Intro

We wrote about Kforce Inc. (NYSE:KFRC) in February of this year when we were bullish on the technology segment of the professional staffing services company. It is a given that company-related technology spending will continue to increase as the information age continues to gain traction. This dynamic gives Kforce a solid foundation due to its long-term relationships with its clients, as well as its ability to charge top-dollar for its technology-related solutions.

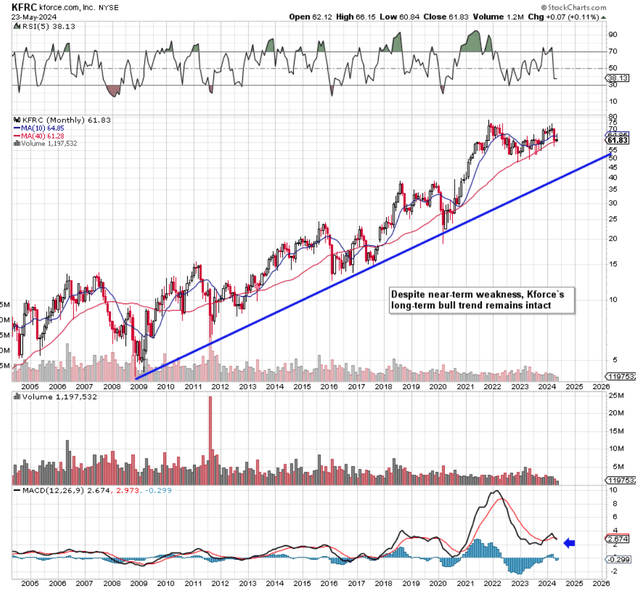

Shares over the past 3 months or so have declined approximately 8%, trading beneath intermediate temporary support of $62 a share. In saying this, we are standing pat on our ‘Buy’ recommendation, as there is still not sufficient evidence from a technical standpoint that Kforce’s long-term uptrend has come to a halt. To this point, the company’s profitability & valuation metrics still check out, which is why we recommend investors remain patient here until this present volatility runs its course.

As we see below on Kforce’s long-term chart, sustained higher lows & higher highs have been the order of the day since 2008. Although the stock’s 40-month moving average has been breached occasionally over the past 15 years, this support level by and large has acted as strong support, demonstrating that Kforce remains a proven recession-proof stock. Furthermore, the stagflation in the share price over the past 2+ years has brought the long-term MACD indicator back down to a level that may have the ability to prompt an upturn in the stock once more.

Kforce Long-Term Technicals (Stockcharts.com)

Reading Between The Lines Concerning The Recent Q1 Earnings Report

Kforce’s Q1 headline earnings numbers were announced on April 29th where both earnings and revenues declined by double-digit percentages compared to the same quarter of twelve months prior. Although the in-line EPS of $0.58 per share in Q1 & revenues of approximately $352 million did little to convince investors, we believe (upon further study of the report & associated trends) that Kforce’s fundamentals remain in solid shape for the following reasons.

The overriding reason why Kforce’s earnings will remain elevated is due to the proliferation of AI in recent times. Although many labor-orientated jobs, unfortunately, will go by the wayside in the emerging ‘new’ economy, we see the demand for Kforce consultants continuing to grow, so organizations can remain ahead of the curve. Suffice it to say, that when a consultant’s services not only assist but remain critical to how a respective company transforms its digital abilities, there appears to be no other outcomes other than demand remaining elevated for Kforce which is again tested by how much repeat business it garners. The CEO pointed to the same on the company’s recent earnings call.

Our core competency is rooted in the ability to identify and provide critical resources, real-time and at scale, to help world-class companies solve complex problems and help them competitively transform their businesses.

Firstly, as alluded to above, what will underpin Kforce’s success going forward is the sustained spending by companies on technological initiatives. Although the macroclimate continues to bring uncertainty to how and when companies spend their money, management did mention that there was a sizable improvement in technology assignments starting in March of Q1. We expect this momentum to continue into Q2 with sequential growth expected over the next couple of quarters (EPS of $0.73 & $0.80 expected in Q2 & Q3 respectively)

Suffice it to say, given that sustained technological spending is here to stay, Kforce just needs to make sure it remains in a position to keep capitalizing on the established trend. Demand is not the problem, it is making sure the company continues to get paid in a timely fashion (accounts receivables) To this point, with relation to the adding of value over time (thus making it impossible for clients to refuse Kforce’s services), the company continues to double down on its managed teams’ investment, project solutions capabilities & integration of the same. Taking the above into account along with the company’s direct hire and staffing services, Kforce has positioned itself at the forefront to be able to keep offering its customers complex solutions to their IT challenges.

Continuous Buybacks Positively Affect Valuation

Therefore, given the searing ROE Kforce continues to report, let’s discuss Kforce’s valuation from a different perspective and how I believe it will continue to improve irrespective of near-term growth rates. In our previous commentary, we focused on Kforce’s rising return on capital and how growing profitability was affecting the valuation of the stock favorably. Furthermore, as we learn below, I believe the valuation of the stock from a balance sheet perspective is much stronger than presently perceived.

Over the past four quarters in Kforce, GAAP profit came in at $55.9 million, resulting in an operating cash flow of $85.6 million. Now given that capex spending only amounted to 9%+ of 12-month trailing operating cash-flow, 90%+ of that cash-flow ended up being free cash-flow which is key.

Now that cash has to go somewhere so when you hear the CFO state on the recent Q1 earnings call that more than $900 million of cash has been returned to shareholders since 2007, you see immediately that Kforce is a proven shareholder-friendly company. A company that is willing to put its money where its mouth is concerning the cash flow it generates through buybacks & dividend reimbursements. Furthermore, what is key is that the enriching of shareholders has not affected Kforce’s long-term profitability trends. ROE as alluded to above comes in at almost 32%, dwarfing the current sector median (ROE of 12.5%).

Stated Price To Book Multiple Is Misleading

As we see below specifically through Kforce’s trailing book multiple of 7, investors may believe that shares of the staffing company are too expensive from an asset standpoint. Just remember from a reporting standpoint, Kforce’s assets are essentially its account receivables. The quicker the company gets paid, the quicker it can turn over its cash and boost that ROE even more.

Kforce Valuation Metrics (Seeking Alpha)

Kforce’s stated equity reached $164.5 million at the end of Q1. However, $896 million of treasury stock also sits on the balance sheet, points to the following. Treasury stock refers to the stock management has repurchased to date but has yet to retire. Therefore, given the optionality concerning the re-issuing of this stock, management could use these internal reserves to boost liquidity or invest in future growth initiatives. Now, although many investors do not look at high levels of treasury stock as necessarily being an advantage to companies (due to dilution accompanying the re-issuing of stock), in a company such as Kforce, it has distinct advantages such as the following.

- This ‘stock’ becomes essentially cash when required. Compare that fact with having a sizable debt balance, resulting in a similar shareholder equity total.

- It presents the option to keep financing in-house, which again keeps large interest expenses on loans at bay

- Look at the stock’s long-term chart above. The continuous increase in Treasury stock has been a good investment for shareholders, considering the`premium’ unretired stock now commands.

Suffice it to say, that not all reported book multiples from a valuation standpoint are created equal. Kforce has a strong balance sheet where assets outweigh liabilities by some margin.

Conclusion

To sum up, Kforce, (concerning its highly remunerated technology segment) is in the enviable position that its profits should remain elevated despite a potential rising unemployment rate and the continuous encroachment of artificial intelligence. The lion’s share of companies cannot state the same. Furthermore, the company’s proven ability to generate large amounts of cash flow should keep a floor under the stock even in temporary negative growth environments. We look forward to continued coverage.

Read the full article here