I have covered Juniper Networks (NYSE:JNPR) before and stressed its software-centric strategy. Now that ChatGPT has shown the capability of Generative AI to improve productivity as I will elaborate below, I look into how the company is differentiating its product using artificial intelligence.

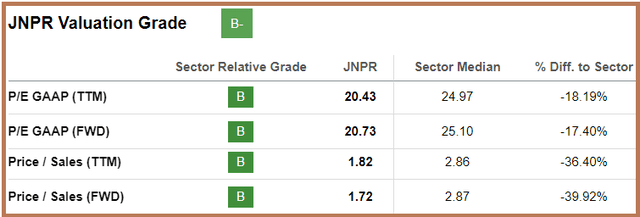

The aim of this thesis is to highlight the value-creating capability of the technology for a company that currently trades at a discount compared to the median for the IT sector, whether it is on earnings or sales multiples as shown below.

JNPR Valuation Metrics (seekingalpha.com)

For this purpose, I will go use the financial data and scan earnings transcripts for management comments as well as shed light on supply chain constraints, which have again become a hot issue after China recently imposed restrictions on the export of certain chip-making metals. There are also demand-related constraints to contend with, but I start by providing insights into how it differentiates products using AI.

The AI Differentiator

With the advent of Work-From-Home or more people working from their apartments following the Covid-induced tendency, the underlying network infrastructure also had to be adapted to cater to a more hybrid workplace. At the same time, the higher frequency of cyberattacks also demands a higher dose of IT security. Hence, in contrast to the previous network configurations which were largely confined to corporate walls and could be protected with perimeter security, post-Covid connectivity is more expansive as most employee access points are located beyond the physical office. As such, the new network architecture which has emerged is best protected with zero-trust network access (ZTNA) and needs to be flexible for easy access to distributed applications located in multi-cloud environments using SD-WAN (software-defined wide area network) and SASE (secure access service edge).

In this respect, some of the vendors which are well-positioned are Cisco Systems (NASDAQ:CSCO), Fortinet (NASDAQ:FTNT), Juniper, and VMware (VMW) with its VeloCloud. Thus, service providers like AT&T (T) or Verizon (VZ) look to these equipment suppliers when having to scale networks at client premises. Their products are also in demand by cloud service providers like Amazon (NASDAQ:AMZN) when rolling out platform-based managed services.

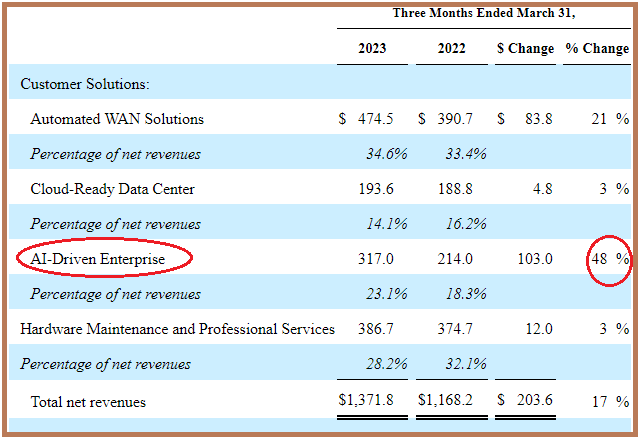

Looking at AI differentiator, this is visible in the very way Juniper classifies its revenues, namely by Customer Solutions, as shown below. Here, in addition to Automated WAN and Cloud Ready Data Center, there is also AI-Driven Enterprise. This comprises both wired and wireless solutions mostly making use of Mist AI. Without going into too many technical details, this is about combining machine learning and data analytics techniques to simplify operations for IT admins as well as provide optimal protection.

FQ1’23 SEC Filings (seekingalpha.com)

Behind these catchy words, it is basically about funneling data from various sources (routers, switches, firewalls) to obtain actionable insights for enabling a high degree of automation which then translates into fewer site visits and rapid problem resolution at a time where 24/7 network availability with zero downtime has become the corporate norm.

Furthermore, for customer support purposes, Mist AI includes an assistant called Marvis which guides users through a natural language conversational interface, in some way similar to the commonly used language employed by ChatGPT. This amounts to simplifying the task of managing increasingly large and complex networks which are also vulnerable to threats and explains why AI-Driven Enterprise sales grew by a whopping 48% YoY in FQ1’23 as encircled in red above.

Thus, AI is now second behind Automated WAN in terms of revenue generation by solutions and constituted 28% of overall revenues in the last reported quarter. However, the Data Center business which generated $293.6 million remains susceptible to supply chain issues as has been the case since the fourth quarter of 2021 (FQ4’21), due to exposure to China as I had explained previously.

Supply and Demand-Related Problems

At that time Data Center sales were down by 9% year-on-year due to orders not reaching customers as intended. The root cause of the problem was Covid movement restrictions blocking the company’s access to Chinese-made components in the form of semiconductors or other electronics needed to assemble networking gear.

Now, the East Asian country has announced that it would ban exports of gallium and germanium which are two metals used respectively in the production of semiconductors and fiber optic cables. While the company neither uses these metals directly nor manufactures chips or cables, the exact impact on Juniper’s operations is not known and more clarification can be obtained during the next earnings call, expected on the 27th of this month.

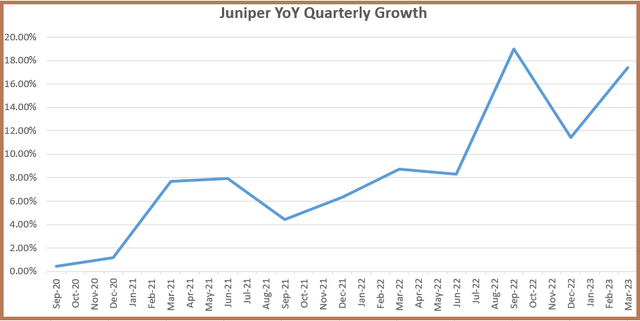

Pursuing further, as seen by the quarterly YoY revenue growth in the chart below, despite its fluctuating path, it has improved since the September 2021 quarter. This improvement has been made possible to Juniper’s supply chain spanning countries like Taiwan, Malaysia, Mexico, and America in addition to China. In addition to diversification in components sourcing, more appropriate timings involving customers rescheduling projects to be aligned with shipment deliveries have also helped.

Chart built using data from (seekingalpha.com)

On the other hand, the company is also facing lower demand for certain cloud products which has mostly to do with deteriorating macroeconomic conditions impacting businesses’ appetite to expand. Thus expect potential revenue shortfalls during FQ2’23 in case some customers delay orders due to economic uncertainty. The problem could be exacerbated in case the Federal Reserve raises interest rates further in the balance of 2023, as the elevated borrowing costs may throw cold water on cloud providers’ willingness to expand their networks, especially if they rely on borrowings for growth.

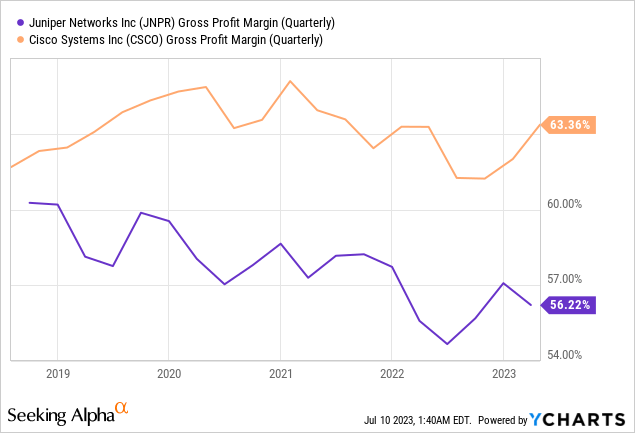

Moreover, Juniper’s ability to grow its revenues has come at a cost.

Thus, as shown in the blue chart below, its gross margins have been trending lower mostly as a result of higher supply chain costs. In this case, a comparison reveals that Cisco’s gross margins have seen less impact as per the orange chart. The reason for this, as I explained in a previous thesis, was the result of the networking giant’s engineering team carrying out modifications at the circuit board level in order to get rid of components that were more difficult to be sourced and replace them with easier-to-procure ones.

Such an ability seems to be lacking for Juniper with the CFO stating that “while supply has improved for the majority of our products, we continue to experience supply constraints for certain components, and supply chain costs remain elevated”.

AI Should Have the Upper Hand

However, gross margins also depend on the revenue mix which could be more skewed towards AI as ChatGPT has raised awareness of the opportunities, especially among CEOs managing companies where the complexity of the network requires more specialized IT staff whose wages have to be raised to keep up with higher CPI (Consumer Price Index).

Detailing further, with AI allowing for a higher degree of automation, there is a need for fewer manual tasks thereby reducing operating costs. At the same time, taking advantage of Mist AI’s natural language interactions (instead of having to learn complex user codes), IT admins are more inclined to use Juniper’s technology as it allows them to be more productive analogously to ChatGPT where you can generate a report way faster than when done in a conventional way. Talking figures, according to research firm McKinsey, 0.2% to 3.3% of annual productivity growth can be obtained through a combination of Generative AI and other technologies.

Scanning specifically for related prospects, according to the CEO, “Our customers are clearly recognizing the value of our cloud-native AI-driven architecture, which helps them optimize user experiences from client to cloud and minimize operating costs through proactive automation”.

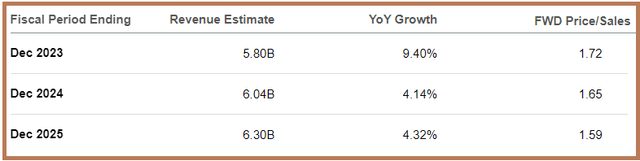

Noteworthily, in addition to intelligent algorithms, there are other reasons for top-tier U.S. corporations to adopt Juniper’s AI-driven solutions, namely for replacing older generation switches. In this respect, with technological evolution and the ever-present need for higher speeds to support the higher traffic volumes due to wider consumption of video, data centers have to upgrade from 100G to 400G, implying that demand for high-end switches is likely to be sustained over the medium term. It is precisely on this basis that the fiscal 2023 revenue guidance was updated to 9.4% above last year as illustrated below.

Revenue: Actual and Estimates (seekingalpha.com)

Talking valuations, this forward Price-to-Sales of 1.72x represents nearly a 40% discount to the median for the IT sector as per the introductory table and, performing only a 10% adjustment, I have a target of $38.74 (35.22 x 1.1) for Juniper based on the current share price of $35.22.

In conclusion, Juniper is a buy due to its AI differentiation which is likely to lead to the generation of more revenues, to offset potential shortfalls due to short-term weakness in demand and supply constraints. In this respect, despite such constraints, the executives expect an improved profitability of 100 basis points for operating margin for 2023 over last year.

To further support this bullish position, which contrasts with my previous sell position in mid-2022 when the company was still supply constrained and could not fulfill some customer orders, this time AI-related sales have accelerated from 24% in FY’22 to 48% in the first quarter of 2023 which marks an extraordinary progression. On top, it is not subject to revenue concentration risks as its top ten customers accounted for only 30% of sales during the last reported quarter, while recurring sales grew at 39%.

Finally, do expect volatility due to exposure to East Asia and for this purpose, more cautious investors may wait for related clarifications before putting their money on the stock.

Read the full article here