflation may continue to be uneven.”

Across all these scenarios, I see the U.S. capital markets holding strong against the tide of bad news. For how long? Nobody knows. One thing is certain, though: an investment in overseas markets does sound like a good hedging plan to protect your U.S. equities’ performance. For that reason, I recommend a Buy for JIRE and similar funds that have shown their resilience even when the U.S. markets themselves have been performing well.

Read the full article here