One industry that I have been very bullish about for well over a year now is the homebuilding industry. Estimates vary, but usually the consensus is that this country is suffering from a shortage of between 4 million and 7 million homes. Until this shortage is reduced significantly, I would argue that the housing market would be quite attractive for investors. And one company that I have been bullish on during this time, and actually longer, is KB Home (NYSE:KBH).

KB Home

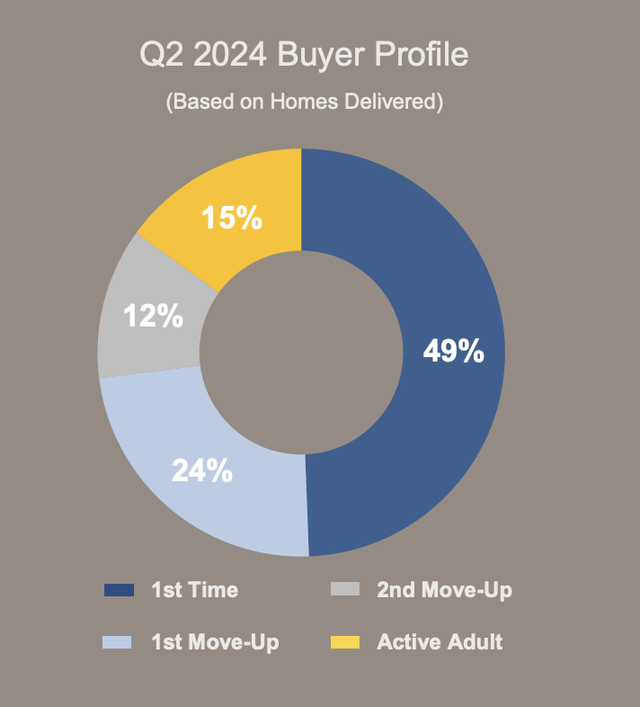

Overwhelmingly, KB Home focuses on newer home buyers. 49% of the homes that it delivered in the second quarter of this year were sold to first time buyers. Another 24% were sold to homeowners that were moving up to another home from their first home. This composition, combined with how shares have been priced and the catalysts facing the homebuilding industry, led me to reaffirm the company as a ‘buy’ candidate when I last wrote about it in January of this year. Since then, things have turned out quite well, with the stock shooting up 34.9% compared to the 17.8% increase seen by the S&P 500 over the same window of time.

As great as this increase is, it pales in comparison to how things have been over the long run. Since my first bullish article about the company, published in March of 2015, the stock is up an astounding 480.1%. By comparison, the S&P 500 is up only 167.7%. After such a massive move higher, you might think that I would be ready to downgrade it to something more modest. But with current catalysts in place and how shares are currently priced, I would argue that keeping the company rated a soft ‘buy’ is logical at this point in time.

KB Home keeps building value

Author – SEC EDGAR Data

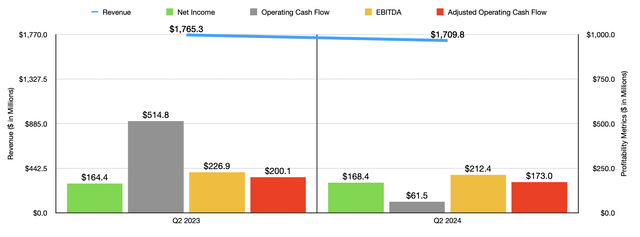

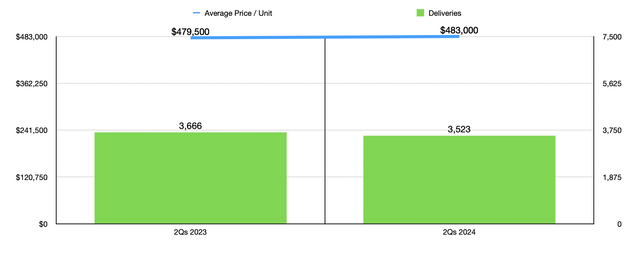

Fundamentally speaking, things have been somewhat mixed for KB Home as of late. Consider the most recent quarter for which data is available, the second quarter of the 2024 fiscal year. During that time, the company reported revenue of $1.71 billion. That is unfortunately down from the $1.77 billion the company reported one year earlier. Even though the company benefited from a rise in the average price of a home delivered from $479,500 to $483,000, this was more than offset by a drop in the number of homes delivered from 3,666 to 3,523.

Author – SEC EDGAR Data

The good news is that the higher pricing helped the company increase its net profits from $164.4 million last year to $168.4 million this year. Unfortunately, all other profitability metrics for the company worsened during this time. Operating cash flow, for instance, plunged from $514.8 million to $61.5 million. If we adjust for changes in working capital, the picture was better, with the metric dropping from $200.1 million to $173.9 million. Meanwhile, EBITDA declined slightly from $226.9 million to $212.4 million.

Author – SEC EDGAR Data

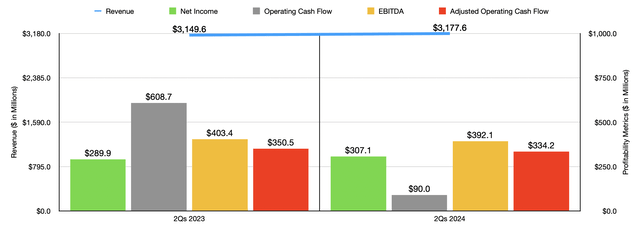

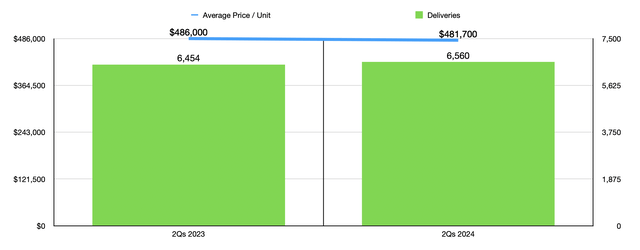

When it comes to the first half of this year compared to the same time last year, KB Home has seen a very similar picture. There was one exception to this. This involves revenue, which increased from $3.15 billion last year to $3.18 billion this year. Despite the pain experienced from a delivery perspective in the second quarter of this year, deliveries for the first half of 2024 came in strong at 6,560 homes. That is slightly above the 6,454 homes delivered during the first half of 2023. Unlike in the second quarter, however, the company did suffer from a drop in the average price of a home delivered. This figure declined from $486,000 last year to $481,700 this year.

Author – SEC EDGAR Data

As was the case for the second quarter on its own, KB Home did see net profits rise for the first half of this year compared to the first half of 2023. Net income grew from $289.9 million to $307.1 million. Other profitability metrics we’re not as fortunate. Operating cash flow plunged from $608.7 million to $90 million. If we adjust for changes in working capital, the decline was much smaller from $350.5 million to $334.2 million. And finally, EBITDA for the company fell from $403.4 million to $392.1 million.

Author – SEC EDGAR Data

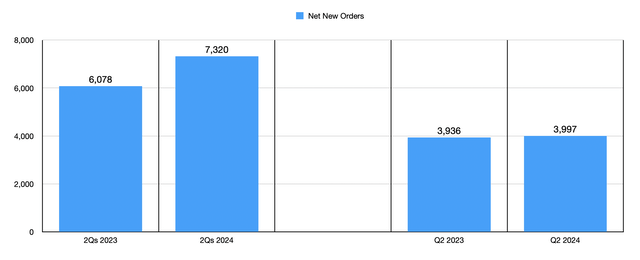

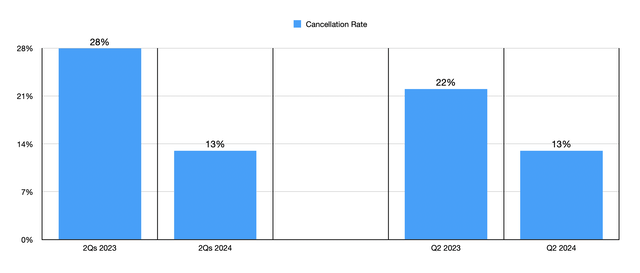

This mixed picture might discourage some investors. Having said that, there are some positives to take into consideration. First, net new orders have been solid. For the first half of this year, the company landed contracts for 7,320 new homes. That’s up soundly from the 6,078 homes the business landed contracts for the same time last year. Admittedly, most of this improvement on a year-over-year basis came during the first quarter. But even the second quarter saw a year-over-year increase from 3,936 homes last year to 3,997 this year. Some of the improvements seen can certainly be attributed to a decline in the company’s cancellation rate. For the first half of last year, this number was a whopping 28%. For the first half of this year, it was only 13%. And for the second quarter, it totaled 13% this year compared to 22% last year.

Author – SEC EDGAR Data Author – SEC EDGAR Data

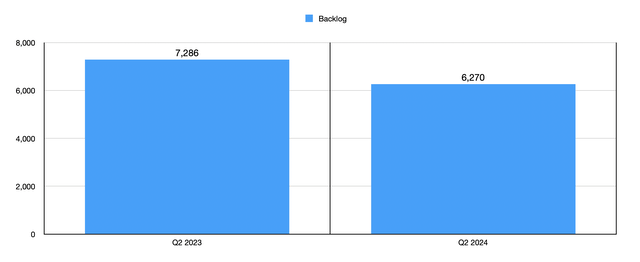

This is not to say that everything is great. Backlog still needs some work. The company ended the most recent quarter with 6,270 homes in its backlog. That is down from the 7,286 homes that the company counted for the second quarter of the 2023 fiscal year. Having said that, everything is about perspective. At the end of 2023, management reported a backlog totaling only 5,510 homes. This means that, in the span of only two orders, the company grew its backlog by a whopping 13.8%. Considering how high interest rates currently are, I consider this to be a remarkable feat.

Federal Reserve

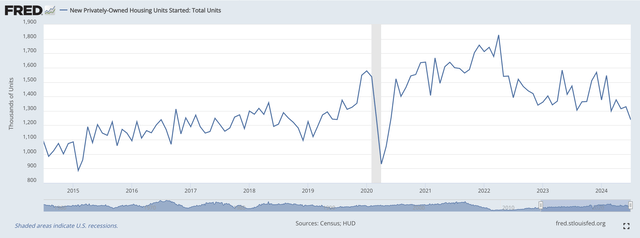

Another thing that I find bullish about the company is the fact that we are experiencing a housing shortage at a time when new privately owned housing starts are on the decline. In the chart above, you can see exactly what I mean. Just take the month of July as an example. During that month of this year, there were roughly 1.24 million new privately owned housing starts. That represents a pretty substantial decline of 16% compared to the 1.47 million the same time last year. The overall trend since around 2022 has been for declines to occur. But at some point, between interest rates declining and pent-up demand for housing increasing, this trend should reverse. When it does, this would be very bullish for the company. And in truth, the improvement in pricing seen in the second quarter of this year compared to the same time last year, the drop in cancellation rate, and the rise in net new orders, could be evidence that we aren’t too far away from that occurring.

Author – SEC EDGAR Data

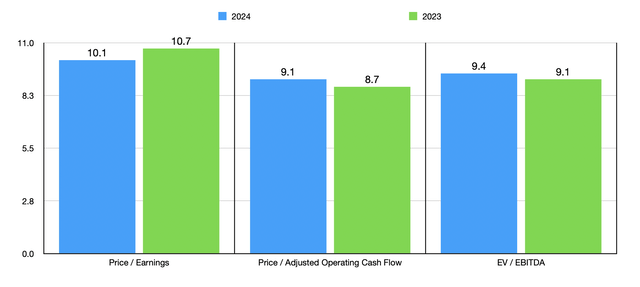

When it comes to valuing the company, I think the best thing to do is to annualize results experienced so far this year. Doing that, we get net income estimated for 2024 of $625.2 million. Adjusted operating cash flow would be $692.9 million, while EBITDA would be $783.5 million. In the chart above, you can see what this means for the valuation of the business. The chart also values the company based on historical results for 2023. To be honest with you, on its own, the company is getting pretty close to being fairly valued. And relative to similar firms, I would say that’s the case as well. In the table below, I compared KB Home to five comparable firms. On a price to earnings basis, our candidate was the most expensive of the group. It was the cheapest on a price to operating cash flow basis. But when it comes down to the EV to EBITDA multiple, I found that three of the five companies ended up being cheaper than it is.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| KB Home | 10.1 | 9.1 | 9.4 |

| Taylor Morrison Home Corporation (TMHC) | 9.7 | 18.6 | 8.2 |

| Meritage Homes (MTH) | 8.4 | 19.1 | 6.8 |

| Century Communities (CCS) | 9.6 | 74.7 | 9.6 |

| Beazer Homes USA (BZH) | 6.4 | 25.8 | 12.3 |

| M/I Homes (MHO) | 8.4 | 16.1 | 6.6 |

Takeaway

Based on the data provided, I would say that KB Home is certainly experiencing some mixed results at this time. But on the whole, I think the picture is bullish for the business. Shares might be fairly valued compared to other companies. But they are still undervalued on an absolute basis to me, even if only marginally so. This puts the company on the edge between a ‘buy’ and a ‘hold’. But when you consider the catalyst, that I think, should propel revenue and profits higher, I believe that enough additional upside is on the table to justify a soft ‘buy’ rating.

Read the full article here